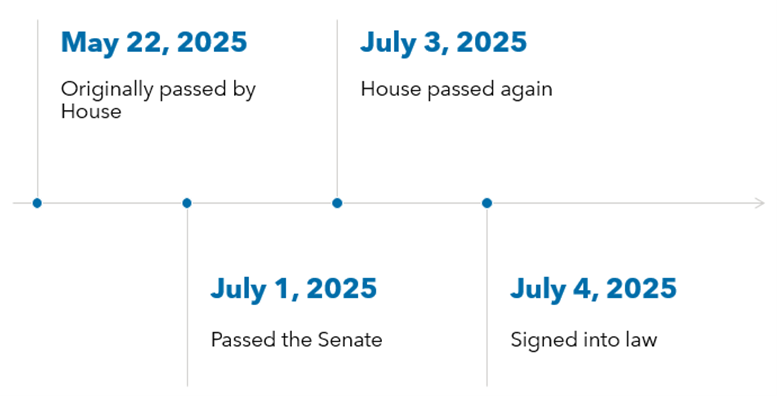

30 (Yes, 30) Ways the “One Big Beautiful Bill” Will Impact Your Taxes

In case you missed it: Watch Warren Averett’s July 10 webinar to get clear, practical guidance on what the new legislation means and how to move forward with confidence. Access the on-demand recording here.

The legislation that has become most commonly known as the “One Big Beautiful Bill” (OBBB) is now law, and true to its name, it’s big, complex and full of major tax changes.

Under the OBBB, many of the provisions from the Tax Cuts and Jobs Act of 2017 that would have expired have now been modified, extended or made permanent. Plus, the OBBB has introduced several new tax provisions of its own. Each provision comes with its own effective and expiration dates, making the overall landscape even more intricate.

Ultimately, the best way to accurately understand how your business should respond is to connect with your tax advisor to discuss how the changes will impact your organization’s unique situation.

Until then, we’ve outlined 30—yes, 30—of the largest ways that you can expect your taxes to be impacted by the OBBB.

1. Bonus Depreciation

This bill reinstates 100% first-year depreciation for qualifying property (with a useful life under 20 years), effective for assets placed in service after January 19, 2025. However, if a binding contract to acquire the property existed before that date, 100% bonus doesn’t apply.

While the House’s version of the bill proposed a temporary extension, the Senate made this provision permanent, which is a welcome change after years of short-term renewals.

2. Qualified Production Property

One of the most talked-about provisions in the bill is the ability to fully expense manufacturing buildings, which were previously depreciated over 39 years. Under the new law, facilities used in “qualified production activities” can qualify for 100% bonus depreciation. However, there are several important caveats, so it’s essential for businesses to consult a tax advisor before moving forward in this area.

3. 179 Expensing

The bill also significantly expands Section 179 expensing, doubling the maximum deduction to $2.5 million, with a phase-out starting at $4 million in total purchases for tax years beginning after December 31, 2024. These amounts are adjusted annually for inflation starting in 2026. The changes to 179 expensing make it easier for businesses to immediately deduct the cost of personal property and certain real property.

4. R&D

The bill reverses a key provision that previously required taxpayers to capitalize and amortize research and development expenses. Starting in tax years beginning after December 31, 2024, domestic R&D expenses can once again be fully expensed, but taxpayers can also choose to continue capitalizing expenses if it better suits their strategies. Small businesses can amend prior year returns to retroactively expense capitalized domestic R&D expenses.

All other taxpayers (and small business taxpayers) can elect to deduct any unamortized R&D expenses from 2022–2024 on their 2025 return. It’s important to point out that there were no changes to the treatment of foreign R&D expenses, and they must continue to be capitalized and amortized over 15 years.

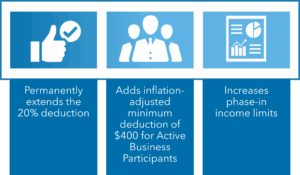

5. Qualified Business Income

The bill permanently extends the 20% Qualified Business Income (QBI) deduction for pass-through entities, which was originally set to expire after 2025. Starting in tax years after December 31, 2025, the bill also raises income phase-in thresholds and adds a $400 inflation-adjusted minimum deduction for active business owners.

6. Changes To Interest Expense Limitation

This provision affects businesses subject to interest expense limitations. Under the 2017 tax law, a business’s interest expense deduction limit was based on EBITDA, but starting in 2022, it shifted to EBIT—excluding depreciation and amortization—reducing deductible interest. The new law restores the EBITDA standard for tax years beginning after December 31, 2024.

There were also changes to how EBITDA is calculated under the new law that goes into effect for tax years beginning after December 31, 2025. For example, certain capitalized interest is now also subject to the limit.

7. Qualified Small Business Stock

There are major enhancements to Section 1202, the Qualified Small Business Stock (QSBS) exclusion. For stock issued after July 4, 2025:

- The gain exclusion limit increases from $10 million to $15 million, now indexed for inflation.

- The gross asset limit for issuing QSBS rises from $50 million to $75 million, expanding eligibility.

- The five-year holding requirement is relaxed:

- 3 years = 50% exclusion

- 4 years = 75% exclusion

- 5+ years = 100% exclusion

The changes to the QSBS exclusion will allow more taxpayers to issue QSBS and is intended to encourage investment in U.S. corporations.

8. Corporate Charitable Deductions

The bill introduces a 1% floor on corporate charitable deductions. While corporations can still deduct up to 10% of taxable income, the first 1% is now non-deductible.

9. Percentage of Completion Method of Accounting Exception for Residential Construction Contracts

Previously, contractors were generally required to recognize income on long-term contracts using the percentage-of-completion method. There were two exceptions: small contractors and those working on home construction. The new law allows for larger residential projects to also qualify for the exception.

10. Partnership Sale Rules

The bill also tightens the disguised sale rules for partnerships. While the wording updates here may seem minor, they effectively lead to a change that will broaden the rules’ applicability, making them more relevant to a wider range of transactions.

11. FICA Tip Credit

Spas, barbers and similar service providers are now eligible for the FICA tip credit, an employer credit equal to 7.65% of reported tips, which was previously only available to those in the food and beverage industry.

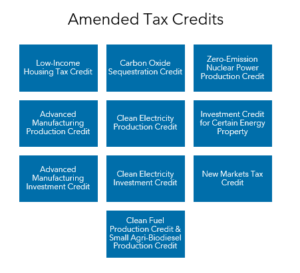

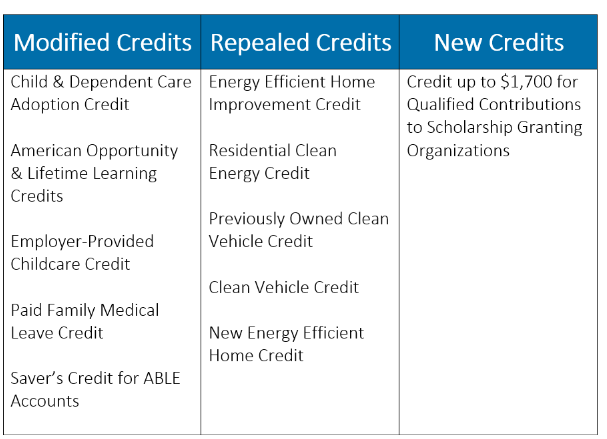

12. Business Tax Credits

The bill phases out several existing tax credits for businesses—particularly in green energy—and modifies others by changing how they’re calculated or who qualifies. It also makes significant changes to the Employee Retention Tax Credit.

13. Individual Tax Rates

The bill permanently extends the lower individual tax rates introduced by the Tax Cuts and Jobs Act, keeping the top marginal rate at 37% instead of reverting to the pre-TCJA rate of 39.6% in 2026. Only the bottom three brackets are adjusted for inflation, and capital gains tax rates remain unchanged under this bill.

14. Alternative Minimum Tax Exemption and Phase-Out

The Alternative Minimum Tax (AMT) was designed to ensure high-income taxpayers pay a minimum level of tax by disallowing certain deductions and recalculating income.

The Tax Cuts and Jobs Act significantly increased the AMT exemption, reducing the number of taxpayers affected. The new bill makes that higher exemption permanent.

15. Deduction for Tip Income

The bill includes a new above-the-line deduction for tip income, which has been commonly referred to as “no tax on tips.” Starting in 2025, taxpayers can deduct up to $25,000 in qualified tips annually, with phase-outs beginning at $150,000 and ($300,000 for joint filers) of income, respectively.

It’s important to note that this is a deduction and not a full exemption. The provision runs through 2028 and is expected to reduce the tax burden for many service industry workers.

16. Overtime Pay Deduction

The final bill includes a new overtime pay deduction: up to $12,500 for single filers or $25,000 for joint filers can be excluded from income, with phase-outs starting at $150,000 (single) and $300,000 (joint). Only the premium portion of overtime pay qualifies for the deduction.

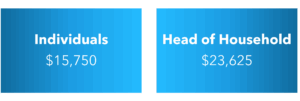

17. Standard Deduction Increase

The doubled standard deduction, which was set to expire, is now permanent. It also includes a modest increase for individuals and heads of household to further reduce the number of taxpayers who itemize.

18. SALT Cap

The state and local tax (SALT) deduction cap increases from $10,000 to $40,000 starting in 2025, though it will revert after 2029. The $40,000 cap phases down (not out) for incomes over $500,000.

19. Itemized Deductions and Other Items

The bill makes several notable changes to itemized deductions for individuals:

- Taxpayers can now deduct up to $10,000 in auto loan interest, as an above the line deduction, on auto loans starting after December 31, 2024, with a phase-out beginning at $100,000 for single filers or $200,000 for joint filers.

- A new 0.5% floor applies to itemized charitable deductions, but all non-itemizers can now claim an above-the-line deduction up to $1,000 for single filers or $2,000 for joint filers.

- Individuals taxed at the top tax rate will see a 2% haircut on itemized deductions, and the value of deductions will be capped at 35%.

- The $750,000 cap on acquisition debt and the disallowance of home equity interest remain unchanged.

- Most miscellaneous deductions are now permanently disallowed, except for educator expenses, which remain deductible.

20. Repeal of Personal Exemption

Personal exemptions were set to return in 2026, but the new bill permanently repeals them.

To offset this, the doubled standard deduction has been made permanent, maintaining broader tax relief for most filers.

21. New Senior Deduction

Starting in 2025, taxpayers over the age of 65 can deduct up to $6,000 from taxable income, subject to income-based phase-outs. The deduction phases out when income exceeds $75,000 for single filers and $150,000 for married filing joint filers.

22. Child Tax Credit

The Child Tax Credit, which was increased to $2,000 per child under the 2017 Tax Cuts and Jobs Act, will now rise to $2,200 starting in 2025.

23. Natural Disaster Provisions

The bill expands the casualty loss deduction for individuals. While most miscellaneous itemized deductions remain disallowed, personal casualty losses are deductible if they result from a natural disaster. Previously, this applied only to federally declared disaster areas. The new rule also includes state-declared disaster areas, offering broader relief to taxpayers in disaster-prone regions.

24. Trump Accounts for Newborns

For children born between 2025 and 2028, the government will deposit $1,000 in seed money if the account is opened. Withdrawals are not allowed until age 18, except in limited circumstances, and once the child reaches 18, the account is taxed like an IRA. Additionally, employers can contribute up to $2,500 per year to these accounts on behalf of employees’ dependents.

25. Individual Tax Credits

Many energy-related credits were repealed or scaled back, and several others were modified. The law introduces a new individual credit of up to $1,700 for qualified contributions to scholarship-granting organizations, offering a fresh incentive for educational giving.

26. Estate Tax

The estate and gift tax exemption has been permanently increased. Starting in 2026, the exemption will be set at $15 million per person (or $30 million for married couples), up from $13.99 million in 2025.

27. Nonprofits

Many of the proposed changes to private foundations and tax-exempt organizations did not make it into the final bill. However, the final bill significantly increases the excise tax on endowments for private colleges and universities. The top rate rises from 1.4% to 8%, though the exemption threshold was expanded to include institutions with at least 3,000 tuition-paying students.

28. Opportunity Zones 2.0

The new law introduces “OZ 2.0,” starting January 1, 2027. It offers similar benefits: capital gain deferral, a 10% exclusion of the original gain if held for five years, and full exclusion of appreciation if held for 10 years. While the structure is similar to the original Opportunity Zones program, OZ 2.0 includes some enhancements and new criteria and designations.

29. International Tax

The bill includes important changes for U.S. individuals and businesses that own controlled foreign corporations (CFCs). While the technical details are complex, the key takeaway is that the effective tax rates under these provisions will generally be lower than if the TCJA provisions had expired.

30. 1099 Reporting

The bill raises the 1099 reporting threshold from $600 to $2,000, effective for payments made starting in 2026. This change will ease the compliance burden for businesses that work with many independent contractors, reducing the number of required filings. For 2025, the $600 threshold still applies.

Learn More About Tax Changes That Impact You

Even though the bill is law, it will continue to evolve as Treasury interprets the new law and issues guidance in key areas. If you’d like to gain a better understanding of what’s in the bill and how it could specifically impact you, connect with your Warren Averett advisor directly.