Good Business, Bad Timing (How Market Conditions Override Performance More Often Than Owners Expect)

Many business owners approach an exit expecting that stable revenue, consistent margins and management depth will translate into a smooth sale.

These are the fundamentals buyers are supposed to value, and in isolation, they do. But the transaction market doesn’t evaluate businesses in isolation. It evaluates them against capital availability, buyer appetite, credit conditions and competitive deal flow.

Owners who conflate operating results with deal outcomes are frequently caught off guard when the two diverge. And they diverge more often than most expect.

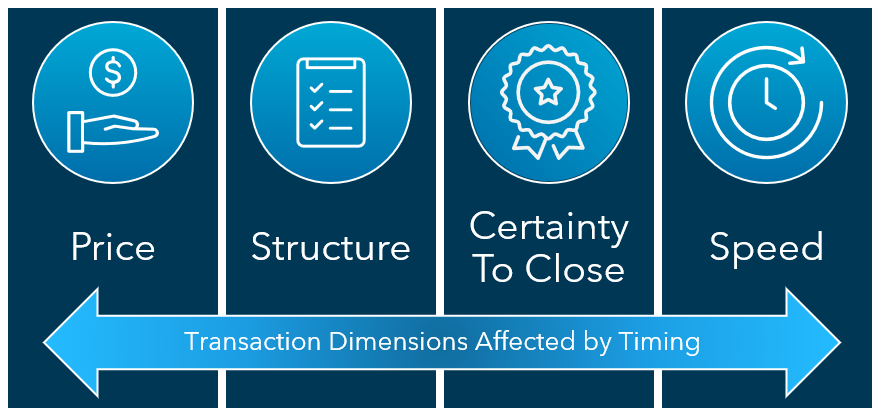

The solution is to understand what timing means in business transactions and how it influences the four dimensions of any transaction: price, structure, certainty to close and speed.

What Does “Timing” Mean in a Business Sale?

In mergers and acquisitions (M&A), timing refers to the prevailing state of buyer behavior the moment a sale is initiated, not when the business is operationally ready for sale.

Macroeconomic conditions, interest-rate environments, credit-market liquidity, sector-specific sentiment and the cumulative deal activity shape buyer behavior. These factors are largely outside an owner’s control and independent of the underlying business performance.

The business didn’t change; the market did.

How Does Timing Affect Price?

Valuation multiples aren’t static. They’re a function of market competition, financing costs and the perceived riskiness of future cash flows. When market conditions tighten, fewer buyers are willing to pay at the top end of valuation ranges, and the spread between high and low offers widens.

Forecasted performance carries less weight than audited historical results because buyers discount forward-looking figures in times of elevated macroeconomic uncertainty.

Normalized adjustments and addbacks are standard components of most quality-of-earnings analyses. These also face heightened scrutiny.

Buyers are less inclined to credit non-recurring expense removals or pro forma synergies, compressing the effective purchase price even when the stated multiple appears reasonable.

How Does Timing Affect Deal Structure?

Price and structure aren’t independent variables. When buyers can’t (or won’t) pay the full negotiated value at close, they shift a portion of consideration into contingent or deferred instruments. Earnouts, seller notes, equity rollovers and holdback provisions happen frequently, and each transfers economic risk back to the seller.

A transaction that closes at a nominally attractive headline price but includes a 20% earnout tied to two years of post-close revenue targets is materially different from one that closes entirely in cash.

Sellers unprepared for this dynamic may find themselves obligated to remain involved in a company they intended to fully exit.

How Does Timing Affect Certainty To Close?

Deal certainty is the probability that a signed letter of intent (LOI) will lead to a completed transaction. It’s an underappreciated dimension of market timing.

Buyers with committed capital and streamlined approval processes move efficiently from indication to close in active markets. But the opposite dynamic prevails in constrained markets. Contingencies multiply and financing conditions become more onerous. Regulatory and governance approvals require additional layers of internal review.

Buyers may renegotiate pricing or terms after the exclusivity period has commenced. These late-stage retrades divert management’s attention, increase confidentiality risks and reduce the seller’s negotiating leverage.

A business that is performing well isn’t immune to these dynamics.

How Does Timing Affect Speed?

Transaction timelines expand when market conditions tighten. The interval between first meaningful buyer contact and signed definitive agreement lengthens as buyers conduct more intensive preliminary due diligence before committing to exclusivity.

Once in exclusivity, diligence periods extend as the buyer engages additional specialist advisors such as cybersecurity specialists, environmental consultants and compensation analysts. Buyers work on building a more defensible investment thesis for their internal approval processes.

Extended timelines also increase operational risks for sellers. It increases management distraction and can scare key employees, customers and vendors if they’re aware of the process.

The same transaction that might have closed in four months in a favorable environment may require twice as much time in a constrained one, and each additional month carries incremental exposure.

How Do Market Conditions Change Buyer Behavior?

When market conditions tighten, institutional buyers adjust their internal investment criteria. Return hurdles increase, approval thresholds rise and buyers pay more attention to documentation quality and management transferability.

In a tight market, a private-equity firm that once underwrote a deal on projected cost synergies may now require demonstrated EBITDA with minimal adjustments, a diversified customer base with long-term contracts and a management team willing to roll an equity stake.

Buyers still value strong historical performance and incremental growth, but these traits don’t remove buyer caution or reliably improve price, structure or certainty when the broader market environment shifts.

Waiting for conditions to improve isn’t always the answer. Extended timelines can introduce new operational and personnel risks without producing a materially better market.

How Should Owners Looking To Sell Think About Timing?

Owners who understand timing as an independent variable in the exit equation make different decisions than those who don’t. They develop expectations based on realistic outcome ranges rather than single-point estimates. They evaluate tradeoffs and might accept a lower price in exchange for greater certainty to close.

Preparation efforts focus on demonstrating proof and transferability with:

- Clean, audited financial statements

- Documented operating procedures

- Diversified revenue streams

- A management team capable of operating independently of the founder

Learn More About Planning for the Sale of Your Business

Even strong companies can face difficult exits when market conditions affect how buyers evaluate, structure and execute transactions.

Attributing exit friction solely to internal business deficiencies leads to pursuing remedies that don’t resolve the underlying issue and flawed decisions about timing, price and deal terms.

Reach out to your Warren Averett advisor directly or ask a member of our team to contact you for guidance on navigating the gap between intrinsic business value and market price at a given moment. Those two figures often differ, and the difference is rarely the business’s fault.