Do You Know Where Your Remote Employees Are? (and Why It Matters)

What constitutes a “remote” employee? If you’ve ever taken your computer or cell phone on a trip, you’ve been a remote employee. Since many people found themselves suddenly required to work remotely last year due to the pandemic, for many of us, our work location is wherever our computer is located.

Employers likely generally assumed that work was occurring at the employees’ place of residence, but due to varying state restrictions or health and financial considerations, employees may have temporarily or permanently relocated to rental properties at the beach, a friend or family member’s home, or a new home in another state.

And while it may seem to be of little consequence from the employee’s perspective, it can create significant tax issues for employers. Your employees’ work locations matter greatly when it comes to your company’s state and local taxes.

Although remote workforces are not unique to COVID times, the significant increase in more-than-temporary remote employment arrangements accelerated the need for states and companies to address related tax matters. And because it seems that remote workforces are here to stay, it’s even more important to know where your employees are and what the associated potential tax implications are.

Here are a few questions you can ask yourself to gauge where your company stands with the state and local tax issues associated with remote work:

- Is the remote arrangement a temporary arrangement just for COVID or for a week while the employee managed family matters, or is it anticipated it will be permanent?

- Does your company require employees to report changes in their work location?

- Is there a system in place to capture and analyze the impact of this data if it is gathered?

- Are you aware that there are some jurisdictions requiring the employer to continue payroll withholding based on the pre-COVID work location while the employee’s “temporary” work location also requires payroll withholding?

Why do my employees’ physical locations matter?

State and local income, sales and payroll tax laws govern how—and at what rate—businesses and workers are taxed. These laws vary significantly from state to state, even when those states share a border.

To add to that existing confusion, a handful of states issued temporary guidance allowing companies to have remote employees in the state during the pandemic without triggering a nexus requirement for one or more taxes. This has caused a firestorm of interstate commerce issues—some of which are being pursued in the court systems.

This means that the rise of remote work and dispersion of employees from the office is likely to complicate state and local tax issues for organizations because you may have nexus is places where you haven’t before.

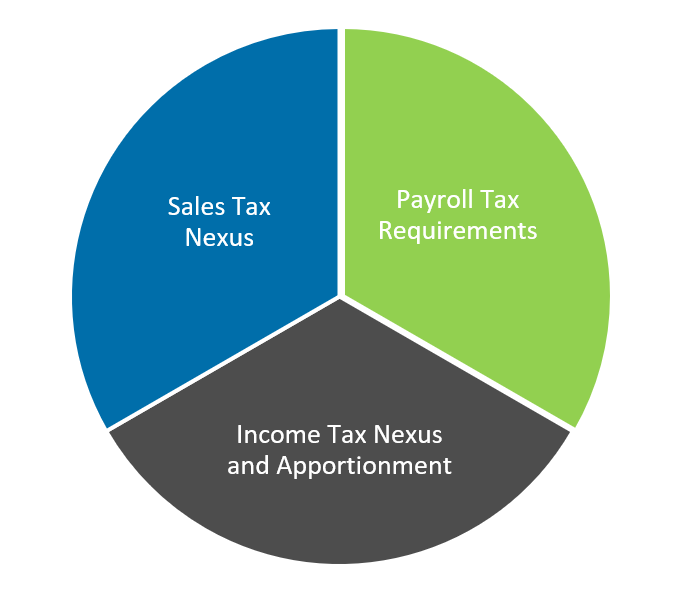

Planning for state and local taxes begins with understanding the following issues.

Sales Tax Nexus

States require companies to collect and remit sales tax in their state when the business has nexus (a taxable presence).

Having a physical presence of employees within a state has been and remains the gold standard for creating nexus for state taxes such as income tax, payroll tax and sales and use tax. The level of physical presence in a state that constitutes nexus has never been consistent; for some states, it’s one day, and for others it may be three days.

Until a few years ago, most states would base nexus on whether the employer had a physical presence in the state. But, since the 2018 U.S. Supreme Court decision in South Dakota v. Wayfair Inc., states can now determine nexus with either a physical presence or an economic presence.

Economic presence is the second test of nexus and is usually based on a certain level of sales in that state, but a single remote employee within a state’s borders can also be sufficient to establish nexus, creating an enormous burden for businesses to ensure they collect and remit sales tax properly.

If your business isn’t collecting sales tax on sales in that state, and it’s determined that you should have collected it, the tax likely comes out of your company’s pocket.

Payroll Tax Requirements

State income tax withholding and unemployment taxes typically follow the rules of the state where the work is performed. When employees come to your place of business for work, payroll withholding follows the rules of the state in which the business is located.

However, when employees work remotely in another state, the employer may need to withhold state income taxes and pay state unemployment taxes for the employee’s home state—assuming the employee is in one of the 41 states that assess state income taxes on wages and salaries.

The first step is determining where employees are working, whether they plan to be there temporarily or permanently, and whether the state has issued a waiver for employees working remotely due to the pandemic. For states with carve-outs for temporary work locations, it’s important to know what period of time is covered—the government stay at home mandate, the employer’s instructed stay-at-home period, or some other window of time.

Many states, including Georgia and Alabama, have announced waivers on state income tax withholding for employees working in the state temporarily due to the COVID-19 pandemic. However, not all states have issued guidance, and each state has its own guidelines. For businesses with employees working temporarily across several states, navigating the patchwork of rules and requirements can be daunting.

In some states, the threshold for deciding whether the employer must submit taxes for the state where the employee is working is based on days working in the state. In other states, that threshold is based on income. And even in other states, it’s based on a combination of the two.

Income Tax Nexus and Apportionment

As mentioned above, physical presence is the gold standard of nexus determination. Some states have minimum nexus threshold standards for payroll to help with temporary presence in state. Others state one day is sufficient, so it’s important to review the rules in each state to see if the company is creating nexus.

If your business has taxable nexus in several states, it can be difficult to determine how much business income is related to your business activity in each state – a process commonly referred to as apportionment of taxable income.

Many states base income tax apportionment on sales and assess income taxes only on the company’s share of sales into that state.

However, some states still factor payroll and property into their income tax apportionment calculations. In these states, employee payroll and the value of business property for employees’ use to perform services help determine what portion of the company’s profits get taxed in that state.

Again, every state has different rules for determining whether the business must pay compensation in the state where the employee is working rather than the business’s home state.

If the company is required to pay wages in another state, both the employee’s payroll and the property they use to perform their job may be sourced to the state where they work, which can significantly impact apportionment calculations.

Plan Now to Minimize Your Tax Burden

Waiting to evaluate everything at tax time can result in penalties, as well as potential tax overpayments. We recommend taking stock of your new remote employees and the state and local tax (SALT) laws they trigger now so you can begin planning strategies to minimize the tax burden.

If you have any questions about these or any other state and local tax issues, please reach out to your Warren Averett advisor, or have a member of our team reach out to you.