You May Have State Income or Sales Tax Obligations in Places You’ve Never Set Foot In

Many companies have state tax exposure in places where they have no office, no employees and no property.

Most business leaders don’t realize it’s an issue, and it’s rarely something they investigate. The realization tends to surface later, during an audit, a pending transaction or a change in advisors, when someone asks a simple question:

Why aren’t you filing in this state?

So, why does that question come up unexpectedly? When does it matter? And what can you do to avoid unnecessary risk and last‑minute decisions?

Why States Care About Where You Sell (Not Just Where You Operate)

States used to rely heavily on physical presence due to two court cases (National Bellas Hess v. Department of Revenue and Quill Corp. v. North Dakota), which established a rule that states could only require businesses to collect and remit sales tax if there was a physical presence. Due to the rise of e-commerce in states, it became apparent there was an advantage to remote sellers, and states tried to become creative by expanding the definition of physical presence.

The landmark 2018 Supreme Court case South Dakota v. Wayfair changed how states defined nexus and determined filing obligations for sales tax purposes. In this case, the Court ruled that sales into a state can create nexus. This can be true even if the company has no people or property there.

After Wayfair, many states began to apply the same economic‑presence methodologies to other taxes, such as state income taxes, franchise taxes and other gross receipts taxes. Today, state tax exposure is increasingly connected to where revenue is earned, not only where operations are located.

Selling Into a State Doesn’t Automatically Mean You Owe Income Tax There

Sales into a state can create economic nexus for income tax as well; however, determining whether a filing obligation exists can vary by each state’s rules and what your company’s activity is in the state.

Why the same sales pattern leads to different answers

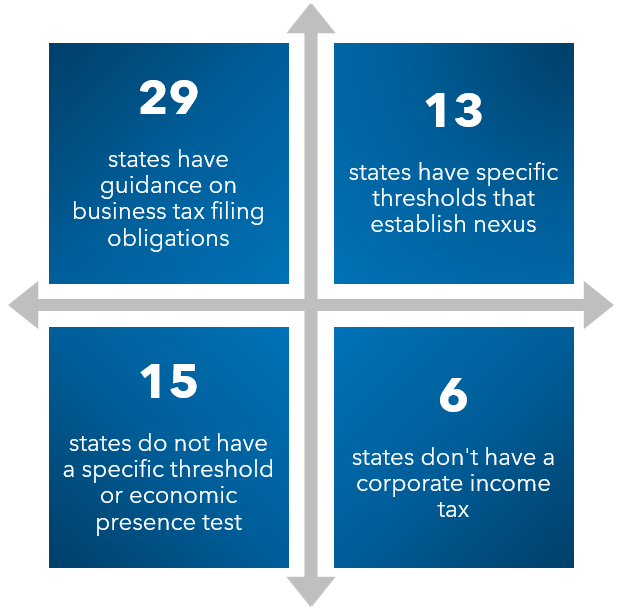

Since the Wayfair case, states began to apply economic presence for income tax in different ways. Some states have established a factor presence threshold, which clearly defines filing requirements if a taxpayer exceeds the stated property, payroll or sales amount in that state. Other states have set standards through statutes, regulations or court decisions. A few states have not issued clear guidance on economic thresholds or do not apply an income tax at all.

This means that selling into multiple states can create filing obligations in more places than expected, and the rules won’t look identical from state to state, or in the same state across differing tax types. A state may have one threshold for income tax, another for sales tax and yet another for gross receipts or franchise taxes.

When sales still don’t translate into state income tax

Even after a company crosses a state’s economic presence threshold, a federal law known as Public Law 86‑272 (P.L. 86-272) can protect the company from that state’s income tax in specific situations. The law was put in place to protect out-of-state businesses whose in-state activities are limited. In general, that protection can apply when:

- The company sells only tangible personal property

- In‑state activity is limited to soliciting orders

- Orders are approved and fulfilled from outside the state

Two boundaries matter:

- The protection doesn’t focus on the sales amount but rather the nature of the company’s revenue derived from the state.

- The protection only applies to income tax and does not apply to taxes not based on income such as sales tax, franchise tax and other gross receipts taxes.

It is important to note that when P.L. 86-272 and a state’s particular economic nexus statutes are in conflict, the federal law typically prevails under the supremacy clause in the Constitution.

Ultimately, businesses should treat sales thresholds as a prompt to evaluate income tax obligations, not necessarily an automatic tax bill. Sales can tell you which states deserve a closer look, but a company’s activities in a particular state can help determine whether there is likely a tax exposure and where other state taxes may still apply.

States are looking into companies’ websites and online presence to determine whether the activity exceeds the protection. Congress seems to be working through modernizing and expanding the protections to cover digital activities and solicitation. Much of the complexity stems from how online sales operate in practice, such as post‑sale customer support, the use of marketing or advertising cookies, offering extended warranties or service plans virtually and website sales that do not require separate order approval.

Estimating Your State Tax Exposure Before You Decide To File

You can’t make an informed decision about state filings without a rough estimate of what’s at stake. If you have business activity in a state and you are not filing a state income tax return there, it’s essential to work with your tax advisor to estimate your potential exposure so you can evaluate what steps are needed to mitigate your tax exposure.

This estimate is based on several factors and puts state filings in the same category as other business decisions: cost vs. benefit, supported by an educated estimate instead of guesswork.

Addressing State Tax Exposure From Prior Years

During the analysis process, it is possible that you may discover a state filing obligation existed in earlier years. That alone doesn’t point to an audit or a worst‑case scenario. That said, it does mean you have a choice to make about how to address the past before it turns into a distraction later.

One common way to handle prior‑year exposure is participating in a state’s voluntary disclosure agreement (VDA). In states that allow anonymous submission, a VDA allows you to approach the state without initially disclosing identity, agree to file a limited number of returns through the state’s lookback period and pay the outstanding tax obligations and related interest. (Other states require identification up front as part of the process.) In many cases, the lookback period is three or four years, and states will waive the penalties for late filing and payment.

This allows you to resolve prior-year exposure through a defined process with a clearer endpoint, instead of leaving the issue unresolved.

Learn More About Your Company’s State and Local Tax Obligations

This issue rarely shows up because someone did something wrong but appears when companies grow or expand without realizing how these changes affected them.

A good next step is to get a clear view of where your company earns revenue, where it currently files, what activities take place in each state and where economic presence rules may apply. With that visibility, leadership can decide with confidence where action is warranted and where it isn’t.

We recommend talking with your tax advisor at least once annually about your state tax footprint (your sales, payroll and property apportionment data) and your exposure for any state where you don’t file a state income tax return.

If you have questions about your state tax exposure, contact your Warren Averett advisor directly, or ask a member of our team to reach out to you to start the conversation.