How to Vet Your 401(k) Third-Party Administrator (Five Questions to Ask)

For many plan sponsors, settling on the right 401(k) third-party administrator can be a difficult task.

One of the most confusing factors in selecting a provider is that the Employee Retirement Income Security Act of 1974 (ERISA) mandates that the fees paid to third-party administrators of an employee benefit plan must be “reasonable.”

But ERISA doesn’t provide a definition for the term “reasonable.”

Many times, the requirement for fees to be reasonable drives plan sponsors to choose the 401(k) third-party administrator that quotes the lowest fee. That has to be the most “reasonable” option, right?

It depends.

On one hand, selecting a discount provider provides assurance in complying with the reasonable fee requirement; but on the other hand, those third-party administrators that quote the lowest fees can also often be the least credentialed and have the least amount of technical experience.

The trouble with using a 401(k) third-party administrator that has less experience is that, unfortunately, fixing certain problems with employee benefit plans can cost far more in the long run than avoiding those errors in the first place.

That’s why it’s important to thoroughly vet 401(k) third-party administrators before you make a selection.

But how can you know when you’ve identified the sweet spot of reasonable fees and quality work?

Below, I’ve outlined five questions that you should ask your 401(k) third-party administrator before you commit to selecting a particular vendor—and why it’s important to know the answers.

Questions to Ask Your 401(k) Third-Party Administrator

Asking these questions will inform you about your 401(k) third-party administrator’s priorities, capabilities and expertise so that you can make the best decision for your 401(k) plan and for your employees.

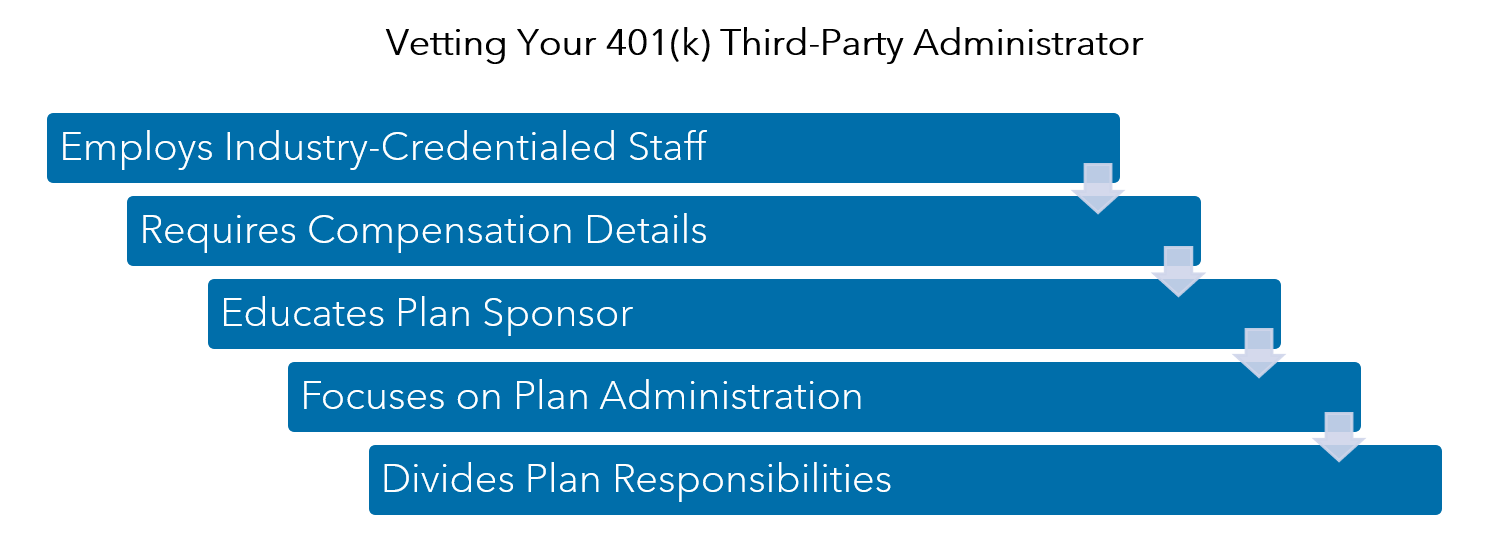

Question 1: Do you employ industry-credentialed staff?

Industry credentials by the American Society of Pension Professionals & Actuaries (ASPPA) or the National Institute of Pension Administrators (NIPA) require a candidate to pass a series of exams to show knowledge of the code.

These credentials demonstrate a commitment to knowledge in the complex field of employee benefit plans. So, a 401(k) third-party administrator that has staff with industry credentials is likely to be more experienced and informed.

In addition, there is continuing education required of individuals with these credentials, which means that these professionals are constantly learning more and more about this particular area.

Question 2: Do you require copies of W-2 and W-3s, as well as all components of compensation?

Compensation is compensation, right? Not necessarily.

Qualified employee benefit plans have multiple definitions of compensation, and these different definitions can be used for different purposes within the plan.

There are numerous reasons why a provider should reconcile back to W-2s. For one, it allows your 401(k) third-party administrator to verify all employees are accounted for and that deferrals are properly accounted for.

By providing the full details of compensation, your plan can take advantage of appropriate options.

Question 3: Do you take the time to explain the terms of the plan to ensure our team members fully understand?

In many cases, the task of providing information to a 401(k) third-party administrator falls on an employee who doesn’t have any knowledge of the plan.

By educating these employees, it raises awareness within the plan sponsor’s own organization, which creates efficiencies from the inside out.

Having a 401(k) third-party administrator that will make the effort to ensure your team understands can benefit your plan in the immediate work, but it’s also an investment in your employees for the future wellbeing of your 401(k) plan.

Question 4: Are you solely focused on plan administration services?

Finding someone dedicated to the complex rules of retirement plans to assist in the establishment and operation of your plan means that the services that you need are at the core of your 401(k) third-party administrator’s expertise.

Engaging a provider that primarily specializes in processing payroll or recordkeeping assets could mean that the task of assisting with the operation of your retirement plan won’t be their main focus.

Question 5: Do you bundle plan administration services?

Think about your plan administration having checks and balances. Bundled providers typically provide several services, but independent 401(k) third-party administrators divide plan responsibilities. Selecting an independent third-party administrator assists in holding other providers accountable.

An Example of One Discount 401(k) Third-Party Administrator’s Performance

As a demonstration of the importance of asking these questions, consider this true story from my past experience with a client.

The Background

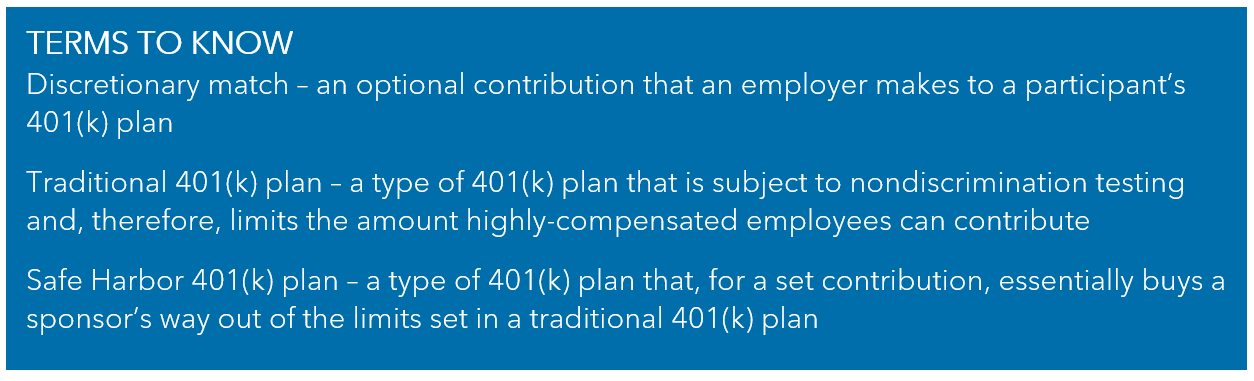

The plan sponsor was a small employer with 38 eligible participants, and plan assets were approximately $1.5 million. The plan is a safe harbor 401(k) plan that uses the 3% nonelective contribution to satisfy the required ADP/ACP nondiscrimination testing. The 401(k) third-party administrator was a regional discount provider.

The Issues

From 2013 until the end of the 2016 plan year, the plan sponsor allocated a discretionary match that was in violation of the safe harbor and plan’s limitations.

The contribution was pushed out of safe harbor status because the plan sponsor was matching on deferrals greater than 6% of compensation and because the match rate increased as the deferral rate increased.

Each of these issues on its own would have been enough to violate safe harbor standards.

As information was gathered, it was determined that since 2009, the plan sponsor was also excluding all part-time employees. The plan document in effect at the time stated that any eligible employee who performed six months of service would be eligible to participate in the plan.

These are issues that many experienced 401(k) third-party administrators have policies and procedures in place to catch.

The Resolution and Results

The IRS has prescribed methods to fix certain operational failures, but those methods are generally limited to the prior two years. This particular case exceeded that timeframe, so ERISA counsel was engaged to assist with bringing the plan back into safe harbor compliance.

In order to correct the errors caused by the discount third-party administrator’s lack of diligence, the employer had to make a large deposit into the plan, not to mention the legal and administrative fees paid to remedy the problems.

In the end, it cost this employer over $200,000 to correct the failures that could have been quickly corrected or prevented altogether with the right procedures set in place by the 401(k) third-party administrator.

How to Move Forward with Choosing a 401(k) Third-Party Administrator for Your Plan

You shouldn’t expect any 401(k) administrator to be perfect. There are, after all, humans behind the calculations.

But, with the right procedures and processes, errors should be caught within a short time frame. It’s important to ask what your current 401(k) third-party administrator is doing to prevent an issue from becoming a problem for your plan.

At the end of the day, a plan sponsor’s responsibility is to do what is best for the 401(k) plan.

Asking the questions outlined above and knowing the answers from your 401(k) third-party administrator can equip you to make an informed decision about your provider and protect your employee benefit plan.

Finding the right provider that will meet your needs can undoubtedly save you time, effort and money in the long run.

Warren Averett Benefit Consultants are experts in designing retirement plans, including 401(k) plans, and helping companies streamline plan administration. If you have questions about how to select the right 401(k) third-party administrator, or if you want to know what plan may be the best fit for your company, contact Warren Averett Benefit Consultants.

This article was originally published on March 15, 2019 and was most recently updated on March 3, 2022.