R&D Tax Credits: A Crash Course

Not sure if you qualify for the Research and Development (R&D) tax credit? If you devote resources to innovation initiatives but have never determined your eligibility, then you could be missing out on a vital source of tax savings.

You’ll find the rules for R&D tax credits outlined in Section 41 of the Internal Revenue Code, but we created this guide as a crash course to explain the main points so you can be familiar with it more quickly and without the accounting jargon.

The Basics of the R&D Tax Credit

The R&D Tax Credit was designed to be a tool that stimulates the economy, creates jobs and boosts international competitiveness, and it’s a primary means for rewarding research activities.

The federal government initially introduced R&D tax credits in 1981 as a two-year incentive to encourage research activities.

Fast forward to 2015: Congress passed the Protecting Americans from Tax Hikes (PATH) Act and made R&D tax credits a permanent feature of the Tax Code. The PATH Act also included additional taxpayer-friendly bonuses.

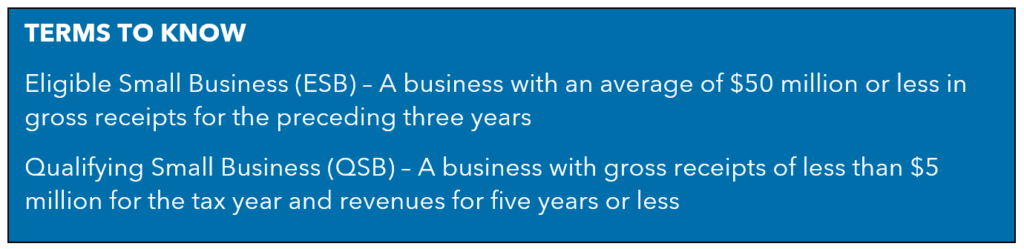

Effective in 2016, an Eligible Small Business (ESB) can offset its Alternative Minimum Tax with R&D credits. An ESB is a business with an average of $50 million or less in gross receipts for the preceding three years.

Additionally, a Qualifying Small Business (QSB) with no federal tax liability can use up to $250,000 of its R&D credits to offset payroll taxes until December 31, 2022. For tax years beginning after December 31, 2022, this threshold has moved to $500,000.

A QSB has gross receipts of less than $5 million for the tax year and has revenues for five years or less.

Qualifying for the R&D Tax Credit

R&D credits are available for specific forms of research known as Qualifying Research Activities.

Qualifying Research Activities are those that meet the four-part test set out by the IRS. Essentially, eligibility requires the activity to comply with all the following requirements:

- It aims to resolve or eliminate technical uncertainties when developing or improving a product or process.

- There is a process of experimentation to determine the best way forward, involving methods like modeling, simulation, trial and error and prototyping.

- Experimentation relies on hard sciences like physics, engineering, computer science or chemistry.

- It is undertaken for the purpose of developing or improving a product or process—to enhance its functionality, reliability, quality, performance or cost-efficiency.

Certain activities, such as research related to social-sciences and management functions, as well as activities conducted outside of the United States, are ineligible.

Costs that are eligible for the credit are known as Qualifying Research Expenses. You can claim three types of expenses, including salaries, supplies (such as materials and computer rentals) and contracted research, as long as you can support these claims with sufficient documentation.

Calculating Your R&D Tax Credit

In practice, Form 6765 (Credit for Increasing Research Activities) is used to calculate and claim the credits you are potentially entitled to. The completed form is filed by your R&D tax advisor with your business tax return.

You can use either the regular method or alternative simplified credit method to calculate your R&D credits—whichever gives a better result.

The regular method for the R&D tax credit is 20% of all qualifying expenditures for the current year that exceed a specified base amount. The alternative method is 14% of the difference between the number of qualifying expenditures for the current year and 50% of the average qualifying expenditures for the preceding three years.

Common Misconceptions about the R&D Tax Credit

Unfortunately, common misconceptions often prevent business owners from claiming R&D tax credits.

For example, many believe credits are reserved for revolutionary breakthroughs or new inventions. However, businesses are rewarded for attempting something technically challenging, and this can involve creating or improving a product or process. You don’t even have to succeed in your experiments to qualify.

Another misconception is that credits are available for specific industries, when all industries are, in fact, eligible. Any taxpayer may qualify, whether you are a start-up, sole proprietorship or large corporation.

Some also believe R&D tax credits are only relevant for profit-making enterprises, even though they can be carried forward for 20 years or can potentially be used against payroll tax liabilities.

Finally, there are those who dread the efforts involved in claiming the credit. While documentation requirements may seem onerous at first, many involve types of records that are already kept.

Moving Forward with R&D Tax Credits

It’s vital that businesses take full advantage of economic incentives such as those offered in Section 41 and in the R&D tax credit in order to be as competitive as possible.

And no business wants to overpay its taxes.

If identifying and claiming R&D credits seem overwhelming, Warren Averett’s experienced professionals can help you navigate the process both effectively and efficiently.

This article was originally published on July 22, 2019 and most recently updated on August 8, 2024.