A Basic Guide To Indirect Cost Allocation for Government Contractors

Understanding how to identify direct and indirect costs is just the first step to DCAA compliance; you need to allocate costs correctly too.

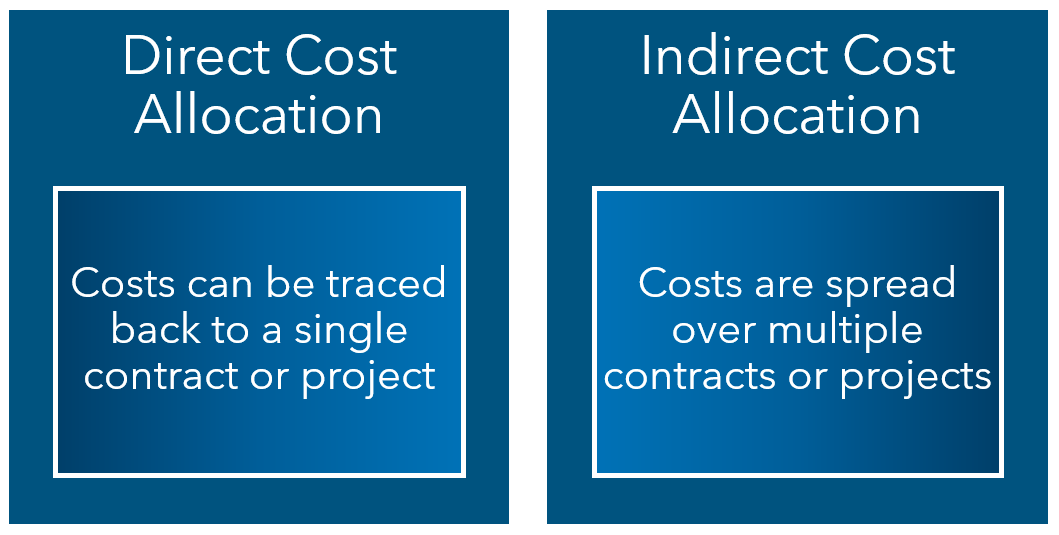

There are two basic types of cost allocation methods. The first relates to direct costs, and it’s straightforward because these can be traced back to a single contract or project. The challenge to achieving compliance is primarily about configuring your system to ensure costs are accumulated at the contract level.

The second type of allocation involves spreading indirect costs over multiple projects, which is more complex and highly subjective. Because it’s an area that often causes confusion for new and seasoned government contractors alike, we’ll take a closer look at how you can allocate indirect costs for DCAA compliance.

The Basics of Allocating Indirect Costs

Indirect costs cover a wide range of expenses incurred for multiple cost objectives (a cost objective is a technical way of referring to a project, contract, task or even a contract line item). It can also include things like an independent research and development undertaking, or a bid and proposal project. A company can have one or several indirect cost accounts.

DFARS requires indirect costs to be accumulated and allocated in a logical and consistent manner. For instance, you can’t assign a cost element as indirect if similar expenses for a different project have been included as a direct cost.

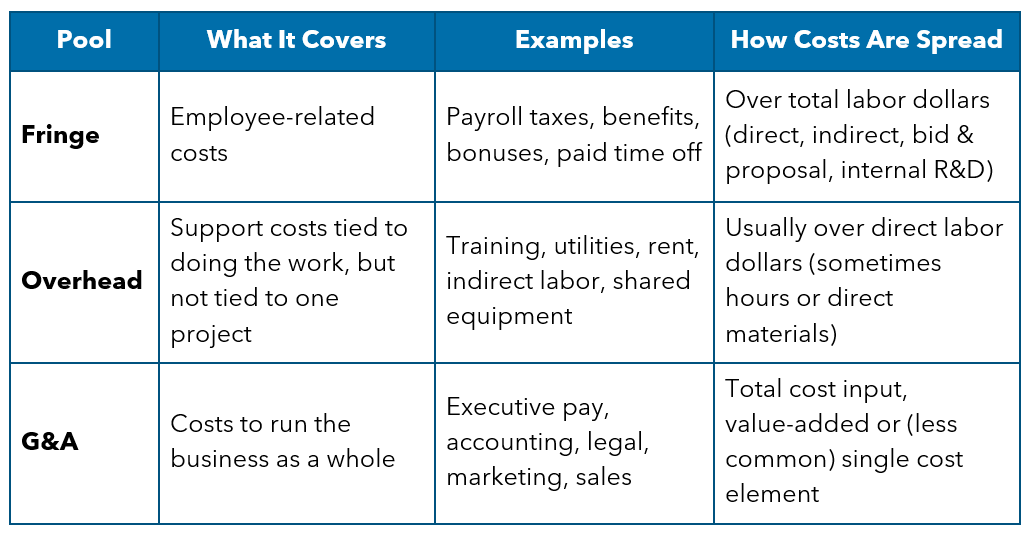

In practice, similar accounts are grouped together and aggregated in indirect cost pools. A typical indirect cost structure has three pools: fringe, overhead and general and administration (G&A).

Apart from ensuring DCAA compliance, getting your indirect costs right is crucial because it forms the basis of your indirect rates. Overstating your rates makes you less competitive and more likely to lose out when bidding for a contract. But if you understate your rates, you risk losing money on the contracts you do win.

Indirect Cost Allocation Requirements and Method

The aim of indirect cost allocation is to work out the proportion of non-direct expenses that each project will bear. This proportion is your indirect cost rate. The allocation should be based on the benefits brought to the contract or project, and the method of allocation is the same for all indirect cost pools: divide the total collected in the overhead, G&A or fringe pool by an appropriate allocation base.

You’ll need to use an allocation base that allows indirect costs to be apportioned reasonably and equitably. There must be a relationship between the allocation base and the cost pool. Accepted allocation bases differ across cost pools.

Using a simple example, let’s say you’ve incurred employee training costs in the overhead pool. Although the training was not taken for the performance of any particular project, it’s reasonable to conclude that all projects would likely benefit from your employees being better trained. In this case, the allocation base related to the cost pool could be direct labor dollars. Therefore, your allocation is the costs accumulated in the overhead pool divided by direct labor dollars.

Let’s further examine the cost accumulation and allocation bases for each indirect cost pool.

Fringe Pool

Fringe costs are incurred to attract and retain employees. These may include employer taxes, health insurance, 401(k), bonuses, compensated absences, and so on. Expenses are usually allocated over total labor dollars, which take into account direct and indirect labor, bid and proposal labor, and internal R&D labor.

Overhead Pool

The overhead pool captures indirect costs that support operations or direct production. However, these indirect costs can’t be traced to a single contract, project, order or product. There are many examples of costs that might be aggregated in the overhead pool, such as indirect labor, training, utilities, rent, quality assurance, supplies and depreciation of equipment used for multiple projects.

You may choose to have multiple overhead pools depending on the way your business operates. If you have multiple locations, it may be useful to have a separate overhead pool for each site. You may also choose to split overhead pools according to operating divisions and product lines.

You’ll need to choose an allocation base to apportion the costs in your overhead pool. A typical base for allocating costs in this pool is direct labor dollars; however, in certain instances, direct labor hours or direct material dollars may be used.

G&A Pool

G&A expenses are those incurred to run or manage the overall business. As such, they can’t be associated with a single project, contract, order, product or division. These expenses typically relate to functions that serve to benefit the entire organization, such as executive management, accounting and finance, legal, people and culture, technology, business development, marketing and sales.

Examples of G&A expenses might include salary of executive staff, salary of other staff (in functions like legal, accounting and public relations) and selling and marketing expenses.

Typical allocation bases for the G&A pool are as follows:

- Total cost input: G&A is applied to all non-G&A expenses.

- Value-added G&A: Subcontracts, direct materials and expenses from the G&A pool are excluded from the allocation base, which means your G&A rate will be higher compared to the total cost input method.

- Single cost element: Not commonly used, but it includes all costs of a chosen element (say, all direct labor costs).

Facilities Pool

A facilities pool is an intermediate pool that tracks costs like rent, utilities, depreciation and other maintenance costs, then allocates them over square footage or headcount for allocation into final indirect pools.

More Information About Cost Allocation Methods

As you can see, the types of allocation methods are very different for direct and indirect costs. While the rationale behind indirect cost allocation remains the same across each pool, the allocation base you should use changes.

If you would like guidance on how to optimize the structure of your cost pools and select an appropriate allocation base for each one, our GovCon experts can help. Our team of professionals combines technical know-how and practical experience to ensure your system is doing everything according to regulations. Reach out to your Warren Averett advisor directly, or ask a member of our team to contact you.

This article was originally published on September 20, 2020 and most recently updated on April 10, 2026.