Safe Harbor 401(k) Plans: What They Are and How They Work

Compliance testing is one of the biggest hurdles business owners face when offering a 401(k) plan to employees. A Safe Harbor 401(k) plan allows plan sponsors to avoid the majority of those mandatory compliance tests and their related hassles.

But is it the right option for your business?

What Is a Safe Harbor 401(k) Plan?

A Safe Harbor 401(k) plan is a type of retirement savings plan that automatically satisfies many of the IRS’s nondiscrimination requirements. These plans mitigate many of the restrictions that a traditional 401(k) plan can have.

The key feature of a Safe Harbor 401(k) is mandatory employer contributions. Employers must make annual contributions to all eligible employees, and these contributions are immediately fully vested.

Those required contributions can take one of two forms:

- Matching contributions: The company provides an employer contribution to eligible employees who elect to participate in the plan by making regular payroll deductions. For example, an employer might match 100% of employee contributions up to 3% of compensation plus 50% of the next 2% of compensation.

- Non-elective contributions: All eligible employees receive an employer contribution of at least 3% of compensation, regardless of an employee’s deferral amount into the plan.

Employers can also offer a Qualified Automatic Contribution Arrangement (QACA)—a specific type of Safe Harbor 401(k) plan that includes an automatic enrollment feature.

In a QACA plan, a default employee deferral of a set percentage (typically 3%) is made to the plan unless the employee opts out in writing. Those automatic contributions can increase each year up to a specified percentage. Employers typically match 100% of the first 1% of contributions and 50% of deferrals between 1% and 6% of compensation.

What’s the Difference Between a Safe Harbor 401(k) Plan and a Traditional 401(k) Plan?

There are a few key differences between a Safe Harbor 401(k) plan and a traditional 401(k) plan.

Nondiscrimination Testing

Traditional 401(k) plans are subject to annual nondiscrimination testing. These tests ensure contributions and benefits do not disproportionately favor highly compensated employees (HCEs) over non-highly compensated employees (NHCEs).

Safe Harbor 401(k) plans are exempt from most of these tests because they automatically meet the requirements.

Employer Contribution/Vesting Requirements

In traditional 401(k) plans, employer contributions may be subject to a vesting schedule, meaning employees must work for the company for a certain period before gaining full ownership of the employer contributions.

Safe Harbor plans require immediate vesting of the safe harbor contributions.

Administrative Responsibilities and Costs

Safe Harbor 401(k) plans are more straightforward to administer without many of the nondiscrimination testing issues and the obligation to maintain a vesting schedule. This simplicity helps keep administrative costs low.

Traditional 401(k) plans are typically more expensive to administer due to the annual nondiscrimination testing requirements, even if employer contributions to the plan are higher.

With a Safe Harbor 401(k) plan, mandatory employer contributions may mean more benefit costs for the employer, but because these plans automatically satisfy testing requirements (the Actual Deferral Percentage (ADP), Actual Contribution Percentage (ACP), and top-heavy tests), those costs are usually offset by the additional benefits of lower administrative costs and the ability of higher wage earner limitations to be removed.

Compliance Requirements

Employers with Safe Harbor 401(k) plans must meet specific participant disclosure requirements to maintain their status. These disclosures give participants the information necessary to make timely and informed decisions about their retirement accounts.

Traditional 401(k) plans do not require participant disclosures, although they are recommended.

How Should I Determine if a Safe Harbor 401(k) Plan Is Right for My Company?

Both traditional 401(k) plans and Safe Harbor 401(k) plans can be a viable choice for your business. So how do you decide which one is right for you? Asking yourself the following questions can help.

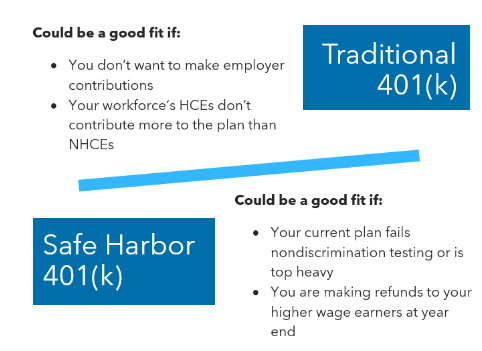

Do I have issues with 401(k) nondiscrimination testing?

If your current 401(k) plan frequently fails nondiscrimination testing, resulting in corrective distributions or contribution refunds, a Safe Harbor 401(k) plan could resolve these issues by automatically meeting the testing requirements.

Is my plan top-heavy?

A plan is considered top-heavy if more than 60% of its assets are in the accounts of key employees. Safe Harbor 401(k) plans help avoid top-heavy plan issues, simplifying administration and compliance.

Can I make required employer contributions consistently?

Safe Harbor plans mandate specific employer contributions. To avoid potential compliance issues, ensure your company can reliably make these contributions.

Can I fulfill compliance requirements?

Consider whether your company can meet the compliance and administrative responsibilities associated with a Safe Harbor 401(k) plan, including the annual notice requirement.

What is my capacity for plan administration?

Assess whether your company has the resources to handle the administrative aspects of a traditional 401(k) plan. Opting for a Safe Harbor 401(k) plan can help keep your compliance burden manageable.

Get Trusted Guidance to Choose the Right 401(k) Plan

Choosing the right 401(k) plan for your business involves carefully considering various factors, including compliance, administrative capacity and employee preferences.

While a Safe Harbor 401(k) plan offers many benefits, it’s not the right solution in every situation. For personalized guidance and to ensure the best decision for your company’s retirement plan needs, contact Warren Averett Benefit Consultants.