Cash Balance Plans: What They Are and How They Work

What are cash balance plans? And what does having a cash balance plan mean for your company?

Here, I’ve outlined what cash balance plans are, how they operate and key terms to know as you consider your company’s retirement plan options.

Resource: Compare your options with this retirement plan comparison chart.

What are Cash Balance Plans?

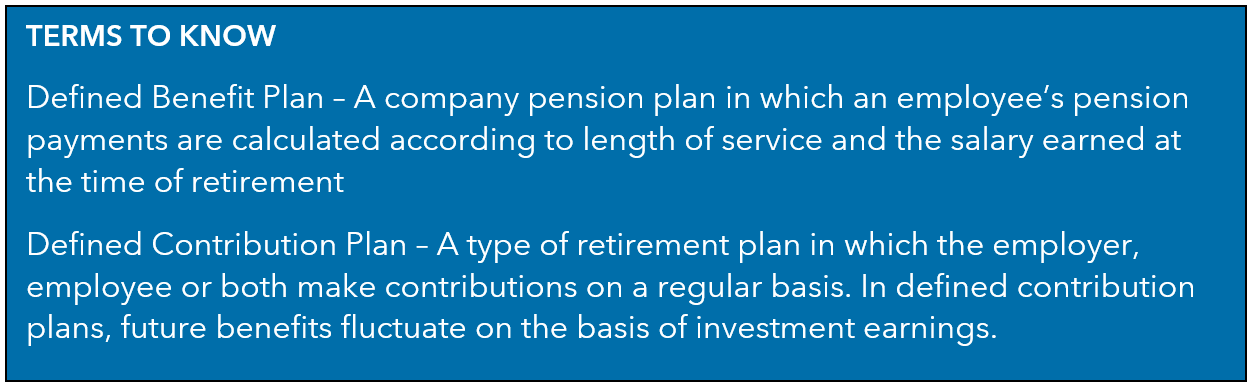

A cash balance plan is a type of defined benefit plan that operates differently than other types of retirement plans, like 401(k) profit-sharing plans or traditional defined benefit plans.

Cash balance plans are often referred to as “hybrid plans” because, generally speaking, they offer the best of both worlds:

- the high contribution limits of defined benefit plans; and

- the ease of understanding a defined contribution plan.

Most cash balance plans are established for the primary benefit of the owners or executives of a company. So, the contributions from the company for owners and executives are typically very large, with a smaller contribution provided to staff to meet Internal Revenue Service (IRS) requirements.

When setting up a cash balance plan, the sponsoring company selects the amount of contribution for each owner and executive, up to the maximum amount permitted by law.

Only businesses can sponsor a cash balance plan, and any business entity may do so, even if the owner of the business is its only employee.

Why are Cash Balance Plans Growing in Popularity?

Cash balance plans are becoming an increasingly popular option for benefit plan design for a few main reasons:

- With the increased number of small business owners who are getting closer to retirement age, the government desires privately funded pension plans help fund the retirement of America’s workers.

- Cash balance plans reduce taxable income in order to fall below the qualified business income (QBI) income threshold.

How Do Cash Balance Plans Work?

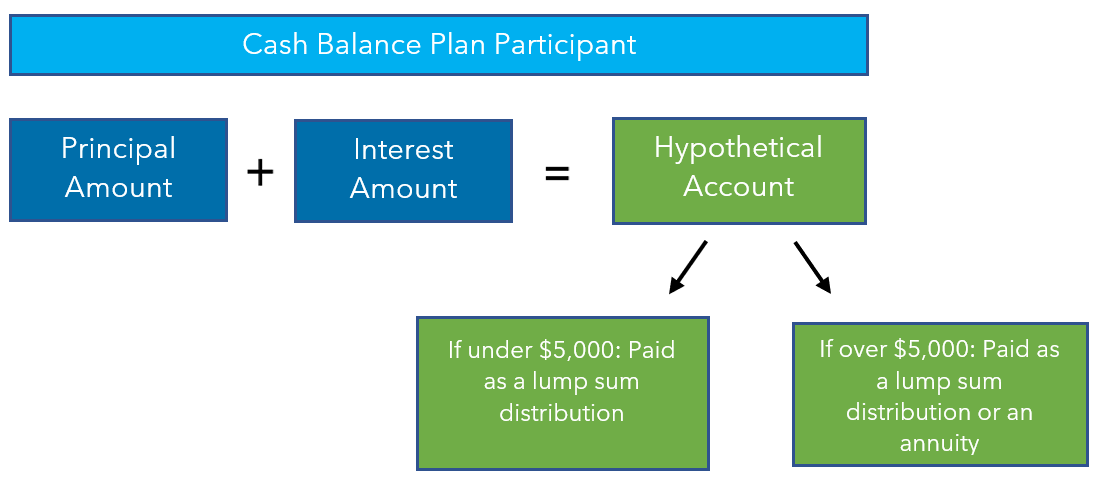

Under a cash balance plan, a “hypothetical account” is established for each participant. Hypothetical accounts are maintained by the cash balance plan administrator.

In general, the hypothetical account in a cash balance plan can be paid out as a lump-sum distribution to a participant upon death, disability, retirement or termination of service.

If the value of the account exceeds $5,000, the participant must also be given the option to elect payment of an annuity in lieu of a lump sum. Payment of a lump-sum distribution may be restricted if plan assets are not sufficient.

For this purpose, hypothetical accounts in a cash balance plan are valued using rates of interest and mortality prescribed by the IRS.

If assets are not sufficient, the employee may be restricted to receiving only the annuity form of payment or waiting until assets are sufficient to take a lump sum. If the contribution recommended each year is deposited, such restrictions rarely occur.

What are the Contributions to a Cash Balance Plan?

Each year, contributions and interest are credited to hypothetical accounts within a cash balance plan.

- Contributions are credited to hypothetical accounts each year in accordance with formulas in the plan document.

- Interest is credited to each hypothetical account each year based on a rate selected by the plan sponsor. Typically, this rate is a flat percentage between four percent and five percent, or it is based on the yield of an index, such as the 30-year treasury yield.

Contribution Amounts

The amounts which can be contributed from year to year are subject to complex non-discrimination testing.

Contributions made for highly-compensated individuals must bear a reasonable relationship to the amounts contributed on behalf of individuals who are not highly compensated.

When performing the nondiscrimination test, the cash balance contributions are combined with the contributions the company is providing in other retirement plans (typically a 401(k) plan). The amount of the required contribution depends on employee demographics.

Once a participant has worked 1,000 hours during a plan year, the employer must make a contribution on his or her behalf and cannot amend the plan to lower the amount of the contribution.

This is true even if the participant subsequently terminates employment during the year. For most full-time employees, 1,000 hours will be reached for a calendar plan year in June.

The cash balance plan can be amended periodically to permit different contribution levels, but some restrictions apply. Individual participants are not able to direct the investment of their accounts. Plan assets will be pooled and invested by the trustee (usually the company owner or owners).

Interest Amounts

The hypothetical accounts of the participants in the cash balance plan will be credited with interest at a rate guaranteed by the plan document. If the actual trust earnings exceed the guaranteed rate, the excess will be used to reduce future employer contributions.

This will not affect the amount credited to the participants’ accounts. That is, the account will increase according to the plan’s schedule, and the increase will be funded partially from employer contributions and partially from the excess earnings.

Typically, the employer contribution will be different from the amounts added to the participant accounts. This is primarily due to differences between the interest that is credited to the participant accounts and the return on the plan’s investments, but can also be due to vesting or changes in IRS required assumptions.

What Happens When a Cash Balance Plan Participant is Terminated?

Under cash balance plans, when a participant terminates his or her employment, he or she will be eligible to receive the vested portion of the hypothetical account balance.

A participant’s vested percentage is determined by the plan document and can be 0 percent for up to three years of service and then must be 100 percent upon completion of three years of service.

Are Cash Balance Plans Insured by the PBGC?

In general, the benefits in most cash balance plans are insured by the Pension Benefit Guaranty Corporation (PBGC).

Plans that are covered by PBGC insurance must pay a premium to the PBGC each year. If plan investments do not perform adequately or the plan sponsor chooses to make less than the recommended contribution, the plan could have unfunded benefit liabilities.

Unfunded benefit liabilities will increase the amount of premium that must be paid.

How Is the Tax Deduction Taken for Contributions to A Cash Balance Plan?

How the tax deduction for the contributions to a cash balance plan is taken depends on the entity of the plan sponsor.

The contributions for non-owners are always a company tax deduction. The owner contributions are either a company tax deduction or a personal tax deduction, depending on whether or not the plan sponsor is a corporation.

Learn More about Cash Balance Plans

Whether or not your company chooses a cash balance plan, selecting and designing the right retirement plan for your company can be a difficult task; with so many different options for benefit plan design, it can be hard to know what plan is the best fit for you.

Warren Averett’s Benefit Consultants are experts in designing employee benefit plans and helping companies streamline plan administration.

If you have questions about cash balance plans or if you want to know what plan may be the best fit for your company, contact Warren Averett Benefit Consultants.

This was originally published on January 17, 2019 and was most recently revised and updated on July 25, 2023.