The One Big Beautiful Bill Breakdown: Employers’ Tax Treatment of Compensation and Benefits

The One Big Beautiful Bill (OBBB) has updated several tax rules for compensation and benefits, adding new deductions and expanding credits for employers.

The Previous Tax Law

Overtime

Overtime has historically been taxed in the same way as regular wages, subject to federal income tax.

Tips

Tips have also been treated as regular taxable income for federal income tax purposes.

Business Meals

Employers could generally deduct 50% of the cost of meals provided to employees, such as meals served in on-site cafeterias or offered during late shifts, emergencies or business meetings. In some cases, the cost was fully deductible.

FMLA Tax Credit

Family and Medical Leave Act (FMLA) Paid Leave Tax Credit, which originated with the Tax Cuts and Jobs Act of 2017, was a temporary provision allowing employers to claim a percentage of wages paid to qualifying employees on paid leave. The credit had been extended multiple times since its inception, and it was scheduled to expire in 2025.

Employer-Provided Child Care Credit

This tax credit had allowed employers to claim up to $150,000 per year for providing certain childcare services on behalf of employees.

New and Final Law Under the One Big Beautiful Bill

Overtime

For tax years 2025-2028, W-2 employees (not independent contractors) can now deduct a portion of their overtime earnings from federal income, up to $12,500 for single filers or $25,000 for joint filers. This above-the-line deduction begins to phase out once income exceeds $150,000 (single) or $300,000 (joint).

Only the excess of the employee’s regular rate (the extra half-time in “time-and-a-half”) is eligible. To qualify, employees must receive “qualified overtime compensation” as defined by the Fair Labor Standards Act (FLSA). It is important that employers become familiar with the requirements of this provision.

There are still many questions for employers, including how to calculate overtime vs. ordinary pay and how withholding will be affected by this change. The IRS will be issuing guidance on or before December 31, 2025.

Business Meals

Also, starting in 2026, employers will no longer be able to deduct the cost of meals provided for their employees’ convenience. The only exceptions are meals provided in specific remote or hazardous work environments.

Tips

Starting in 2025, tipped workers can deduct up to $25,000 in tip income from their taxable earnings. The deduction phases out for incomes above $150,000 (single) or $300,000 (joint) and lasts through 2028.

FMLA Tax Credit

The FMLA Paid Leave Tax Credit is now permanent with expanded employee eligibility, including changing the minimum employee work requirement to six months with a minimum of 20 hours per week.

Businesses no longer need to be covered by FMLA to qualify, and the credit can apply to either wages paid during leave or insurance premiums for leave coverage.

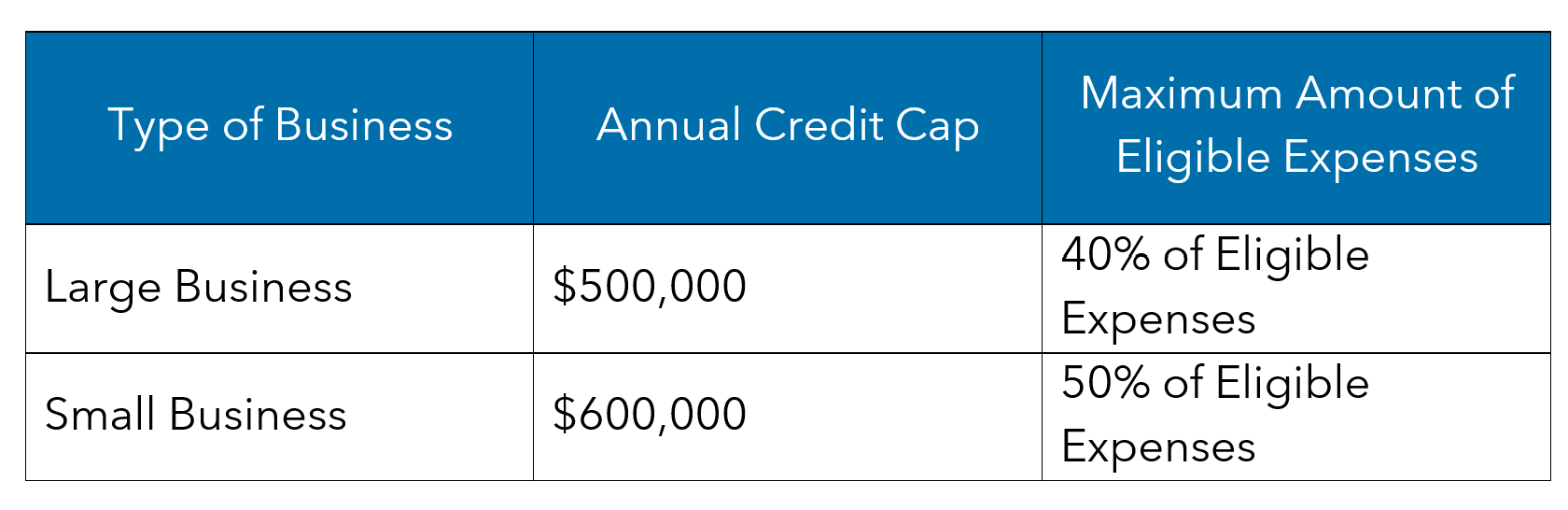

Employer-Provided Child Care Credit

Starting in 2026, the annual credit cap and eligibility requirements increase, encouraging broader use of this credit. The credit is equal to an amount of eligible expenses up to an annual credit cap.

What It Means for You

Employers should be making sure they are tracking overtime and tips correctly because there will be additional reporting related to these at year end.

In addition to the additional reporting, there are many changes that can affect businesses. It’s important to know how and when the OBBB changes will affect your business. The IRS is expected to release guidance on several of these provisions, and our team is watching for these updates to keep you informed.

To learn more about how the One Big Beautiful Bill and these specific provisions may impact you, contact your Warren Averett advisor.