What is a SOC 1 Report? (An Overview for Businesses)

System and Organization Controls (SOC) reports are intended to help service organizations build trust with their customers. It’s also for companies looking to understand the controls their vendors have in place and manage any risk associated with using vendors as part of their day-to-day business.

If your business is curious about a SOC 1® report, there are a few basics to understand that can set you up for success.

There are different SOC reports, and each has a different area of focus intended to meet the needs of the service organization and the user entities—customers and clients—that work with them.

The SOC 1 report is focused on financial reporting.

What is a SOC 1 Report?

The SOC 1 report addresses the internal controls of a service organization and the effect those controls may have on a user entity’s financial statements.

What is the SOC 1 Criteria?

The control objectives of the SOC 1 report are the overarching goals—depending on your specific organization—that the controls themselves are designed to meet. Essentially, the SOC 1 control objectives are the “why,” and your organization’s internal controls are the “what” and “how.”

For example, a control objective for a SOC 1 report may be “Controls provide reasonable assurance that logical access to system resources is restricted to properly authorized personnel.” There will then be a series of controls, such as “Role-based access is utilized to allow appropriate users to see but not edit data” and “Access control privileges are reviewed monthly.”

What is the Intent of a SOC 1 Exam?

The intent behind SOC 1 examinations stems from attestation examinations.

This means that the management for a service organization asserts and documents the existence of controls associated with financial reporting, and a qualified CPA firm then reviews those assertions and provides an opinion on whether the controls provide reasonable assurance that the risk is mitigated or addressed adequately.

The intent of the report is to prove that the service organization has the proper controls defined and in use, as reviewed and determined by a third party, that controls the integrity of financial reporting and the data used for it.

It is not a guarantee by the third-party assessor of protections; rather, it confirms only that the controls, as designed and implemented, should mitigate risks in the assessor’s opinion.

It’s important to note that the purpose isn’t to identify that there is a single control in place for every risk. Instead, the controls are reviewed individually and as a whole for coverage and effectiveness.

What are SOC 1 Reports Used For?

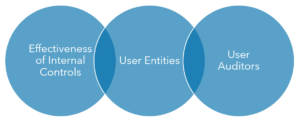

Because SOC 1 reports review the controls an organization has designed and implemented to protect the integrity of financial data, they have a number of uses.

First, they are used by the service organization itself to help them understand the impact and effectiveness of the internal controls they have in place to address risks to the organization and the services it provides. Also, should a SOC 1 report find issues with the existing controls, the service organization can use that information to target areas of improvement.

Second, they give assurance to the service organization’s users that the appropriate controls are in place and working consistently.

Lastly, the SOC 1 reports are reviewed by user auditors when planning and performing audits on a user entity’s financial statements.

Who Needs a SOC 1 Report?

SOC 1 reports are needed by organizations that perform services that could impact their clients’ financial statements.

Common examples of these kinds of entities include payroll processors, trust departments, employee benefit or retirement plan operators, registered investment advisors, loan servicers, payment processors and others.

However, even if your organization is not among those listed above, if the services you provide can affect a user entity’s financial reporting, you’ll also need a SOC 1 report.

What is Included in a SOC 1 Report?

The SOC 1 report itself is fairly straightforward. It includes general information about the organization, as well as the period covered by the report.

The control objectives are documented, as well as the controls designed to meet those objectives.

Any tests performed by the service auditor, as well as the results of those tests, are recorded, and the overall opinion of the auditor is noted as unmodified (i.e., there were no significant issues found with the design of controls or their implementation, if appropriate), qualified or adverse.

A qualified or adverse opinion, where an issue was found, will also document the potential risk and is determined by the pervasiveness or materiality of the issue.

Have More Questions about What a SOC 1 Report is? Want More SOC 1 Report Examples?

The SOC 1 report is important for service organizations to ensure that they are recognizing, accounting for and mitigating risk in financial reporting and financial data.

The report is also key in proving to user entities that the service organization is taking commercially reasonable precautions and that they are considering and addressing any risk to their own financial reporting. If the services your organization provides to clients potentially have an impact on their financial statements, you’ll likely be asked to provide a SOC 1 report.