Casualty Losses: What You Need to Know to Help Your Business Recover from a Natural Disaster

Natural disasters and the resulting recovery can be burdensome and even devastating for some businesses.

After a disaster, it can be hard to know how to get your business, its operations and its finances back on track, but there are many options available to help impacted companies.

Depending on a business’s specific situation, casualty losses may be able to help companies start on the road to recovery.

What is a Casualty Loss?

A casualty loss is defined as the damage, destruction or loss of property resulting from an unexpected event, such as a flood, hurricane, tornado or other natural disaster.

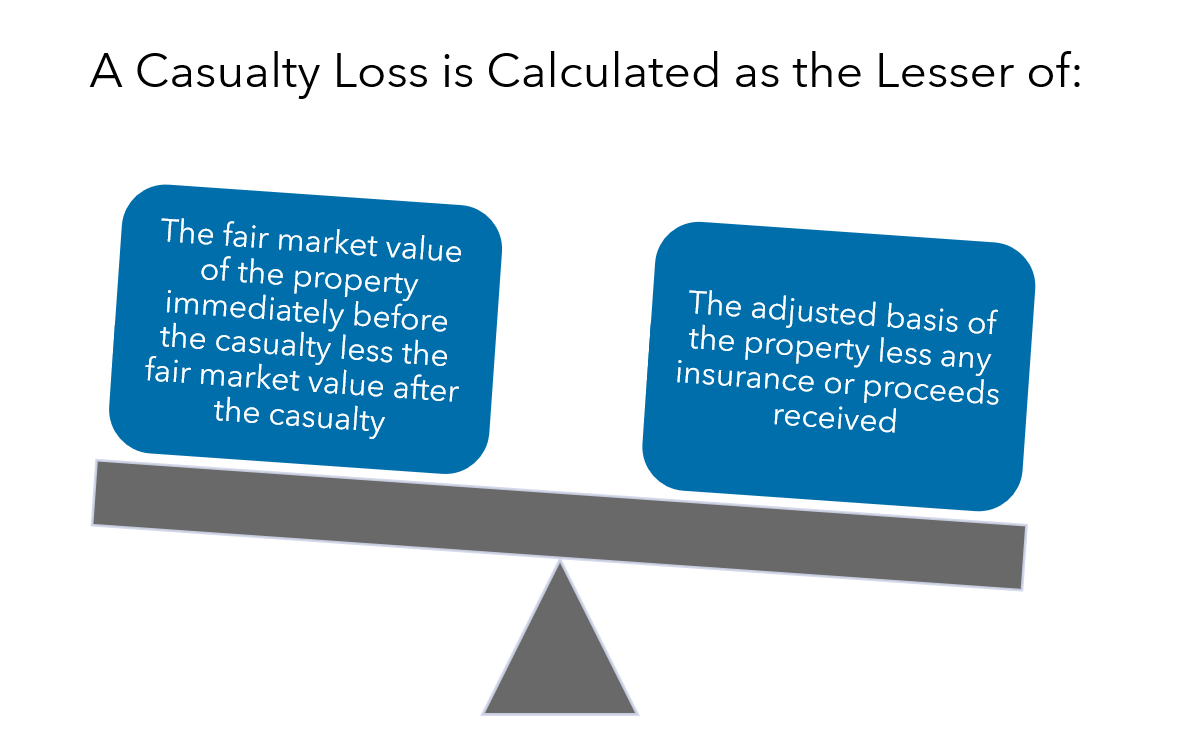

A casualty loss is calculated as the lesser of:

- The fair market value of the property immediately before the casualty less the fair market value after the casualty; or

- The adjusted basis of the property is less any insurance or proceeds received.

There are multiple safe harbor methods that can be used to calculate the drop in fair market value on personal property losses, including your principal residence, second home or contents.

Who Can Take a Casualty Loss?

The Tax Code allows for the deduction of a loss if it is connected to a trade, business or a transaction entered into for profit.

If a loss is not related to business, it can be deducted as a personal casualty loss, but additional limitations apply. In order to take a personal casualty loss from 2018 until 2025, the loss must have occurred in a presidentially declared disaster area.

Other limitations associated with a personal casualty loss include a $100 limitation per casualty and an overall limitation of 10% of the taxpayer’s adjusted gross income unless it is designated as “qualified disaster” by Congress.

If it is designated as a “qualified disaster,” then the limitation goes up to $500 per casualty, but there is no limitation for adjusted gross income.

You may also add the casualty loss to your standard deduction if you do not itemize. Congress has in the past designated major disaster areas based on FEMA individual and public assistance as “qualified disasters” in year-end tax bills.

Can Trees and Timber be Included in a Casualty Loss Claim?

The IRS recognizes landscaping and trees as a part of your property, even if you purchased and planted them at a different time than when you purchased your property.

So, to mitigate the loss of trees on your property after damage from a hurricane or natural disaster, you may be entitled to a casualty loss deduction on your federal tax return.

The National Woodland Owners Association (NWOA) has released an article about casualty losses related to timber and landscape trees that could be helpful to you. The NWOA examines how to determine your property’s original basis, discusses how and when to claim a casualty loss and provides examples of casualty loss scenarios.

Another valuable resource may be the National Timber Tax Website, which provides an overview of what property owners should consider when looking to take advantage of a casualty loss for trees or timber, including:

- Unmerchantable timber;

- Salvaged damaged timber; and

- Involuntary conversions.

For victims with timber losses, you will need to get an appraisal of the fair market value of the timber before the storm and the fair market value of timber after the storm from a certified appraiser.

What Should I Prepare or Know Now?

Here are a few tips that may help if you’re looking to make a casualty loss claim:

Prioritize Documentation

Take pictures of everything that is a loss, especially high-end valuables, and keep and track receipts of items bought during recovery efforts.

Know Your Insurance Coverage

Be aware of deductibles. Does your policy reimburse hotel or rental home expenses if you are displaced? Does your policy provide replacement cost coverage or actual cash value?

Be aware that some insurance reimbursements and government agency funds are not required to be recognized as taxable income. Insurance payments received to cover living costs when displaced are excluded from income. Payments received from a government agency for the cost of moving are also not included in income.

Know the Disaster Area Specifications

Know that if you have a business or home in a FEMA-declared disaster area, you may have a tax-deductible casualty loss. If you are outside of these counties, your deductible personal casualty loss is limited to the extent of personal casualty gains.

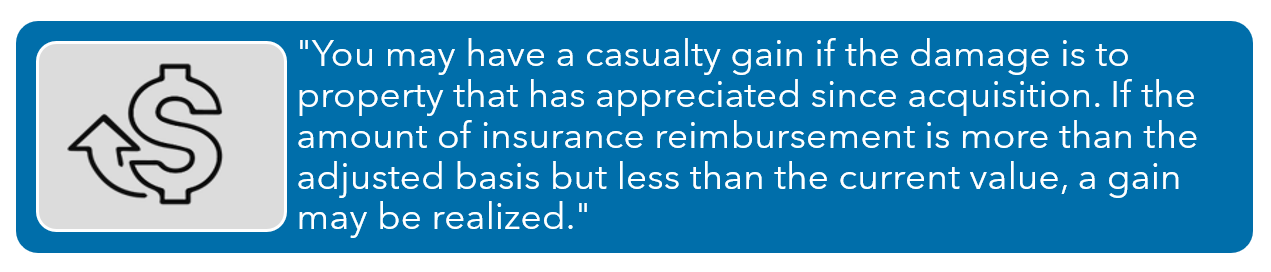

Understand Casualty Gains

Know that you may have a casualty gain if the damage is to property that has appreciated since acquisition. If the amount of insurance reimbursement is more than the adjusted basis but less than the current value, a gain may be realized.

You can elect to defer the gain recognition on your tax return by purchasing replacement property within a period that begins when the casualty occurred and ends two years after the close of the first tax year in which any part of the gain is realized.

Understand Safe Harbor Methods

Be aware that using a safe harbor method to compute the casualty loss will not be challenged by the IRS, eliminating the potential need for costly litigation.

Connect with Your Tax Advisor

Talk to your tax advisor as soon as you can about what information is needed to calculate the loss and if it would be beneficial to recognize the loss on your tax return.

How Can I Learn More About Casualty Losses for My Business?

We know that not every situation is covered in the information above, and each property owner’s specific circumstance will be different.

The IRS has answered common questions from disaster victims specifically about casualty losses. You can access an excerpt from the IRS website here to learn more about how to determine and compute casualty losses.

The most effective way to obtain reliable insight and advice for your business during hurricane or disaster recovery is to partner with an advisor.

If you have questions about casualty losses, tax relief associated with disaster recovery or helping your business after a hurricane, please contact us to have a tax and disaster recovery financial expert reach out to you.

This article was originally published in October 2018 and was most recently updated with new information and insight on August 31, 2022.