Cloud Computing and the R&D Tax Credit [Answers to Frequently Asked Questions]

The Research and Development Tax Credit (R&D) was first introduced in the 1980s, at a time when software developers typically rented time on off-site computers rather than owning their own equipment. As technology advanced, companies began purchasing their own equipment for software development, thus making computer rental expenses for the R&D credit largely irrelevant.

Fast-forward a few decades, and computer rental expenses have returned in a big way—this time in the form of cloud computing services, such as Amazon Web Services and Microsoft Azure—making it possible for companies using these services to save a bundle on their taxes.

Access our comprehensive guide about the R&D tax credit here.

Which cloud computing expenses qualify for R&D credits?

Only certain uses of cloud computing services count as qualified research expenses (QREs). As the IRS puts it in Treasury Regulations Section 1.174-2:

“Expenditures represent research and development costs in the experimental or laboratory sense if they are for activities intended to discover information that would eliminate uncertainty concerning the development or improvement of a product. Uncertainty exists if the information available to the taxpayer does not establish the capability or method for developing or improving the product or the appropriate design of the product.”

In short, an activity counts as research for purposes of claiming the tax credit if it relates to a new or improved product or process, is technological in nature and there is a level of technical uncertainty that can be eliminated through a process of experimentation.

For example, software developers can use a cloud environment to not only perform their development work, but also design a mirrored virtual environment to test their newly developed code to confirm that it doesn’t disrupt the functionality of the existing program.

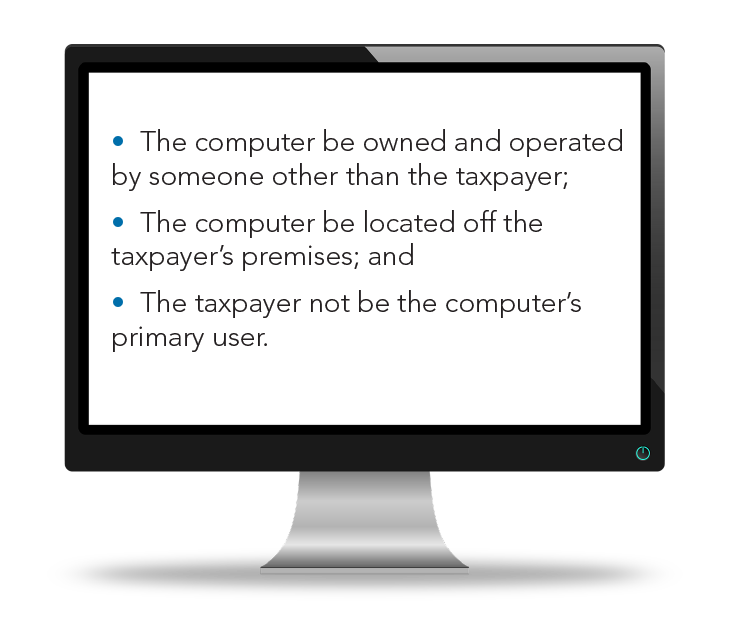

The IRS spells out the rules for ”computer rental expenses” as QREs in Treas. Regs. Section 1.41-2 (b)(4). The three basic requirements are:

- The computer be owned and operated by someone other than the taxpayer;

- The computer be located off the taxpayer’s premises; and

- The taxpayer not be the computer’s primary user.

Computer cloud rental services meet the above requirements because the business claiming the R&D credit is not the primary user of the cloud infrastructure, the servers for the rental service are in various locations and the cloud servers are owned by other companies, such as major service providers AWS, Azure and Rackspace.

Activities that typically do not qualify include hosting a web-based platform for customer use.

What should a business do to be able to claim the R&D credit for cloud computing?

Since many businesses use cloud computing services for a number of different activities, it’s crucial to track the expenses devoted specifically to hosting the testing and development environment, or pre-production, when using those services. Businesses will also want to retain records, including computing invoices or receipts, to meet the R&D recordkeeping requirements and simplify QRE calculations at tax time.

How should a business approach adding a new type of qualified research expense in order to claim the R&D tax credit?

Any time a business adds a new type of QRE to its R&D tax credit math, the business needs to maintain consistency by adding that expense to its “base period” – the period that’s contrasted with the current tax year to see how much R&D expenses have changed (and hopefully increased).

If a business starts claiming cloud computing expenses as QREs, it will also need to add in the appropriate amount of cloud computing and/or computer rental expenses to its base period. This keeps businesses from overstating their R&D expenses every time a new type of QRE is discovered.

How should a business adjust base expenses?

How your business will adjust your base expenses depends on which method you use to set your base for the R&D credit:

- Businesses using the Regular Method will adjust the fixed base percentage described in Regs. Section 1.41-3(d)(1) for tax years 1984 – 1988 to include computer rental expenses if the company chooses to claim cloud computing expenses as a QRE in the current tax year.

- Businesses using the Alternative Simplified Method (ASC) will adjust the three-year base in accordance with Regs. Section 1.41-9(c)(2). The company will need to add cloud computing expenses to the total QREs from the three taxable years prior to the current year when calculating its base amount.

Adjusting the base amount in either case can be tricky, involving a deep dive into financial records for the applicable years. This is a feat best tackled by an experienced accountant with specialized knowledge in the R&D credit.

Claiming Your R&D Credit for Cloud Computing Expenses

Because the Research and Development Tax Credit reduces your tax bill dollar-for-dollar, it’s a powerful way to save money for your business. Failing to claim the R&D tax credit could potentially lead to a lesser R&D tax credit benefit.

To learn more about how your business may benefit from the R&D tax credit, reach out to your Warren Averett advisor directly, or ask a member of our team to reach out to you.