What Is Included in a DCAA Compliant Indirect Rate Calculation?

Federal government contracts represent a lucrative and stable income stream, but compliance requirements and competition can be major hurdles for your success. Knowing what is included in a DCAA compliant indirect rate calculation can make the difference in securing these valuable contracts and scaling your business operations.

Direct vs. Indirect Costs

Before we get into the specifics of what is included in a DCAA compliant indirect rate calculation, it’s crucial to differentiate between direct and indirect costs.

A direct cost is one that is attributable to a single cost objective (e.g., contract, task, project or contract line item). These costs are generally required for contract performance. Typical direct costs include materials or equipment used exclusively for one cost objective. Direct costs also include the labor costs of workers who are able to identify their efforts to a single project.

But sometimes costs span multiple cost objectives. Costs that cannot be attributed to a single project or task are indirect costs. For example, consider a manager who supervises many contracts. In such a case, it would be impractical to attempt to divide his time among these projects to allocate their portion of his labor cost. Equipment used in multiple projects faces the same problem. To assist in this problem, these indirect costs are dealt with differently than direct costs.

Importance of Indirect Costs

If you only supply a single government contract and have no other non-governmental sources of income, then the distinction of direct and indirect costs can be immaterial. But for the majority of businesses, this is not the case, and the distinction is crucial.

The distinction between direct and indirect costs leads us to the important step of examining the indirect rate. This is an important concept in dealing with government contracts, from the proposal stage to the execution. The indirect rate gives valuable insight into a company’s financial circumstances, which is important when conducting business with the government. It also allocates permitted indirect costs to contracts in a fair and equitable fashion.

The purpose of the indirect rate is to allocate “pools” of indirect costs to more than one project. So the problems mentioned above involving the manager supervising multiple projects or equipment used in multiple projects are effectively addressed in this manner by allocating their costs across multiple cost objectives.

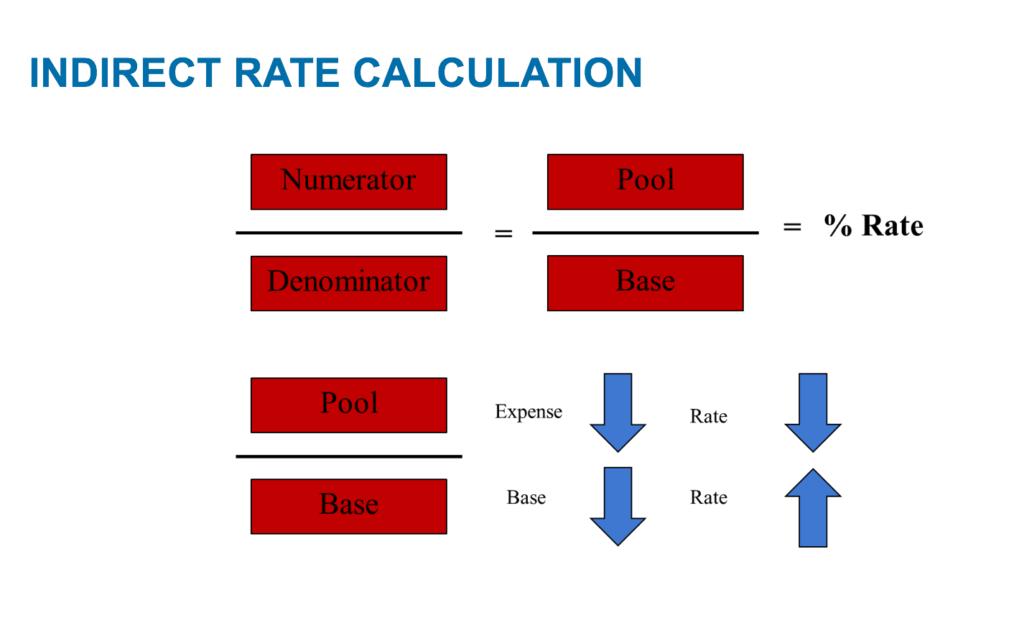

The indirect rate refers to the ratio of total indirect costs to the total base. The mathematical formula for an indirect rate calculation is provided below:

How the Indirect Rate Formula Works

As evident in the formula, the indirect rate is the result of dividing the indirect cost pool by the allocation base. As with any such equation, as the numerator (i.e., the cost pool) increases, the indirect rate also increases.

Conversely, reducing the cost pool yields a lower indirect rate. The denominator (i.e., allocation base) works in the opposite way. A higher base leads to a lower indirect rate, while a lower base yields a higher indirect rate.

Indirect Cost Pools

When the direct and indirect costs are established, it is important to develop homogenous indirect cost pools. This term implies that all indirect costs are grouped logically so that they have a similar relationship to the particular base that is being used for allocation. In other words, it would not be acceptable to combine indirect costs for running a service business with those of a manufacturing operation.

Two-Tier vs. Three-Tier

There are two distinct indirect rate structures commonly used that include the two-tier and three-tier structure.

Generally, a smaller business may find a two-tier setup sufficient, while many larger businesses opt for the three-tier structure. This distinction carries different cost allocation implications. For example, a two-tier rate structure generally features a much higher overhead rate because it includes fringe benefits, with the three-tier overhead rate generally in single digits due to the fact that fringe is treated as a separate rate.

A three-tier structure consists of Fringe, Overhead and General and Administrative (G&A) cost pools.

It is important to remember that total cost will be the same using both of these methods.

Fringe Costs

This type of indirect cost is relatively straightforward. It includes costs related to your staff, including fringe benefits (e.g., health insurance) and payroll taxes.

While fringe costs are rather simple to define, they represent the difference between two-tier and three-tier rate structures. In the three-tier system, fringe costs are considered a final pool. In a two-tier system, however, fringe costs are treated as an intermediate pool.

Overhead

Overhead includes the indirect costs involved in support operations or direct production. While these costs are directly related to projects, they cannot be allocated to one specific contract because they overlap across many projects. Overhead costs include the depreciation of equipment used on multiple projects, quality assurance and supplies that are shared across multiple contracts as well as costs like indirect labor and training.

General and Administrative Expenses (G&A)

These are expenses that arise from the overall operation of the business. G&A costs are not attributable to a single project because their functions span all projects for the company. These are expenses incurred through the functions of human resources, accounting and IT, to name a few.

Allocation Bases

It is important to allocate indirect costs in an equitable fashion. The proper allocation base represents the cause for the indirect costs to incur. There are generally accepted allocation bases established for each cost pool, as outlined below:

- Fringe – The fringe costs typically use total employee labor. So fringe is allocated to both direct and indirect labor activities.

- Overhead – The most common allocation base for overhead costs is direct labor.

- General and Administrative Expense – The proper allocation base for G&A is that which best represents the business activity. The Total Cost Input base is commonly used, which is the sum of direct costs, overhead, fringe, as well as unallowable direct and overhead costs.

Professional Help Is Available

A DCAA compliant indirect rate calculation is one of the many unique challenges that your business will face in pursuing government contracts. DCAA compliance can be a time-consuming and complicated ordeal, and it can be even more challenging without prior experience in dealing with government processes.

The experts at Warren Averett can guide you through the process to help you successfully meet all compliance requirements.