Manufacturing Financing: How To Avoid a “No” From the Bank When Growth Accelerates

Expansion can feel exciting, and company growth can escalate quickly. Credit looks available. Orders are up. Inventory is moving.

But then, what happens if the bank says “no” without much warning?

By the time you hear “no,” you’ve already invested time and resources in your growth plan. And reversing course isn’t simple. That is why planning ahead for financing is so critical, especially in the manufacturing industry, where receivables are higher, inventory commitments are larger and cash flow is tighter.

These factors can quickly affect how much financing you can access (and whether your bank views your growth as sustainable).

Understanding these pressure points is the first step toward avoiding surprises.

This guide walks through the four key areas to be aware of if you’re pursuing manufacturing financing—where growth creates pressure (and what to do before the pressure turns into a hard stop).

1. Communicate With Your Bank Often and Early

Banks base their decision on whether or not your company’s numbers fit their risk tolerance. You can’t always control that timing, but you can reduce surprises by bringing your bank into your plan early.

Bankers are relationship managers by title and by role. Treat them like partners in your planning.

Schedule a proactive briefing, and bring clean, current reporting. At a minimum, share:

- Your growth outlook

- Projected timing

- The expected impact on receivables, payables and inventory

- Plans to finance working capital through the growth phase

It’s also helpful to ask what information would help the bank stay comfortable as you scale.

Early, specific communication lowers the chance of an abrupt stop and shows the bank that you manage risk with intention.

2. Manage Growth From the Balance Sheet

When growth accelerates, strong sales and healthy margins can make everything look positive on the income statement. But the income statement alone won’t show whether your business can actually sustain that growth. Those answers lie in the balance sheet.

Your balance sheet can tell you how much cash is tied up in receivables, payables and inventory (and whether you’re liquid enough).

Start with reviewing your accounts receivable. Look at how quickly customers are paying and calculate your days receivable by dividing total receivables by average daily sales. If that number is climbing, cash is slowing down and borrowing costs are going up. This tells you whether growth is creating a cash gap that could force you to rely more on your line of credit.

Next, review your accounts payable. Calculate your days payable by dividing total payables by average daily cost of goods sold. If this number is shrinking, you may be paying vendors faster than necessary, which drains cash and increases pressure on your credit line.

Finally, compare your days receivable with your days payable. The difference between days receivable and days payable (known as “the spread”) shows whether cash is coming in faster than it’s going out. A wide spread means you’re financing growth with borrowed money. A smaller spread reduces borrowing and cuts interest costs.

Setting targets for these metrics and reviewing them often with your finance team can keep growth from turning into a liquidity crunch.

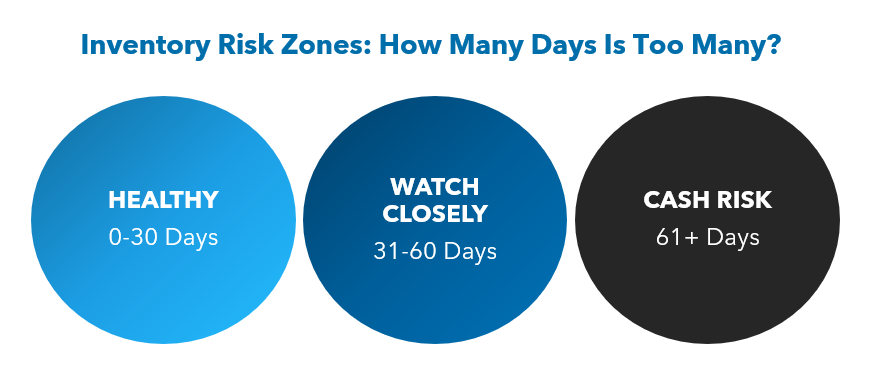

3. Control Inventory Before It Controls Your Cash Flow

Inventory can feel like an asset, but during rapid growth, it can quietly become a liability. Every extra pallet or part ties up cash. If you’re using a line of credit, that inventory is costing you interest every day. Managing it intentionally is critical to keep growth from straining your cash flow.

Align purchasing with real demand instead of optimistic forecasts. Overbuying creates excess inventory that locks up cash and adds borrowing costs. Then, identify slow-moving or obsolete items and act quickly. Price reductions or supplier returns can release capital that would otherwise sit idle.

For custom builds or long-lead projects, consider requiring customer deposits. This reduces the cash burden during production and helps you avoid financing the entire job yourself.

Consider tracking inventory with a simple dashboard that shows the days that inventory is on hand for key product lines. Reviewing this periodically helps prevent inventory from quietly eroding liquidity.

Purchasing controls matter as well. Growth can trigger overbuying, which compounds the pressure on working capital. Implement approval steps or limits on spending tied to forecasted demand to keep purchasing disciplined.

4. Plan Ahead for Customers Who Stretch Payment Terms

If large customers push payment beyond 90, 120 or even 180 days, it’s critical to plan for the impact on cash flow before it becomes problematic.

Begin by segmenting your receivables by customer and by payment terms to determine which accounts will take the longest to pay, and consider how that affects your cash position. Modeling the impact before you agree to extended terms helps you decide whether you can absorb the delay without borrowing more. Tie your purchasing cadence to expected receipts from those customers. If you know cash will not arrive for 120 days, avoid front-loading purchases that will sit on your shelves and add interest expense.

Collections also need structure. For long-term accounts, create a workflow that assigns responsibility, sets timing and tracks resolution. Staying proactive reduces surprises and keeps cash moving.

Consider early payment discounts only when the math works in your favor. If the discount costs less than the interest you would pay on borrowed funds, it can be a smart trade-off. If not, hold your ground.

Managing extended terms is about visibility and planning. When you know where the pressure points are, you can make decisions that protect cash flow and reduce reliance on debt.

Learn More About Sound Manufacturing Financing and Accounting

Growth can be exciting, but it should never outpace cash flow. When you manage receivables, payables and inventory with discipline, you create the liquidity to fund your plans and keep your bank confident in your strategy.

To learn more about reviewing your balance sheet and cash cycle, connect with your Warren Averett advisor directly, or ask a member of our team to reach out to you.