The One Big Beautiful Bill Breakdown: Nonprofits

The One Big Beautiful Bill (OBBB) introduces several provisions that will significantly affect nonprofit organizations across the country.

It’s important to note that many controversial measures from earlier drafts (including revoking tax-exempt status without due process, taxing name and logo royalties, expanding unrelated business income tax on transportation benefits and increasing the excise tax on foundation investments) were removed before the Bill’s final passage.

So, while nonprofits have been spared from potentially severe operational and financial burdens, there are still several aspects of the legislation that will have an impact (both direct and indirect) on nonprofit organizations.

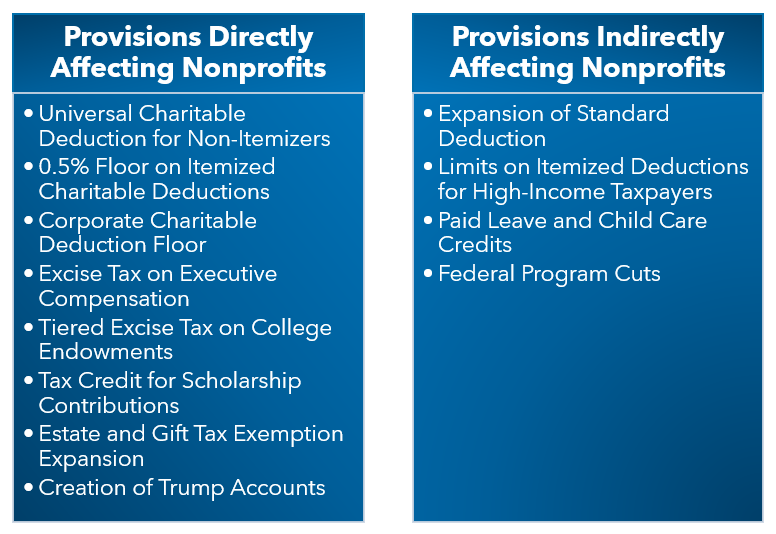

Provisions Directly Affecting Nonprofits

Universal Charitable Deduction for Non-Itemizers

Taxpayers who do not itemize can now claim a universal charitable deduction of up to $1,000 for individuals and $2,000 for married couples.

This provision is expected to generate an estimated $74 billion over 10 years for nonprofits. It’s also expected to expand the donor base by incentivizing charitable giving among middle-income households, potentially increasing small-dollar donations.

0.5% Floor on Itemized Charitable Deductions

Itemizing taxpayers must exceed a 0.5% threshold of their adjusted gross income (AGI) before charitable contributions become deductible. Because smaller donations will no longer offer tax benefits, high-income donors may reduce or restructure their charitable giving, which could lead to a decline in major gifts.

Corporate Charitable Deduction Floor

Corporations can only deduct charitable contributions that exceed 1% of taxable income, with limited, five-year carryforward for excess contributions. Small and mid-sized businesses may scale back their charitable efforts in response, which will impact nonprofits that rely on corporate giving.

Excise Tax on Executive Compensation

The 21% excise tax on nonprofit executive compensation of over $1 million now applies to all current and former employees, not just the top five. This takes effect for tax years starting after December 31, 2025. Large nonprofits, especially those in the healthcare and education fields, may face increased tax liabilities and pressure to restructure compensation packages.

Tiered Excise Tax on College Endowments

Nonprofit colleges and universities with over 3,000 tuition-paying students face a tiered excise tax on investment income:

- $500,000-$750,000 per student: 1.4%

- $750,001-$2 million: 4%

- Over $2 million: 8%

As a result, reduced endowment income may limit grant-making and financial support for affiliated nonprofits and scholarship programs.

Tax Credit for Scholarship Contributions

Donors can receive a non-refundable tax credit of up to $1,700 for contributions to qualified Scholarship Granting Organizations (SGOs). Unused credits can be carried forward for five years.

Educational nonprofits may see increased donations, but nonprofits in other sectors may see reduced funding as donors shift their giving to maximize tax credits.

Estate and Gift Tax Exemption Expansion

The estate and lifetime gift tax exemption is permanently extended to $15 million for individuals, indexed for inflation. Fewer estates will be subject to tax, potentially reducing charitable bequests made for tax planning purposes.

Creation of Trump Accounts

The OBBB introduces “Trump Accounts,” tax-free savings vehicles for children under 18, that can be used for education, housing or business ventures once the beneficiary turns 18. Nonprofits can contribute to these accounts for qualified groups. These accounts could make it harder for nonprofits, especially those focused on education and youth programs, to raise funds the traditional way.

Provisions Indirectly Affecting Nonprofits

Expansion of Standard Deduction

The standard deduction, which was set to be reduced significantly prior to the OBBB, has been permanently increased to $15,750 for single filers and $30,000 for joint filers (and will be indexed for inflation). This reduces the number of taxpayers who itemize. With fewer taxpayers itemizing, fewer donors will get a tax benefit for giving, which could lead to a drop in overall donations.

Limits on Itemized Deductions for High-Income Taxpayers

Deduction caps have been placed for those in the highest tax bracket (37%). The cap reduces the overall itemized deductions by 2/37, making the effective benefit of itemized deductions for high income taxpayers 35% instead of 37%. High-net-worth donors may reduce or restructure their giving, impacting capital campaigns and major gift programs.

Paid Leave and Child Care Credits

Credits for paid family leave and employer-provided childcare have been expanded. However, nonprofits are excluded from claiming these credits, potentially creating inequities in employee benefits compared to for-profit employers.

Federal Program Cuts

The OBBB reallocates funding across federal agencies, which may indirectly affect nonprofits that rely on federal funding. These reallocations have resulted in reductions in Medicaid, SNAP and other federal programs.

Nonprofits may face increased competition or reduced availability of federal support. Those serving vulnerable populations could see an increased demand for services that stretches already tight resources.

What It Means for You

The OBBB is a mixed bag for nonprofits.

While the universal charitable deduction and scholarship tax credits are bringing new opportunities, the limitations on itemized and corporate deductions, expanded excise taxes and estate tax changes may reduce high-dollar contributions and strain nonprofit budgets.

Indirect provisions, such as changes to the standard deduction and federal funding priorities, make things even more complicated.

Nonprofits need to stay informed, rethink fundraising strategies and advocate for policies that affect their work to ensure they can effectively advance their missions under the new law.

To learn more about how the One Big Beautiful Bill and these provisions may impact you, contact your Warren Averett advisor.