3 Essential Tips for Succession Planning in the Construction Industry

For business owners, retiring from a construction business typically isn’t as straightforward as in other industries.

When they’re ready to retire, business owners in many other sectors can easily sell to financial buyers, such as private equity funds. But the construction industry is oftentimes less attractive to these buyers.

This, along with the family dynamics often involved in construction business transitions, adds an extra layer of complexity. Plus, the unique aspects of the construction industry itself make exits and transitions even more complicated.

That’s why proactive succession planning is crucial for a successful exit and a smooth retirement. It’s true for any business, but it’s especially nuanced for construction companies.

Here, we’ve outlined three essential considerations for owners in the construction industry to build out practical and strategic succession plans.

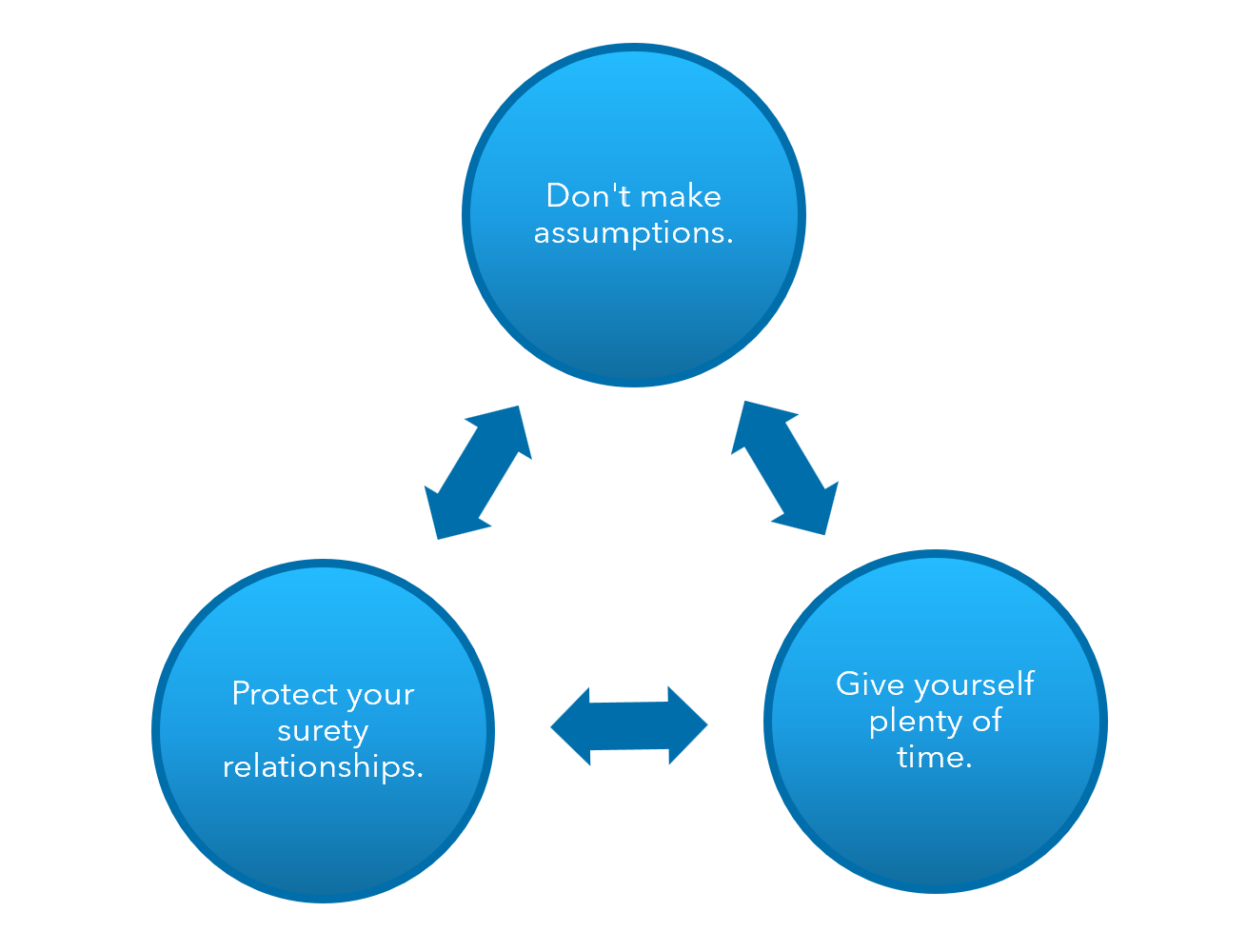

1. Don’t make assumptions.

While many construction companies are family-owned and operated for generations, an owner shouldn’t presuppose that your family will want to take over your business when you retire.

Your children might have different career goals or interests, so assuming they will want to take over the family business could lead to wasted time and resources if they decide to choose a different path.

Similarly, your employees may not be eager to become business owners. Even your highest performing team members simply may not be interested in taking the company’s reigns.

Running a business, especially in high-risk industries like construction, involves significant challenges and risks, and not all employees may want to take on the responsibilities and risks of ownership. Just because your employees excel in their roles doesn’t mean they will want to step into the owner’s shoes.

While having family members or employees take over a business is a great succession planning approach for many construction companies, it’s important to not operate under assumptions that these options are available. At the end of the day, it’s important to have intentional discussions that lead to a realistic succession plan which considers your family’s and your team’s actual interests and aspirations.

2. Give yourself plenty of time to educate and plan.

Succession planning should begin as soon as possible because it involves many people and many factors, some of which you might not anticipate. Even if selling your business seems like a far-off event, it’s best to begin the process (and revisit frequently) long before it’s a reality.

Starting early and discussing often gives you the time to handle all of the complexities effectively—and it gives you the flexibility to pivot appropriately when you need to. This ensures that your plan remains relevant and effective as circumstances change.

One of the most important long-term factors of succession planning that often goes overlooked is education. It’s critical to educate everyone involved in the transition (from your employees to your spouse) so that all parties understand their respective roles and responsibilities during and after the company’s transition.

This takes time, but it’s essential to ensure a smooth transition by making sure everyone knows what to expect and what is expected of them.

And while the company’s transitional activities are important, as a business owner, you should also allow yourself time to prepare for what comes after an exit from a personal perspective. This includes planning for your new role, lifestyle, goals and financial situation to ensure a successful and fulfilling transition to the next phase of your life.

3. Protect your surety relationships.

A hasty business succession can affect your surety relationships, which can impact the new owner group.

Oftentimes, a long-time owner has built the skills and reputation needed to establish a trusted relationship with the bonding company. So, when a long-time owner leaves a construction company suddenly, it can disrupt the organization’s bonding capacity, which then affects the company’s ability to secure projects and maintain financial stability.

That’s why it’s extremely important to allow as much time as possible to mentor and groom the management team so that the bonding company is confident that there are qualified and experienced individuals who are ready to assume the role of the previous owner.

If you’ve been personally guaranteeing the company’s debt or personally indemnifying bonds, educating the new owners needs to be a critical component of your succession plan. It’s important to intentionally prepare new stakeholders to take on this responsibility and risk so that your surety relationships remain stable throughout the transition.

New stakeholders may need time, resources and education to get comfortable with this role, and they may also need time to build adequate net worth to pledge as a personal indemnity on a bond.

The more time you have to manage this transition and build new relationships, the smoother the process will be.

Learn More about Succession Planning for Construction Companies

Construction companies come with unique characteristics that introduce complex dynamics into the succession planning process, so it’s important to work with an advisor you trust to set yourself and the company up for stable success in the future.

And it’s never too early to get started.

To learn more about succession planning for your construction company, or to get started with creating a customized plan, contact your Warren Averett advisor directly, or ask a member of our team to reach out to you.