Form 6765, Credit for Increasing Research Activities: A Beginner’s Guide

Research and Development (R&D) Tax Credits offer dollar-for-dollar reduction in federal income tax liability, but how easy is it to claim them?

The answer lies in Form 6765.

While the IRS provides instructions for using Form 6765, these often make references to the relevant sections of the Internal Revenue Code. So, unless you already know the technical ins and outs of the Tax Code, the IRS guidance can prove difficult and time-consuming to follow.

That’s why we developed a simple beginner’s guide for Form 6765—to help you figure out how to claim the R&D Tax Credit without the technical jargon.

What Is Form 6765, and Why Would I Need It?

Form 6765 is used to calculate and claim the R&D Tax Credits and to communicate how you would like to apply these credits.

For example, if you’re an eligible small business, you can use the tax credit to offset both your regular and alternative minimum tax. If you’re a qualified small business (you have gross receipts less than $5 million in the taxable credit year and you don’t have gross receipts for any year before the five-year period that ends with the taxable credit year), you can choose to apply the credit against payroll taxes. Or, if you’re a member of a group of companies, you can report and substantiate your portion of the group’s R&D Tax Credits.

What Information Is Required for Completing Form 6765?

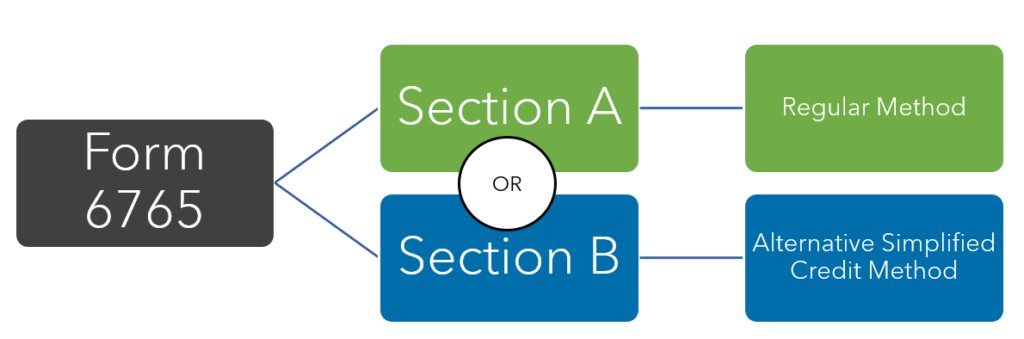

Form 6765 has seven distinct sections: Sections A, B, C, D, E, F and G.

Sections A, B, C and D historically have been part of Form 6765 for reporting numerical data associated with the R&D tax credit. Sections E, F and G have been newly added to the form after the IRS released a new version of the Form in early 2025. As a result, the additions of these sections will require taxpayers to provide additional, explanatory and more descriptive information with their tax returns.

We’ll take a deeper look at each of these seven sections, including the newly added Sections E, F and G, as well as what you’ll need to know to complete each of them.

Working Out Your Tax Credits – Sections A and B of Form 6765

A common area of confusion concerns the method to use when calculating your R&D Tax Credits. You can use either the Regular Method and fill out Section A, or the Alternative Simplified Credit Method and complete Section B.

(You won’t need to complete both Section A and Section B of Form 6765.)

One way to decide on the best approach is to figure out your entitlement under both methods, and then choose the one that is more advantageous.

In terms of how these approaches differ, the regular research credit is 20% of all qualifying expenditures for the current year that exceed a specified base amount.

Working out the base amount can be a potential pain point because it may involve detailed calculations—depending on whether you are a start-up or well-established business.

The Alternative Simplified Credit Method, on the other hand, begins with finding the difference between the amount of qualifying expenditure in the current year and 50% of the average qualifying expenditure for the preceding three tax years. This difference is then multiplied by 14% to arrive at your R&D Tax Credit.

Calculating your tax credits in Section A or B involves establishing whether expenses relate to eligible R&D activities. Qualifying activities are primarily those that meet the requirements of the four-part test set out by the IRS.

Form 6765 allows you to claim three types of expenses, including salaries, supplies (such as materials and computer rentals) and contracted research. However, bear in mind you will need to support these claims with sufficient documentation.

In practice, a starting point may be to identify potential qualifying research expenses (QREs) that make up the R&D cost in your financial accounting system. However, this is only a starting point, and more work will be needed.

Current Year Credit – Section C of Form 6765

Once you’ve quantified your R&D Tax Credit for the current year, Section C directs you to other forms and schedules, where you will need to report this figure given your business structure.

Claiming Payroll Tax Offset – Section D of Form 6765

Section D of Form 6765 allows a qualified small business to use some or all of your R&D Tax Credits to offset payroll tax obligations, up to a maximum of $500,000.

The amount you nominate in this section should then be replicated on Form 8974, Qualified Small Business Payroll Tax Credit for Increasing Research Activities. The payroll tax offset will become available quarterly after the filing of your federal income tax return.

(New) Other Information – Section E of Form 6765

This new section requires taxpayers to disclose several details that previously were mostly considered during an audit. This additional information includes the total number of business components generating QREs, as well as the total amount of officers’ wages included as QREs. In Section E, taxpayers must also report any major acquisitions or dispositions and any new categories of QREs that have not previously been claimed.

(New) Summary of Qualified Research Expenses – Section F of Form 6765

Taxpayers must itemize their QREs, including wages and contract research costs, in the new Section F.

(New) Business Component Information – Section G of Form 6765

Section G is optional for tax years starting before January 1, 2025, but it will be mandatory for many taxpayers in tax years beginning after December 31, 2024.

However, qualified small businesses that claim a reduced payroll tax credit are exempt from completing Section G. Taxpayers that have less than $1.5 million in QREs, have less than $50 million in gross receipts and that are claiming a research credit on an originally filed return, are also exempt from completing Section G.

For all other taxpayers, Section G requires information about the business components most responsible for QREs, the information sought for discovery, the qualified wages in specific categories and details about claims involving statistical sampling or those filed on amended returns.

Additional Things To Know About Form 6765

Form 6765 should be filed with your company’s income tax return no later than the extended due date of that year’s tax return.

R&D Tax Credits are a complex area to navigate. To ensure your business remains compliant while taking full advantage of tax savings opportunities, connect with a Warren Averett advisor who can help.

This blog was originally published on July 15, 2019 and was most recently updated on March 3, 2025.