The One Big Beautiful Bill Act Breakdown: Trump Accounts

As the dust settles after a record-long government shutdown, the IRS continues to release guidance on how taxpayers should handle the new tax rules under the One Big Beautiful Bill Act of 2025.

Guidance published on December 2, 2025, in the form of Notice 2025-68 provides much-needed clarity regarding a new investment vehicle named after the President: Trump Accounts.

What Are Trump Accounts?

The One Big Beautiful Bill Act permits the establishment of a Trump Account on behalf of every qualifying American child for whom an election is made. The goal of these federally backed savings accounts is to encourage long-term saving and investment from infancy through adulthood.

There are no income restrictions for establishing a Trump Account. To qualify, all you need is a valid Social Security number for the newborn. The Secretary of the Treasury will create or organize the account; however, funds can be transferred to a brokerage firm at a later date.

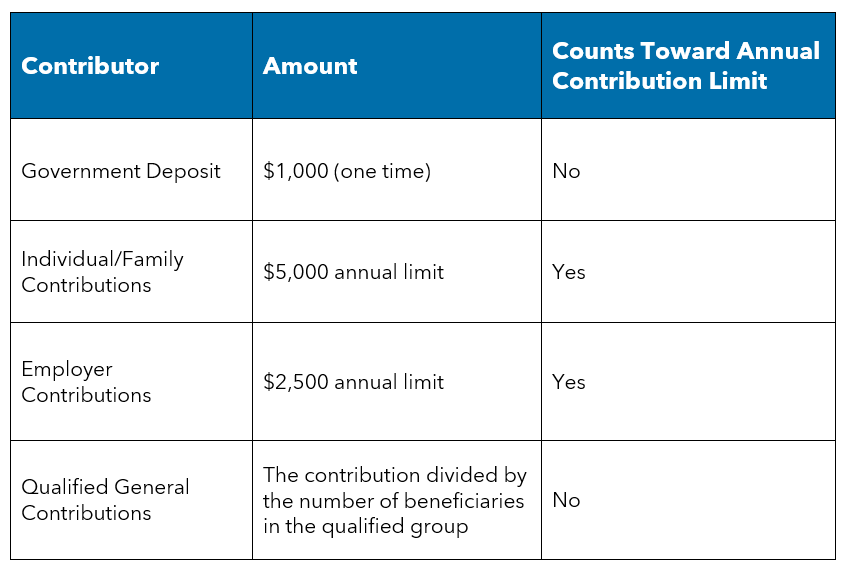

Each qualifying child born between January 1, 2025, and December 31, 2028, will receive a one-time $1,000 government-backed pilot contribution.

Making the Election To Establish a Trump Account

The election can be made through Form 4547, filed at the same time as the 2025 income tax return. Applicants will also be allowed to use an online application (trumpaccounts.org), which is expected to go live in July 2026.

Contributions to a Trump Account

Contributions in this initial phase cannot start until July 4, 2026. However, once contributions are allowed, the following guidelines (based on the bill) will apply.

Parents, guardians and other individuals can contribute up to $5,000 per year until the child turns 18. Parental and family contributions are not tax-deductible and are not taxable upon withdrawal.

Employers may contribute up to $2,500 annually, which is not taxable at the employee or employer level. The employer’s contribution counts against the $5,000 yearly limit and is taxable upon withdrawal.

In addition, the law allows for “qualified general contributions,” which are funds provided by states, the U.S. government, Indian tribal governments, or 501(c)(3) organizations for members of a qualified class of account beneficiaries.

Trump Accounts have an annual contribution limit of $5,000 combined from all sources. However, the one-time $1,000 government deposit and qualified general contributions do not count against the $5,000 limit.

Contributions must be made by December 31 of the contribution year (once they are allowed). Deposits must be invested in stock mutual funds or exchange-traded funds mirroring the S&P 500 or another American stock index during the growth phase. The growth phase spans from the child’s birth through their 18th birthday.

Distributions From a Trump Account

During the growth period, distributions are generally not allowed, except for qualified rollovers, excess contributions or upon the death of the account beneficiary. Once the child turns 18, the account becomes a traditional IRA and will follow standard IRS deadlines for contributions.

Any distribution may be subject to the 10% additional tax on early withdrawals unless an exemption applies (e.g., qualified education expenses, first-time home purchase or the beneficiary reaching age 59½).

What About Children Born Before 2025?

Children born before January 1, 2025, are eligible for a Trump Account with all its features, except they will not receive the $1,000 government-backed deposit.

However, as the news broke about Notice 2025-68, it was revealed that Dell Technologies CEO Michael Dell and his wife Susan pledged $6.25 billion toward Trump Accounts. The pledge aims to expand access for eligible children who are too old to qualify for the $1,000 seed deposit.

With these additional funds, an estimated 25 million American children under age 10 could receive a $250 grant in a Trump Account. To qualify for the $250 Dell contribution, children must live in a ZIP code where the median household income is $150,000 or less.

It is not yet known how the Dell pledge will interact with the guidance published by the Treasury Department and the IRS. Questions remain about claiming and eligibility details.

What It Means for You

This new law aims to spark wealth-building for children while promoting economic stability. However, it is still important to evaluate whether Trump Accounts, a 529 plan, Roth IRA or another investment vehicle is the best fit for your child and family.

To learn more about how the One Big Beautiful Bill Act and this specific provision may impact you, contact your Warren Averett advisor.

This article was originally published on October 2, 2025, and most recently updated on December 12, 2025.