3 Things To Consider for Your Company’s Employee Benefit Plan Compliance in 2025

The SECURE 2.0 Act, which was signed into law at the end of 2022, introduced sweeping changes to retirement plans. Some provisions became effective immediately, while others became effective later.

Through 2024, the legislation allowed for higher catch-up contributions, changed the required beginning date for required minimum distributions and allowed for emergency distributions and tax- and penalty-free rollovers from 529 accounts into Roth IRAs, among other provisions.

Now, businesses offering 401(k), 403(b) or other qualified plans in 2025 and beyond need to be aware of the next wave of provision effective dates to avoid penalties and ensure plan integrity.

Below are three key considerations to help you proactively manage compliance and reduce risk in your employee benefit plan in 2025.

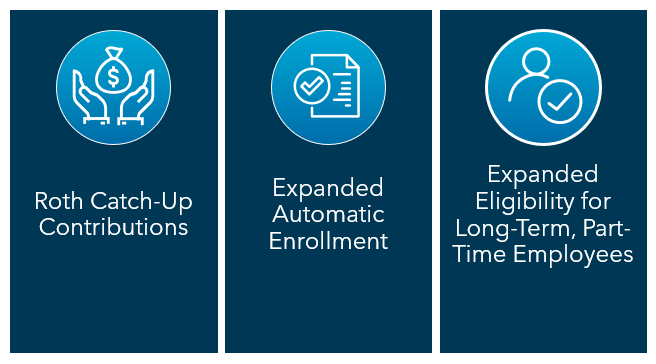

Roth Catch-Up Contributions

Perhaps the most significant change that has yet to occur, SECURE 2.0 made substantial changes to catch-up contributions.

Starting with plan years beginning after December 31, 2025, employees age 50 and older who earned more than $150,000 in prior-year W-2 wages from the employer sponsoring the plan will be required to make their catch-up contributions on a Roth basis.

These contributions will be included in their taxable income but will grow and be distributed tax free, assuming they meet the Roth holding period requirements.

In addition, SECURE 2.0 requires plan sponsors with an eligible participant subject to the new Roth catch-up contribution rule to allow all other eligible participants in the plan who make catch-up contributions to make them on either a pre-tax or Roth basis.

If your plan does not currently allow Roth contributions and you wish to continue to allow catch-up contributions, you must amend the plan to permit Roth deferrals by January 1, 2026. For safe harbor plans, the deadline is no later than December 1, 2025.

Rules for Self-Employed Individuals and Partners

Qualification for the mandatory Roth catch-up contributions depends on FICA wages, so individuals who do not have FICA wages from the plan sponsor will not have restrictions on their catch-up contributions, regardless of their earnings. This includes sole proprietors and partners in a partnership who have only self-employment income. Individuals without FICA wages have the option to designate their catch-up contributions as either pre-tax or Roth.

Higher Catch-Up Contributions for Ages 60-63

Beginning in 2025, individuals aged 60 to 63 may contribute a higher catch-up amount. The increased limit is 150% of the otherwise applicable dollar limit for the taxable year ($11,250 for 2025). That figure is indexed for inflation each year.

These enhanced limits provide an opportunity for late-career participants to significantly bolster retirement savings.

Expanded Automatic Enrollment

Beginning in 2025, 401(k) and 403(b) plans established after December 29, 2022, must include automatic enrollment and automatic escalation features, unless they qualify for an exception. There are several exceptions to this requirement, including those for plans sponsored by churches, governments and collectively bargained groups.

Employees must be automatically enrolled at a deferral rate of at least 3% (but not more than 10%), with an automatic annual increase of 1% until the deferral rate reaches a minimum of 10% and a maximum of 15%.

Expanded Eligibility for Long-Term, Part-Time Employees

Beginning January 1, 2025, SECURE 2.0 modified the definition of long-term, part-time (LTPT) employees to require the inclusion of more employees in an employer’s 401(k) plan.

A long-term, part-time employees are any employees who work at least 500 hours but fewer than 999 hours for two consecutive years starting in 2025. Once they meet that service requirement, employers must permit them to participate in the plan no later than the first day of the plan year or the first day of the seventh month of the plan year, essentially January 1 or July 1 for plans operating on a calendar year.

Plan sponsors can still allow participants to meet minimum age requirements. For example, many plans require participants to be at least age 21 to participate in the plan.

Plan sponsors must ensure that all long-term, part-time employees who meet these service thresholds are permitted to make salary deferral contributions, even if they are not eligible for employer matching or profit-sharing contributions.

These employees are not required to be included in nondiscrimination testing for certain purposes, but they must still receive proper enrollment notices and access to plan features.

Stay Proactive To Stay Compliant

Additional SECURE 2.0 provisions will roll out in 2026, including requirements for paper statements and deferral of tax for certain sales of employer stock to ESOPs. As retirement plan rules continue to evolve, employers must stay on top of implementing required provisions and avoiding compliance risks.

To protect your plan and participants, review your plan documents regularly and coordinate with your service providers to ensure your plan documents and payroll systems are up to date. For tailored guidance and implementation support, connect with a Warren Averett advisor. We’re here to help you understand the rules and take steps to implement necessary changes.

This article was originally published on August 7, 2025 and was most recently updated on November 18, 2025.