The One Big Beautiful Bill Act Breakdown: Bonus Depreciation

Bonus depreciation is a tax savings tool that allows businesses to automatically deduct some or all of the cost of qualifying assets upfront, and the One Big Beautiful Bill Act made changes to it for businesses.

The Previous Tax Law

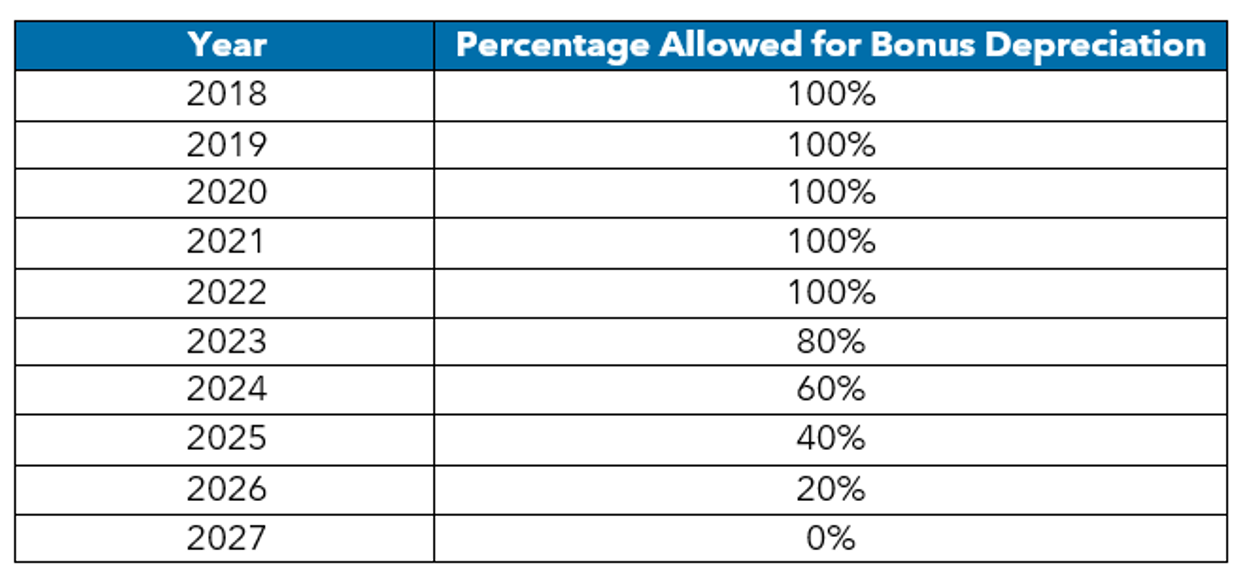

Under the Tax Cuts and Jobs Act (TCJA) of 2017, bonus depreciation allowed businesses to deduct 100% of the cost of qualifying assets (property with a life under 20 years) that were placed in service after September 27, 2017, and before January 1, 2023.

This deduction phased out by 20% annually from 2023 through 2026 and was set to reach 0% in 2027. For tax year 2025, the bonus depreciation rate stood at 40%.

New and Final Law Under the One Big Beautiful Bill Act

While the House’s version of the legislation featured a temporary extension of this bonus, the Senate’s version (the final version) of the bill made it permanent.

The One Big Beautiful Bill Act reinstates 100% bonus depreciation for assets acquired after January 19, 2025. The definition of qualifying property is unchanged, and the bill does not apply retroactively to asset purchases in 2023 or 2024.

This means that if your business had a contract to acquire property prior to January 20, even if the actual acquisition happens afterwards, the property will not qualify for the 100% bonus. The property will qualify for bonus depreciation, if eligible, based on prior law.

What It Means for You

The enhancements to bonus depreciation expand access to the deduction, allowing more businesses to benefit from increased up-front tax savings in the years ahead. The ability to elect out of bonus depreciation and use Section 179 selectively provides valuable flexibility for managing taxable income across entities or years. This strategy should be discussed with your tax advisor to ensure optimal planning.

It’s also important to remember that state conformity varies. Business owners operating in multiple states should consult their tax advisors to understand how these deductions will be treated at the state level.

As of January 2026, the IRS has issued Notice 2026‑11, which largely reaffirms the existing bonus depreciation framework under Reg. §1.168(k)-2, with updated effective dates.

Key confirmations include the definition of an acquisition date, continued availability of the 10% safe harbor for non‑binding contracts, support for component elections and the option to elect 40% bonus depreciation for the first tax year ending after January 19, 2025. We will continue to monitor developments as additional regulations are issued.

To learn more about how the One Big Beautiful Bill Act and this specific provision may impact you, contact your Warren Averett advisor.

This article was originally published on July 25, 2025, and most recently updated on January 21, 2026.