No business wants to overpay on its taxes, but that’s exactly what happens when an eligible entity doesn’t take advantage of the research and development (R&D) tax credit.

Why are businesses overlooking such a significant tax saving opportunity?

It comes down to the fact that the R&D tax credit can be a confusing area to navigate. Without some technical knowledge, it may be difficult for businesses to determine their eligibility for the credit or to estimate the size of expected benefits. Of course, there are companies that are simply unaware of the credit as well.

That’s why we developed this guide—to address these issues by outlining the essentials in plain language from what the R&D tax credit is and how it’s calculated to how you can claim it and much more.

The R&D tax credit is a tax incentive designed to encourage research activities relating to developing or improving products, processes or software. It was introduced in 1981 by the federal government and was later made permanent by Congress through the Protecting Americans from Tax Hikes (PATH) Act in 2015.

The rules for the R&D tax credit are outlined in Section 41 of the Internal Revenue Code. Essentially, the credit is available for eligible expenses incurred on specific forms of research, known as qualifying research activities. Businesses across all industries that attempt to use scientific principles to innovate or make improvements could be eligible, which means the rewards aren’t just for large corporations with big R&D departments!

Benefits vary depending on the specific business.

For profit-making entities, R&D tax credits translate to dollar-for-dollar reduction in federal income tax liability. Eligible small businesses (ESBs) can apply them against alternative minimum tax (AMT) liability as well. Put simply, ESBs are businesses with an average of $50 million or less in gross receipts in the preceding three years.

A qualifying small business (QSB), on the other hand, can use some or all of its credits to offset payroll tax obligations up to a maximum of $250,000 until December 31, 2022; after that, the Inflation Reduction Act increased the election to $500,000. QSBs tend to be start-ups that are less than five years old and have current-year gross receipts of less than $5 million. The payroll tax offset effectively lowers staff costs without reducing headcount or salaries. It also means that you don’t have to be making profits to utilize tax credits.

Unused credits can be carried forward for 20 years and applied against future years’ taxes. This carry-forward feature is vital for maintaining cash flow at times when available funds are lean.

R&D tax credits free up resources for other uses too. In practice, companies typically get back 5-10 cents for every dollar spent in qualified expenses.

Estimating your R&D tax credit entitlement isn’t always straightforward because there are two methods to choose from—the regular research credit or the alternative simplified credit method.

Form 6765 (credit for increasing research activities) provides a series of steps to calculate your potential tax credits using either approach. You can work out your credits under both methods and then apply whichever gives you a better result.

The regular research credit is 20% of all qualifying expenditures for the current year that exceed a specified base amount. This base amount may involve complex and detailed calculations, depending on whether you’re a start-up or well-established business.

The alternative simplified credit is typically 14% of the difference between the amount of qualifying expenditures for the current year and 50% of the average qualifying expenditure for the preceding three years.

The R&D tax credit is only available for eligible expenses relating to qualifying research activities (QRAs). QRAs are those that meet the four-part test set out by the IRS.

Essentially, this means:

Note that there is no requirement for the experiment to succeed. Even failed or abandoned research could attract a tax offset.

If your activity satisfies the four-part test, you can claim qualifying research expenses (QREs) in connection with them.

The three main types of eligible expenses include salaries, supplies (such as materials and computer rentals) and contracted research. Bear in mind that your qualified expenses may be less than your cash outlay. For example, if your employees only spend half of their time on a qualifying project, then only half of their salaries would be included as a qualifying expense.

The IRS also provides a list of activities that cannot qualify for the R&D tax credit. For example, projects relating to management functions and social sciences are ineligible, as are activities conducted outside the U.S.

To get started with identifying potential qualifying expenses, take a look at the R&D costs in your financial accounting system. You may find it helpful to work with an experienced professional to determine the eligibility of your activities and expenses.

A common misconception preventing businesses from claiming the R&D tax credit is that the claim process requires too much effort. While some intentional planning is needed, the key is having the right documentation, which often includes records that businesses are already keeping.

Records that are useful in claiming the R&D tax credit typically include:

It’s important to establish a documentation process as soon as possible. If you ignore it until tax filing season, it may become more time consuming to address any gaps.

With the right documentation, your tax advisor will be able to walk you through claiming the R&D tax credit.

In addition to the R&D tax credit offered by the federal government, many states provide similar R&D tax incentives. If you are exploring your eligibility for credits at the federal level, it’s worth exploring whether your state offers incentives too, as you could be rewarded for things your business is already doing or are planning to do.

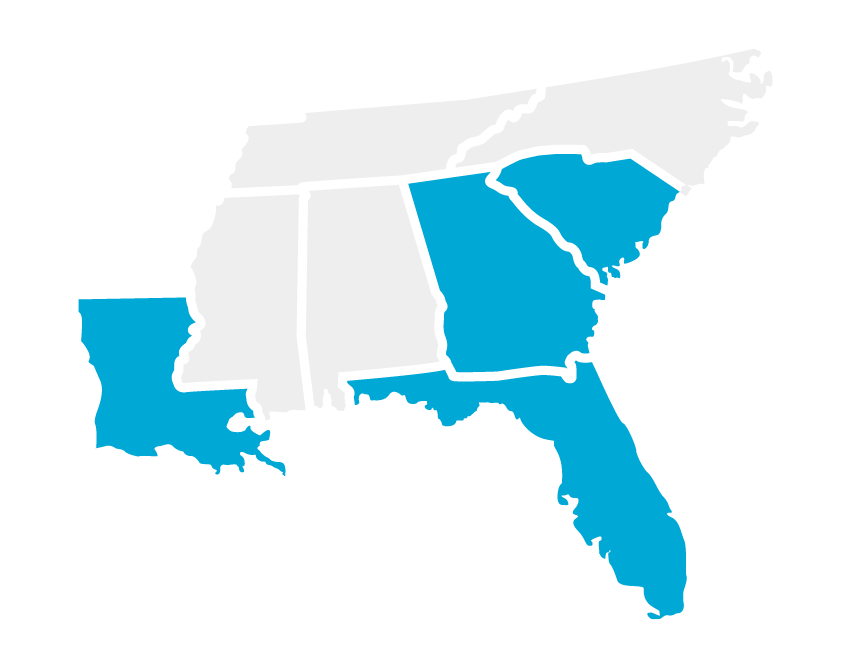

In the Southeastern states, Florida, Georgia, Louisiana and South Carolina offer an R&D tax credit. However, the credits differ from state to state.

Florida’s income tax applies to C-corporations only, and the credit is 10% of qualifying expenses over a base amount.

To be eligible, the R&D activities must be conducted within Florida, and they must be carried out by a business in specific industries. For a full list of eligible industries, click here.

The credit is capped at 50% of the corporation’s tax liability, and there is a statewide cap of $9 million in credits each year.

Unlike Florida’s R&D tax credit, Georgia’s R&D tax credit is open to all business entities. Again, the credit is 10% of qualifying expenses over a base amount, but the base amount is derived differently.

The credit can be used to offset up to 50% of the taxpayer’s income tax liability with any remaining credits either carried forward for up to 10 years or applied against payroll taxes.

Louisiana’s R&D tax credit reduces income or franchise tax and is available for C-corporations, S-corporations, LLCs and partnerships. The credit is calculated as a percentage of qualified research expenditures incurred in Louisiana. This percentage ranges from 5% to 30%. Unused credits can be carried forward five years.

The South Carolina R&D tax credit is five% of expenses that meet the requirements for the federal R&D tax credit. The research activity must be conducted within the state, and the credit is capped at 50% of the taxpayer’s tax liability. Unused credits can be carried forward for up to 10 years.

Alabama, Mississippi and Tennessee do not currently offer an R&D tax credit. North Carolina repealed its program in 2016, though businesses with R&D tax credits carried forward from previous years can continue to use them.

The federal R&D tax credit is available to all businesses that apply innovation. Below are examples of how businesses in some industries might qualify for the federal incentive.

In the sales and design phase, a qualifying activity may relate to developing a new product or improving an existing product. When in production, creating specialized tools or changing engineering processes may be eligible. In the distribution phase, crafting new packaging materials or ways of packaging could qualify.

Examples of qualifying activities include finding ways to meet a new building code, reducing excessive noise or constructing a greener building.

Improving exploration, mining and cleanup processes by experimenting with technology, equipment or procedures could be eligible.

Design, lab work, analysis and refinement of new products or experiments may qualify for the R&D tax credit.

Experimenting with new safety equipment or more efficient engines, improving loading equipment or processes, enhancing dispatching or routing technology could potentially qualify.

Software development activities that enable a company to interact with a third party, such as a customer or vendor, are no longer subject to additional qualifying criteria. As a result, businesses in all industries can claim the R&D tax credit for these activities more easily.

Here are the most frequently asked questions about the R&D tax credit and some quick answers to them.

Typically, 5-10 cents on each dollar of qualified expenses.

If you don’t have an income tax liability, you can carry forward your credits for up to 20 years. Qualifying Small Business can also apply credits against payroll tax, up to a maximum of $250,000 until December 31, 2022, and then up to $500,000.

Yes, if you are an eligible small business.

There is no cap on the federal R&D tax credit, but some state R&D tax credits may be subject to a maximum.

Typical benefits from tax savings include improved cashflow, lower payroll costs and increased competitiveness.

Yes. You can typically claim them by amending your income tax return if it was filed within the past three years.

You make a formal claim by filing Form 6765 with your income tax return. You should have a documentation process in place throughout the year to ensure you have sufficient evidence to support your claim.

You will need financial records showing the money you paid, business records demonstrating the activity’s purpose and a breakdown of qualified vs. non-qualified activities for expenses that relate to multiple purposes.

Three main types of expenses are eligible: salaries, supplies (such as materials and computer rentals) and contracted research. However, your qualified expenses may be less than your cash outlay.

These are research activities that meet the four-part test set out by the IRS, meaning they’re conducted for a qualified purpose, eliminate uncertainty, involve a process of experimentation and are technical in nature.

Within this guide, we have provided you with a summary of what you need to know about the R&D tax credit and links to numerous resources where you can gain in-depth insights.

Some of the topics covered are easier to understand than others. If you have further questions or would like information tailored to your specific situation, it’s important to engage an experienced professional who can provide you with accurate advice.