What is a Cost Segregation Study? (How It Works and Why It Matters)

A cost segregation study can be a powerful way to maximize depreciation deductions and minimize the tax burden for commercial property owners who acquire or develop real estate.

Yet real estate owners, investors and their tax advisors often overlook cost segregation studies simply because they’re not familiar with how it works or what the result is. (Spoiler alert: It may save your company a lot of money.)

Below, we’ve answered a few frequently asked questions about cost segregation studies, how they work, and the tax benefits they provide.

What Is a Cost Segregation Study?

For income tax purposes, property owners and real estate investors generally depreciate residential rental property over 27.5 years and commercial property over 39 years.

But a residence, office building, warehouse or any other real property is never just the structure alone. It also includes several other elements, such as plumbing fixtures, carpeting, sidewalks, fencing and a lot more.

If you were to purchase these assets by themselves, you could depreciate them over five, seven or 15 years. But they are usually purchased as part of a building acquisition or development and written off over the same useful life as the rest of the building: 27.5 or 39 years.

A cost segregation study is a process that looks at each element of a property, splits them into different categories, and allows you to benefit from an accelerated depreciation timeline for some of those building components.

Why Does a Cost Segregation Study Matter for Property Owners?

Segregating the costs of a property matters because of the financial benefits it provides. While the study has an up-front cost, the tax savings from accelerating depreciation deductions can result in significantly increased cash flow over several years.

With a cost segregation study, you get the benefits of time value of money. However, that also means that if you don’t plan on holding the property for the long term, you may not get any benefit from having a cost segregation study because any up-front benefits reverse upon the sale of the property.

Who Performs Cost Segregation Studies?

Performing this analysis on your own isn’t really feasible. It typically involves a team of tax advisors and engineers working together to decide which components of a building should go into each category and how much each element costs on its own.

How Does Cost Segregation Work?

The goal of a cost segregation study is to identify all property-related costs that can be depreciated over five, seven and 15 years—or written off faster using bonus depreciation, which is 60% in 2024 and 40% in 2025.

To accomplish this, your advisory team reviews available property records, inspections, cost details and blueprints and may also perform a physical inspection of the property.

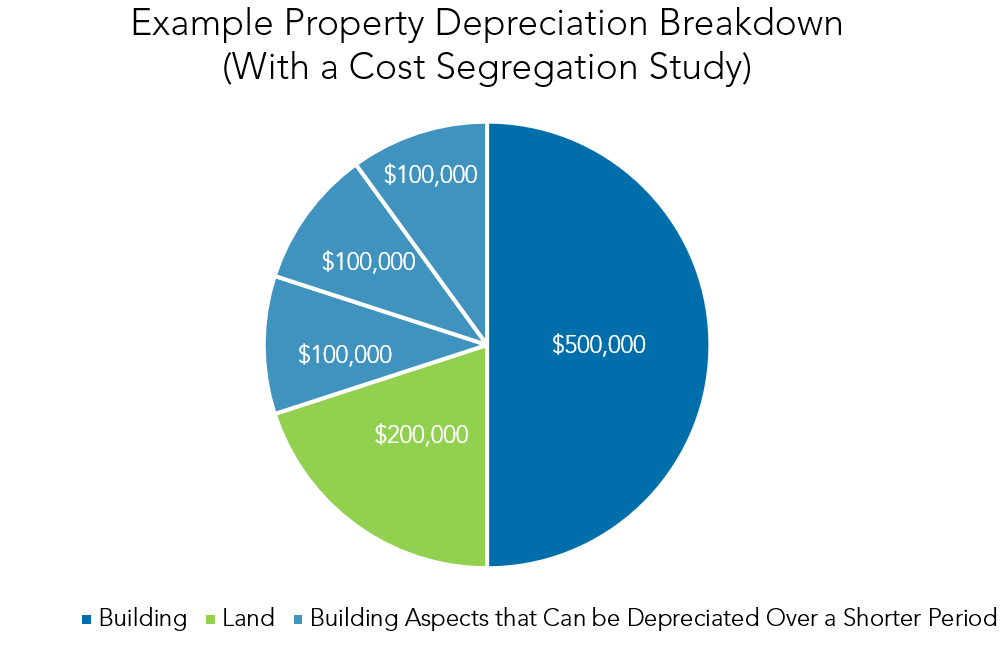

Cost Segregation Study Example

For example: you buy an office building for $1,000,000. Land isn’t depreciable, so you decide the land is worth $200,000, and the building is worth $800,000.

If you depreciate the building over 39 years, your depreciation write-off would be $20,512.82 per year. Assuming a 37% federal income tax rate, that would save you roughly $7,500 in taxes.

Now, let’s say you decide to get a cost segregation study. After completing the study, your advisory team identifies the following costs:

- $100,000 of interior fixtures and finishes that can be depreciated over five years

- $100,000 of interior fixtures that can be depreciated over seven years

- $100,000 of land improvements that can be depreciated over 15 years

Based on the study, $300,000 of the $800,000 building is eligible for bonus depreciation, so 60% of the cost could be written off in 2024. Assuming a 37% tax rate, that would result in tax savings of $72,634 over depreciating the building with no cost segregation (($216,821 – $20,512.82) x 37%).

However, even if you didn’t take advantage of bonus depreciation, those items could be depreciated over a shorter recovery period using an accelerated depreciation method. As a result, your estimated first-year depreciation write-off would be:

- Building ($500,000 / 39 years): $12,820.51

- 5-year property ($100,000 / 5 years): $20,000

- 7-year property ($100,000 / 7 years): $14,285.71

- 15-year property ($100,000 / 15 years): $5,000

Total first-year depreciation expense: $52,106.23

So even if you didn’t take advantage of bonus depreciation, your first-year depreciation write-off would result in a tax savings of $11,689.56 over depreciating the building over 39 years with no cost segregation (($52,106.23 – $20,512.82) x 37%).

When Is the Best Time to Get a Cost Segregation Study?

The best time to conduct a cost segregation study is in the year the building is acquired, constructed or remodeled. However, you can have a look-back study done any time afterwards and claim the resulting write-offs without amending prior-year tax returns.

Learn More about Cost Segregation Services

Every commercial property is unique. If you’re interested in finding out whether a cost segregation study is right for your property, the first step is connecting with an advisor about your options.

This article was originally published on September 1, 2021 and most recently updated on October 18, 2024.