The 4 Types of Nonprofit Financial Reporting That All Nonprofits Need

We’ve all heard the phrase: “garbage in, garbage out.” The same rationale holds true when it comes to nonprofit financial reporting and financial statements.

Stakeholders rely on a nonprofit’s financial reports to make important decisions about and for your organization, so if the information isn’t accurate, bad decisions are likely to be made.

Accurate financial information is also needed to apply for grants, to comply with funder reporting requirements, to comply with loan covenants and to effectively manage the organization.

But what kinds of nonprofit financial reporting do you really need to evaluate the fiscal health of your organization?

Here, we’ll take a further look into the four types of nonprofit financial reporting all organizations should prioritize (internal reporting, reporting to your Board, reporting to the IRS and reporting to external stakeholders), how they contribute to an organization’s financial health and why it’s all so important.

Consider These 4 Types of Nonprofit Financial Reporting

#1: Internal Budget Reporting

The budgeting process is much more than a formality. Budgeting sets the bar for a nonprofit’s financial performance and is essential to accurate nonprofit financial reporting.

Budgets should be created in line with a set budget policy, and they should reflect accurate data from the past and present, as well as sound forecasting for the future. But budgeting doesn’t end after the Board of Directors gives its approval over the final plan. That’s where budget reporting comes in.

It’s important that your Executive Director and management members consistently monitor your nonprofit’s budget-to-actual performance in case you need to make revisions due to unexpected events.

What sources are generating the most funding for your nonprofit? What items account for your expenses? Are there significant deviations from the budget that need to be addressed?

It’s best to review and ask these questions monthly so you can pivot when you need to.

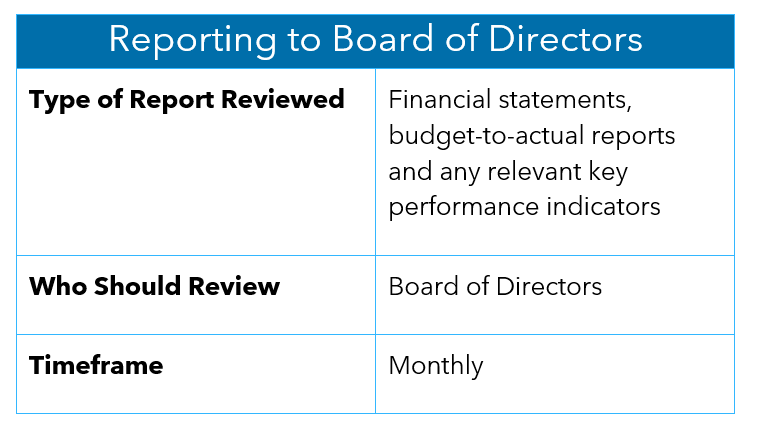

#2: Monthly Reporting to the Board

Providing accurate nonprofit financial reporting to your Board of Directors contributes to a financially healthy organization. It’s best to have your Board review your organization’s financial statements, budget-to-actual reports and any relevant key performance indicators once each month.

Management and the Board of Directors need to be able to review and understand the financial information that is presented to them in order to identify potential problems. This review and understanding are part of their fiduciary duty.

During their review of these nonprofit financial reports, potential warning signs that management and the Board should be looking for include:

- Increasing rates of expenditures

- Growing debt balances

- Defaulting on debt obligations

- Continued declines in cash balances

- Borrowing from reserves to pay current expenses

- Continued budget overruns

- Increasing number of employees needed to provide the same services

- Declining investment returns that are disproportionate to trends in investment yields

- Declines in volunteer hours

- Declines in numbers of constituents served

These warning signs may indicate that a nonprofit organization is not financially stable and is struggling to maintain its financial independence. They can also indicate that public image is in decline or that management is ineffective.

Any and all of these warning signs seen in any nonprofit financial report should be taken seriously by management and the Board.

#3: Annual Reporting to the IRS (Form 990)

The Form 990 is a nonprofit financial report that is often not given the attention it needs. The Form 990 is an opportunity for a nonprofit organization to tell your story, so making sure that accurate information goes into the Form 990 is essential.

While the IRS is commonly associated with the Form 990 (and rightly so), it’s important to remember that the Form 990 is a nonprofit financial report that’s also used by many others to learn about an organization.

Watchdog agencies like Charity Navigator, use the Form 990 to rate charities based on financial health, accountability and transparency. When considering what organizations to donate to, many donors rely on these watchdog agencies, and thereby, the information on the Form 990.

Therefore, if your nonprofit organization isn’t taking the time to make sure the information in your Form 990 is accurate, you may be hurting your overall image in the eyes of donors.

#4: Annual Reporting to External Stakeholders

Accurate nonprofit financial reporting is also imperative for outside stakeholders, including donors, volunteers and funders.

From a donor’s and volunteer’s standpoint, people want to give their time and treasures to organizations that are financially stable. From a funder’s standpoint, most major funders require organizations to provide some level of reporting.

From either standpoint, if the nonprofit financial reporting provided isn’t accurate, organizations can risk both financial and reputational damage.

Financial damage could include donors choosing to donate to another organization, or funders deciding to discontinue funding (or requiring funds to be returned). Reputational damage could occur in situations where inaccurate reporting is a result of fraud, negligence or other misappropriation.

At least once each year, nonprofits should make their audited financial statements, annual program reports and the organization’s annual report available to external stakeholders. Your organization’s annual report is a particularly valuable communication because it helps to establish trust with your contacts, highlight major accomplishments and inspire and thank your supporters.

Building trust with your stakeholders is essential, especially in today’s economy, and tying your nonprofit’s financial reporting back to your mission helps bring it all full circle.

Moving Forward With Nonprofit Financial Reporting

As you can see, providing accurate and timely information in nonprofit financial reporting is imperative for management and Board members to carry out their fiduciary responsibilities, and to effectively manage the organization.

Further, management and Board members need to understand nonprofit financial reporting so they can ask appropriate questions and are able to spot potential warning signs.

At the end of the day, the best practices for nonprofit organizations are the ones that will create timely and accurate financial reporting for your organization, which in turn can fuel your nonprofit to accomplish what matters most—your mission.

For more information about nonprofits or to learn more about how your nonprofit can better understand its financial management and reporting, reach out to your Warren Averett advisor, or ask a member of our team to reach out to you to get the conversation started.

This article was originally published on May 12, 2021 and most recently updated on November 30, 2023.