Could One Law Drastically Impact Your Company’s Current or Future Retirement Plan? [8+ Things to Know About the SECURE Act]

Can one law drastically impact your company’s retirement plan? Yes. And it did.

The Setting Every Community Up for Retirement Enhancement (SECURE) Act (signed into law on December 20, 2019) is considered to be the most impactful retirement legislation in almost 20 years; it contains several provisions to advance the access to and facilitate ease of the administration of qualified retirement plans.

Businesses everywhere will need to amend their retirement plans to reflect the changes in the SECURE Act.

Many of the provisions in the SECURE Act went into effect January 1, 2020, but other provisions will go into effect in the coming years. The deadline for amending is the end of the first plan year beginning on or after January 1, 2022, which should be plenty of time, but it’s important for companies to gain an understanding of what the SECURE Act means for their plans now.

Below, I’ve provided an explanation of the changes related to retirement plans, their effective date and what these changes mean for employers.

1. The SECURE Act introduced small business start-up credits.

Effective as of December 31, 2019, small business with up to 100 employees can now receive a credit for beginning a retirement plan for its employees. This credit is available for the first three years of a plan’s existence.

The SECURE Act increases the current $500 tax credit to the greater of:

- $500 or

- the lesser of

- $250 per non-highly compensated employee who is eligible to participate or

- $5,000

In addition, plans that have an automatic enrollment provision receive an additional $500 credit for three years, regardless of when the automatic enrollment provisions are adopted.

What impact will this have on businesses?

With this new provision in place, there really hasn’t been a better time for small employers to set up some type of retirement plan for their employees.

Small employers that begin a new retirement plan, or those that started one less than three years ago, can take advantage of this credit to help defray most—if not all—of the cost associated with operating a retirement plan.

2. The SECURE Act introduced new plan adoption deadlines.

My accounting friends are going to love this one.

Effective beginning after December 31, 2019, the SECURE Act permits the adoption of new plans after the end of a tax year, but before the tax filing due date for that year (including extensions). For a tax year end of December 31, 2020, the due date to adopt a plan is the tax filing due date in 2021.

What impact will this have on businesses?

Extending the deadline gives employers added flexibility in starting a retirement plan.

It seems like every year, March rolls around, and we get a call from a small business owner or CPA asking if they could start a retirement plan for the prior tax year.

Previously, the answer has, unfortunately, been: no.

But for plan years 2020 and beyond, that answer is now: Of course, you can start a plan.

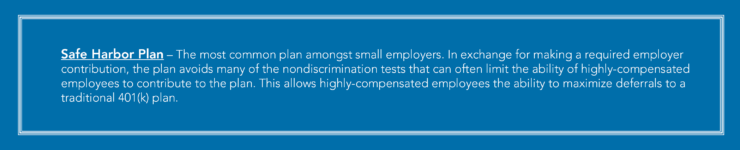

3. The SECURE Act gives new rules for non-elective Safe Harbor plans.

The SECURE Act presented several new rules concerning non-elective Safe Harbor plans. Here are the highlights:

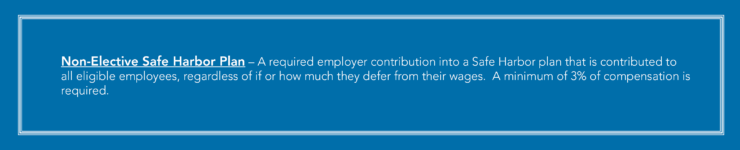

- Eliminating the Notice Requirement for Non-Elective Safe Harbor Plans – Prior to December 31, 2019, all Safe Harbor plans were required to provide a Safe Harbor notice to participants no later than 30 days prior to the plan year end.

Effective for plan years beginning after December 31, 2019, non-elective Safe Harbor plans that don’t offer any matching contributions are no longer required to provide the annual notice.

- Adoption of Safe Harbor Plans after Plan Year Begins – Prior to December 31, 2019, a 401(k) plan couldn’t be amended to a Safe Harbor during the current plan year.

Now, for plan years beginning after December 31, 2019, Safe Harbor non-elective provisions may be adopted up to 30 days prior to plan year end. A Safe Harbor contribution equal to 3% would be required.

401(k) plans may adopt Safe Harbor non-elective provisions in the specific time frame that is:

- 29 days before the plan’s year end, and

- before the due date of any required corrective refunds if they make a 4% Safe Harbor

(Typically, these refunds are due prior to the last day of the following plan year).

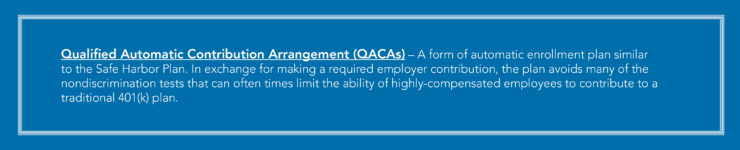

- Increased Cap for Automatic Enrollment – Prior to the new regulations, Safe Harbor 401(k) plans that provided for automatic enrollment under a Qualified Automatic Contribution Arrangement (QACA) limited the default contribution rate.

Effective for Plan years beginning after December 3, 2019, the SECURE Act increases this cap from 10% to 15% for any year after the first year.

What impact will this have on businesses?

The Safe Harbor 401(k) plan allows for employers to avoid some nondiscrimination testing. The elimination of the notice requirement removes the administrative burden to deliver the notice to all participants.

In addition, when a traditional 401(k) plan fails the nondiscrimination test, refunds are typically made to select employees. The ability to retroactively avoid these tests gives plan sponsors an additional alternative that allows employees to keep all of their elected deferrals in the plan.

4. The SECURE Act provides new plan distribution rules.

New plan distribution rules from the SECURE Act include:

- Prior to the new regulations, the required beginning date for Required Minimum Distributions was April 1 of the calendar year following the year in which a participant turns age 70.5 or terminated employment, whichever comes later.

The SECURE Act increases the age from 70.5 to 72. This is effective for employees who turn 70.5 after December 31, 2019.

- Effective December 31, 2019, plan loans effected through credit cards will be considered a taxable distribution. Previously, plans were allowed to issue loan proceeds via credit cards.

- Effective after December 31, 2019, plan participants who have or adopt a child after the effective date can now take a distribution of up to $5,000 from a plan or IRA without a penalty. Prior to effective date, a 10% premature distribution penalty would have applied.

- Prior to the SECURE Act, participants in a pension plan were required to be age 62 to receive a distribution while still employed. Effective after December 31, 2019, the SECURE Act lowers the age from 62 to 59.5.

What impact will this have on businesses?

The real impact concerns plan participants. The ability to leave money in the plan longer allows retirees more flexibility and, potentially, a more comfortable retirement.

The ability of younger employees to withdraw these funds should give them comfort in knowing that they can contribute towards retirement and still have the flexibility to withdraw as life changes occur.

5. The SECURE Act requires the inclusion of long-term, part time employees.

In an effort to increase access to retirement plan coverage, the SECURE Act requires plans to allow employees who are 21 years of age or older, have worked at least three consecutive years and have completed at least 500 hours of service in those years to have the ability to make 401(k) deferrals (effective for plan years beginning after December 31, 2020).

Previously, an employer could exclude employees who work less than 1,000 hours in a 12-month period. These employees aren’t required to receive an employer contribution and are excluded from non-discrimination testing.

Years of service prior to January 1, 2021 will not need to be considered for the three-year period purposes. The earliest these employees would need to be considered is 2024.

What impact will this have on businesses?

This is a positive for both the plan sponsor and participants. It allows participants to participate who might not otherwise have access to a retirement account. The plan sponsor doesn’t necessarily have to cover these employees with employer contributions, and they are excluded from most nondiscrimination tests.

Plan sponsors that currently exclude this class of employees should begin the process of determining just how this affects their specific plan now.

6. The SECURE Act includes changes to lifetime income investments (annuities) in defined contribution plans.

Changes include the following:

- Safe Harbor fiduciary standards for selection of Lifetime Income (Annuity) Provider – Effective after December 31, 2019, defined contribution fiduciaries can rely on new Safe Harbor standards for the selection of annuity providers to make available as an investment option or a component of an investment option under a Plan.

If these standards are adhered to, the fiduciary liability is limited for problems that arise after the investment is purchased.

- Portability of Lifetime Income Investments – Effective for plan years beginning after December 31, 2019, lifetime income investments are subject to significant penalties and charges upon liquidation.

The SECURE Act allows for additional portability of these investments in cases where the plan sponsor eliminates the plan level investment. Without regard to any plan level or in-service distributions, the distribution of the investment can be made via a direct transfer to another retirement plan.

- Lifetime Income Disclosure – At least annually, benefit statements are required to include an estimate of the monthly income a participant could expect to receive if an annuity were purchased with his or her account balance.

It’s important to note that the plan sponsor and other fiduciaries are liable to participants solely by providing this information. This is effective one year after the DOL issues interim final rules.

What impact will this have on businesses?

It’s up in the air still as to how many plan sponsors will elect to allow annuities as an investment.

The complexity and expense associated with annuities makes it probable that they may be misused. The lifetime income disclosure will more than likely be confusing to most participants.

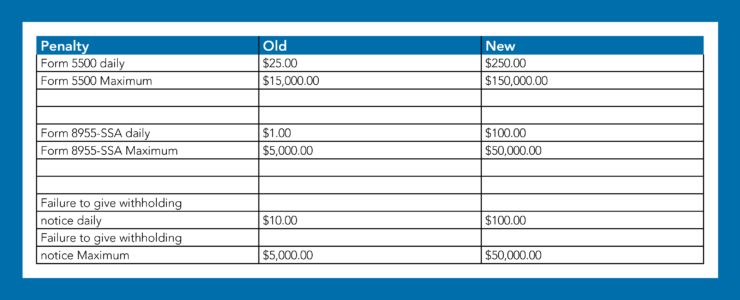

7. The penalty for late filings has gone up significantly under the SECURE Act.

Effective December 31, 2019, the penalty for late Form 5500s increased from a $25 per-day penalty to a $250 per-day penalty. The maximum penalty amount increased from $15,000 to $150,000.

The penalty for late Form 8955-SSAs increased from a $1 per-day penalty to a $100 per-day penalty. The maximum penalty amount increased from $5,000 to $50,000.

The penalty for failing to give participants notice regarding their right to not have withholding apply to distributions is increased from a $10 per-failure penalty to a $100 per-failure penalty. The maximum penalty amount increased from $5,000 to $50,000.

What impact will this have on businesses?

Plan sponsors should ensure the providers of their retirement plan are keeping the entire plan in compliance.

While the Form 5500 penalties are substantial, there are many other plan failures that can cost significantly more. It’s important to note that the Delinquent Filer program is still in existence and greatly limits the potential penalty.

8. The SECURE Act allows for multiple-employer retirement plans.

The SECURE Act allows for multiple employers with no common nexus to band together and form one retirement plan. Effective for plan years beginning in 2021, the SECURE Act allows for a group to file a single annual report instead of multiple reports for each plan.

What impact will this have on businesses?

This is probably the biggest item to come out of the SECURE Act. There are many complexities and unanswered questions with this one. Look for additional information as we learn more about the details.

Additional Changes Under the SECURE Act Worthy of Noting

But wait. There’s more. Here are a few other notable things to know about the SECURE Act.

- The SECURE Act modified Required Minimum Distribution Rules upon the death of a participant, effective for participants who die after December 31, 2019.

Distributions from defined contribution and IRA accounts are required to be distributed within 10 years of the participant’s death unless the distribution is to an Eligible Designated Beneficiary. Prior to the SECURE Act. the distribution could be extended over the designated beneficiary’s life.

- Individuals over age 70.5 will no longer be prohibited from contributing to traditional IRAs.

- If a defined benefit plan is frozen and is closed to certain classes of employees, the SECURE Act provides relief from nondiscrimination, coverage and participation if certain requirements are met. This is effective on the date of enactment that the plan sponsor selects.

Evaluating the Impact of the SECURE Act on Your Business’s Retirement Plan

What do these changes mean for your company’s retirement plan? Have you been contemplating offering a retirement plan but are unsure of where to start in light of these changes?