5 Steps to Make a Business Interruption Claim

Has your organization suffered damage to the business and its finances?

While hurricanes and other natural disasters are most often associated with this damage, a number of different scenarios and events can create a hardship for companies.

It’s important to know what your options are and how to respond in order to facilitate the fastest and fullest recovery possible. Business interruption claims are just one way that your business may be able to receive financial relief after a disaster.

What is a Business Interruption Claim?

A business interruption claim is a claim filed by an organization with a qualifying business interruption insurance policy, which is designed to help organizations protect against and recover from lost earnings attributed to a covered event. Most business interruption policies are add-ons to property damage insurance.

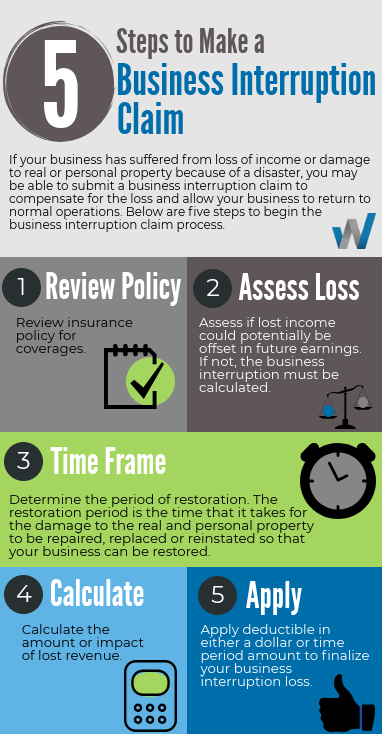

If your business has suffered from loss of income or damage to real or personal property resulting from a disaster, you can submit a business interruption claim to compensate for the loss and to allow your business to return to normal operations.

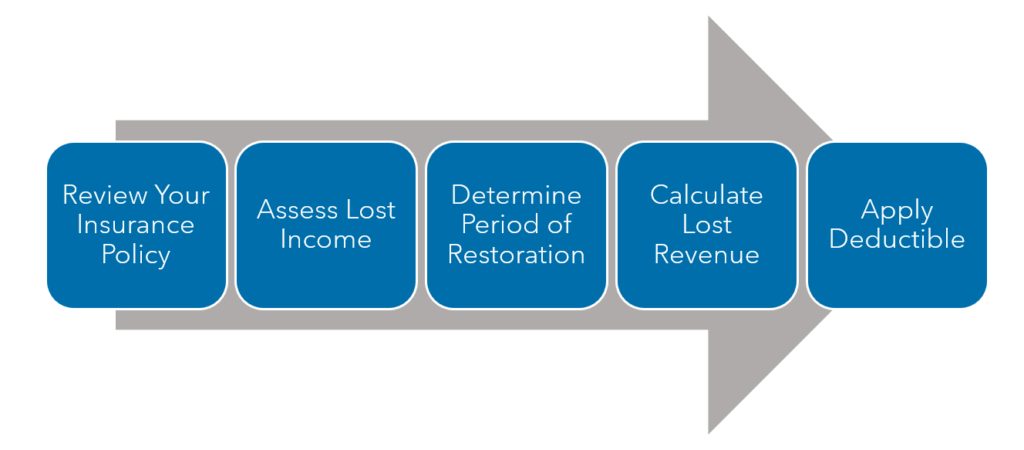

Below are the five basic steps you’ll need to take in order to make a business interruption claim.

Business Interruption Claim Step 1: Review your insurance policy for coverages.

The first step in making a business interruption claim is to review your insurance policy.

Business interruption policies typically only cover damage from insured risks, which vary with the type of policy.

Some policies individually and specifically name each risk insured against (named perils policy), whereas other policies might assume that all risks not specifically excluded are covered (all-risk policy).

It’s important that you look for a business interruption endorsement that defines your coverage and/or the period of coverage. Your Commercial Package Policy (CPP) may not cover the specific risk or may limit the period of loss.

Business Interruption Claim Step 2: Assess if lost income could potentially be offset in future earnings.

Lost income from business interruption can be tricky. The purpose of a business interruption policy is to protect you against lost earnings caused by the suspension or partial suspension of business operations due to a covered event, such as a disaster.

Lost income that is not offset by future earnings is subject to business interruption coverage. If it is not offset by future earnings, the business interruption must be calculated.

Business Interruption Claim Step 3: Determine the period of restoration.

The restoration period is the time that it takes for the damage to the real and personal property to be repaired, replaced or reinstated, so that your business can be restored.

Business interruption policies generally provide benefits during the period of restoration. The period usually begins on the date of the incident; however, some cases may require a waiting period of 72 hours before the period of restoration starts.

The period of restoration usually ends when the business is restored to its previous position or when it could have been restored with the exercise of due diligence. The period of restoration is a critical component of a business interruption loss calculation and, at times, a contentious area of the business interruption claim. Your policy should define the restoration period.

Business Interruption Claim Step 4: Calculate the amount or impact of lost revenue.

Your insurance policy generally defines how to calculate your actual loss sustained, as well as all that the term encompasses. Considerations of lost sales, earnings, projected sales and other costs must be carefully evaluated.

Is your loss supported by production records or inventory records, or do they include extra expenses that may or may not be recoverable? The policy should define what is recoverable.

Business Interruption Claim Step 5: Apply deductible in either a dollar or time period amount to finalize your business interruption loss.

The deductible percentage is important to finalize the business interruption claim and should be included in the declaration page of your policy.

Learn More about How to Make a Business Interruption Claim

Warren Averett has the depth of knowledge and expertise to assist with business interruption claims, and our experts have assisted many businesses through recovering their businesses from disasters.

Warren Averett has the depth of knowledge and expertise to assist with business interruption claims, and our experts have assisted many businesses through recovering their businesses from disasters.

Our team of advisors can review a smaller business interruption claim before it’s submitted or, for more involved claims, calculate the business interruption loss for your claim. Our experts understand that each case and policy is unique, and we can help with the option that’s best for your business.

If you have questions about business interruption claims, please contact your Warren Averett advisor or ask a member of our team to reach out to you.

This article was originally published on November 19, 2018 and more recently updated on June 16, 2022.