The Three 401(k) Tax Credits All Small Businesses Should Know

Opening a retirement plan for your organization’s employees is more practical than ever before.

Thanks to the SECURE 2.0 Act of 2022, tax credits have been expanded for businesses that establish, contribute to and automatically enroll employees in company-sponsored retirement plans, including 401(k) plans.

401(k) Tax Credits for Small Business

There are three 401(k) tax credits that all small business owners should know about when optimizing their retirement plan strategies: the Retirement Plans Startup Costs Tax Credit, the Employer Contribution Tax Credit and the Automatic Enrollment Tax Credit.

Retirement Plans Startup Costs Tax Credit

The Retirement Plans Startup Costs Tax Credit is designed to reward and encourage small businesses for establishing new 401(k) plans. To qualify for this credit, businesses must meet specific eligibility criteria:

- The business must have 100 or fewer employees who received at least $5,000 in compensation in the preceding year.

- At least one participating employee must be a non-highly compensated employee (NHCE).

- The business cannot have maintained a retirement plan for the same employees in the past three years.

The Retirement Plans Startup Costs Tax Credit covers various costs associated with setting up a new retirement plan, such as legal and administrative expenses and educating employees about the new plan. (It’s important to note that businesses cannot claim both this 401(k) tax credit and a tax deduction for the same expenses.)

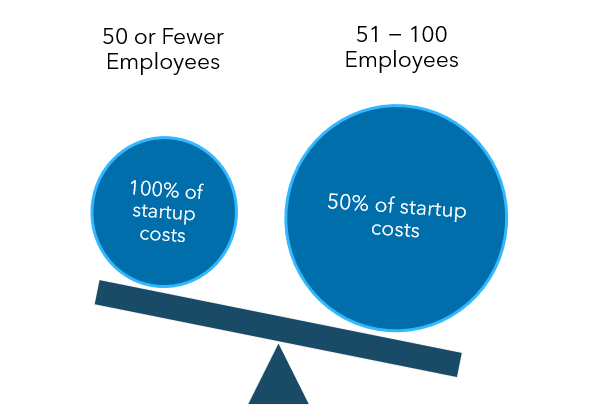

Businesses with 50 or fewer employees can claim 100% of eligible startup costs, while businesses with 100 or fewer employees can claim 50% of eligible startup costs. The tax credit (up to a maximum of $5,000 per year) can only be claimed for the first three years of the 401(k) plan.

Remember to maintain proper documentation of all expenses relevant to your 401(k) startup.

Employer Contribution Tax Credit

For tax years beginning after 2022, the Employer Contribution Tax Credit benefits small businesses that make employer contributions to a new 401(k) plan.

To qualify for this 401(k) tax credit, businesses must have 100 or fewer employees who received at least $5,000 of compensation in the prior year. However, the credit is reduced by 2% for each employee over 50, impacting the total credit available.

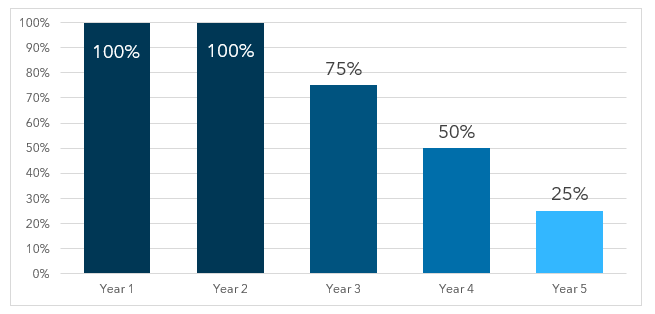

The credit is worth up to $1,000 per employee per year for up to five years, but the percentage of employer contributions used to determine the credit amount phases down over five years: according to the following schedule:

- Year 1: 100%

- Year 2: 100%

- Year 3: 75%

- Year 4: 50%

- Year 5: 25%

When calculating the Employer Contribution Tax Credit, only consider contributions made for employees earning $100,000 or less in compensation. Contributions for participants with compensation over $100,000 do not count towards the credit.

The credit does not apply to employer contributions to a defined benefit plan, but any employer contributions not eligible for the tax credit can still be used for tax deduction purposes.

Automatic Enrollment Tax Credit

SECURE 2.0 also created an Automatic Enrollment Tax Credit to incentivize businesses to incorporate automatic enrollment features into their retirement plans.

Any 401(k) plan adding an automatic enrollment feature qualifies, but the auto enrollment feature must meet the IRS’s Eligible Automatic Contribution Arrangement (EACA) requirements. An EACA uniformly applies the plan’s default automatic contribution percentage to all employees. The Automatic Enrollment Tax Credit is specifically tied to implementing the automatic enrollment feature rather than covering any associated costs.

Businesses with 100 employees or fewer during the previous tax year can claim a $500 tax credit (in total each year) by adding auto enrollment to a new or existing 401(k) plan. This 401(k) tax credit can be claimed for the first three years following the implementation of the automatic enrollment feature.

For employers with more than 10 employees, starting in 2025, automatic enrollment will be required for all new retirement plans.

Documentation to support claiming the tax credit includes proof of the date when the plan was adopted or amended and evidence that they’ve implemented the automatic enrollment feature.

Maximize Your 401(k) Tax Credits With Help From a Consultant

While each of these tax credits is valuable on its own, combining them can make offering retirement benefits much more affordable while also strengthening your company’s talent acquisition and retention strategies—making it essential to understand your eligibility and the credit details.

The sooner you begin offering these benefits, the sooner your employees can begin participating and saving for retirement. However, there are nuances to determining whether the credits are available to your business and calculating your credit.

For personalized guidance and to ensure the best decision for your company’s retirement plan needs, contact Warren Averett Benefit Consultants. We can assist you in evaluating your eligibility for 401(k) tax credits and determining which plan type fits your company’s goals.