401(k) Automatic Enrollment: Tax Credit Questions Answered

The Setting Every Community Up for Retirement Enhancement (SECURE) Act 2.0 brought significant changes to retirement planning, including introducing a tax credit for plans that have an automatic enrollment feature.

What Is the 401(k) Auto Enrollment Tax Credit?

The auto enrollment tax credit is designed to encourage small businesses to adopt automatic enrollment features in their retirement plans by offsetting the costs associated with implementing and maintaining a 401(k) plan.

The tax credit provides eligible employers up to $500 per year for a maximum of three years, meaning a business can receive a total of $1,500 in tax credits over three years.

By encouraging companies to implement automatic enrollment features, lawmakers hope to increase the number of employees actively participating in retirement plans.

What Qualifies a Business To Be Eligible for the Auto Enrollment Tax Credit?

To qualify for the auto enrollment tax credit, businesses must meet specific criteria outlined under SECURE 2.0. These criteria ensure that the tax credit targets small businesses that can most benefit from the financial incentive.

The eligibility requirements are as follows:

- Employee size and compensation: Your business must have 100 or fewer employees who received at least $5,000 in compensation in the preceding year.

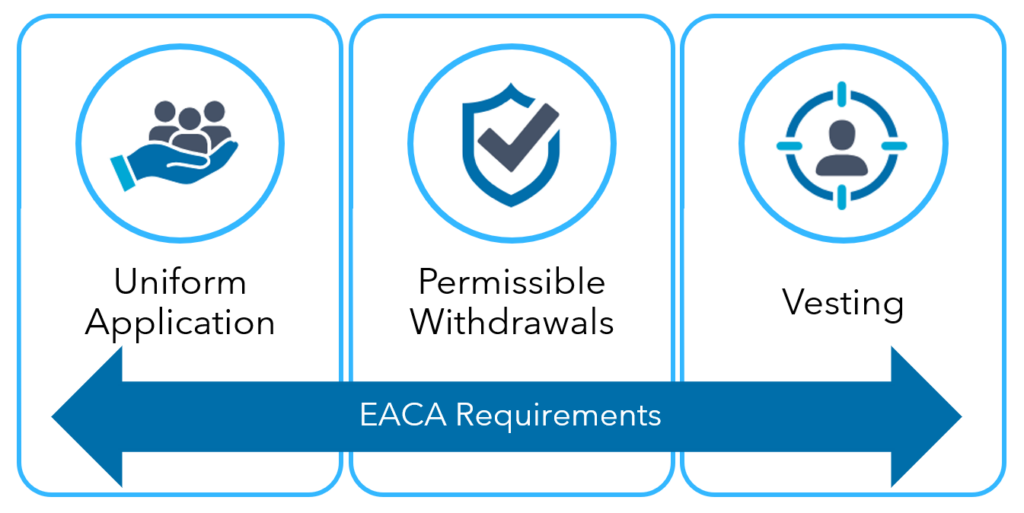

- 401(k) automatic enrollment requirements: The automatic enrollment feature must meet the Eligible Automatic Contribution Arrangement (EACA) requirements to qualify. These requirements include:

- Uniform application: Automatic enrollment must be uniformly applied to all eligible employees after giving them the required notice.

- Permissible withdrawals: Employees must be allowed to withdraw their automatic contributions within a specified period, typically 30 to 90 days, without facing penalties.

- Vesting: The employees vest immediately in their contributions. After two years of service, employees must be 100% vested in the employer automatic contributions.

The auto enrollment tax credit is available for both newly established and existing 401(k) plans, but it’s important to note that companies starting a new retirement plan may be able to pair the auto enrollment tax credit with other 401(k) tax credits to maximize their tax benefits.

How Is the EACA Automatic Enrollment Feature Added to a New or Existing 401(k) Plan?

Plans must meet the EACA requirements to qualify for the auto enrollment tax credit. Existing 401(k) plans that do not already meet these requirements would require a formal plan amendment to incorporate an EACA automatic enrollment feature. Plan sponsors should consult your retirement plan administrator or legal advisor to ensure the amendment complies with regulatory requirements.

A new 401(k) plan can incorporate the EACA feature during the initial design phase. This involves outlining the 401(k) automatic enrollment procedures, default contribution rates and other necessary details in the plan document from the outset.

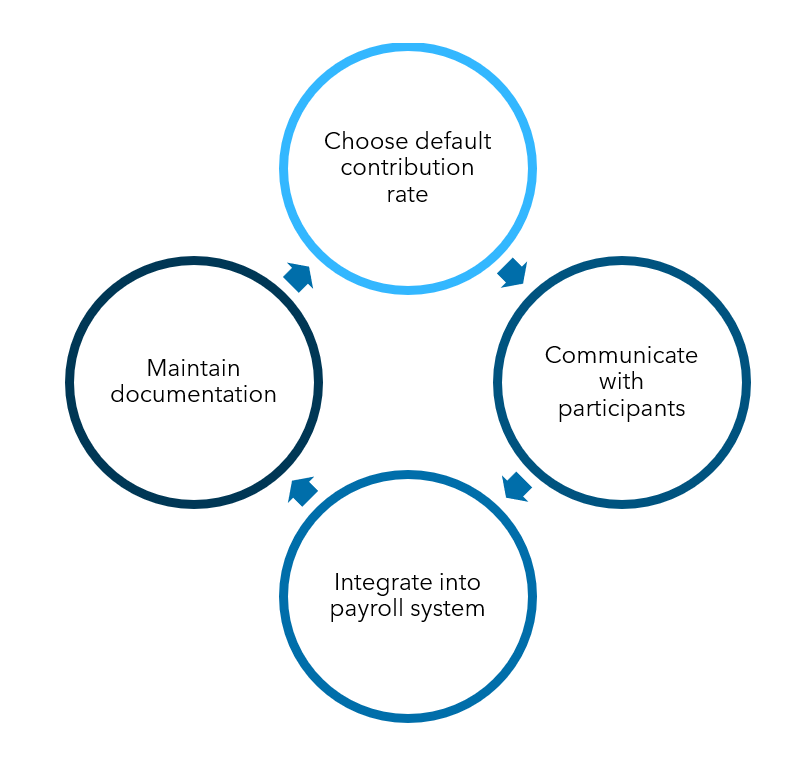

To meet the EACA requirements (and thereby qualify for the auto enrollment tax credit), new and existing plans must:

- Choose a default contribution rate.This rate is typically a percentage of the employee’s compensation and can be designed to gradually increase over time, encouraging higher savings rates. The minimum contribution rate is 3%.

- Communicate with participants. Provide employees with detailed information about the 401(k) automatic enrollment feature, including how it works, the default contribution rate, the right to opt out, how to opt out, how to change the contribution rate, how to make investment elections and the permissible withdrawal period.

- Integrate the automatic enrollment feature into your payroll system. You will need to set up and confirm processes to ensure the right contributions are deducted from employees’ paychecks.

- Maintain proper documentation. To promote compliance and prepare well for audits, it’s important to maintain records of plan amendments, participant communications, payroll adjustments and other relevant documentation supporting the administration of the 401(k) automatic enrollment feature and compliance with EACA regulations.

How Does Incorporating a 401(k) Automatic Enrollment Feature Benefit Sponsoring Companies?

Beyond the auto enrollment tax credit, implementing an automatic enrollment feature offers several benefits to sponsoring companies.

Automatic enrollment significantly boosts employee participation rates in retirement plans, and it simplifies the onboarding process. Rather than requiring new hires to take action to enroll in the retirement plan, they are automatically included, reducing administrative burden and ensuring immediate participation.

Additionally, starting in 2025, all new 401(k) plans for employers with more than ten employees will be required to include automatic enrollment features. So, companies can proactively comply with this upcoming mandate by incorporating automatic enrollment now while also leveraging the tax credit.

How Can Businesses Ensure Compliance With 401(k) Automatic Enrollment Regulations Beginning in 2025?

As the 2025 deadline for mandatory automatic enrollment in new 401(k) plans approaches, businesses should take proactive steps to ensure compliance.

First, ensure you thoroughly understand the specific requirements of the 401(k) automatic enrollment regulations under SECURE 2.0, including the criteria for eligible employees, default contribution rates and permissible withdrawal options.

Keep detailed records of plan amendments, participant communications, contribution rates and any changes to the plan to help demonstrate compliance during audits, and consider partnering with a quality third-party administrator to ensure compliance and optimize your 401(k) plan.

Learn More About the Auto Enrollment Tax Credit

At Warren Averett, our experts can provide comprehensive guidance and support to help you implement automatic enrollment features, leverage the auto enrollment tax credit and comply with upcoming regulations.

Connect with an advisor to ensure you are maximizing the benefits of your retirement plan, preparing for the 2025 changes and taking advantage of available tax credits to offset the cost of offering retirement benefits.