Long-Term Part-Time Employees: SECURE 2.0 Act Considerations for Companies

The Setting Every Community Up for Retirement Enhancement Act of 2019 (the SECURE Act) and its successor, the SECURE 2.0 Act of 2022 (the SECURE 2.0 Act) have ushered in a new era for the retirement plans that companies offer to their employees.

Historically, companies could exclude individuals who worked fewer than 1,000 hours in the plan year from being eligible for a retirement plan.

In 2020, the SECURE Act required employers that offer 401(k) plans to consider long-term part-time employees for eligibility, vesting and company contribution purposes. Under the SECURE Act, companies were required to make these team members eligible for a retirement plan no later than 2021.

The SECURE 2.0 Act modified these rules in 2022, requiring that long-term part-time employees be allowed to participate in a company’s plan after working at least 500 hours for two consecutive years. This change is effective starting with the 2025 plan year. It also makes the long-term part-time employee rule apply to 403(b) plans subject to ERISA.

Here’s what your company should know about complying with the long-term part-time employee requirements in your sponsored retirement plan.

Who qualifies as a long-term part-time employee?

A long-term part-time employee is any employee who worked at least 500 but fewer than 999 hours in three consecutive years. For the SECURE Act and the SECURE 2.0 Act, only those years after 2020 are counted. For plan years after 2024, only two consecutive years are required.

What are the specific compliance requirements for long-term part-time employees?

Plans with a 1,000-hour eligibility rule and those that exclude part-time employees will need to amend their plans, begin tracking the actual hours for all employees and comply with the vesting provisions of the new legislation. If employer contributions are made, they must vest based on 500 hours as opposed to 1,000 hours in a plan year that is typically used.

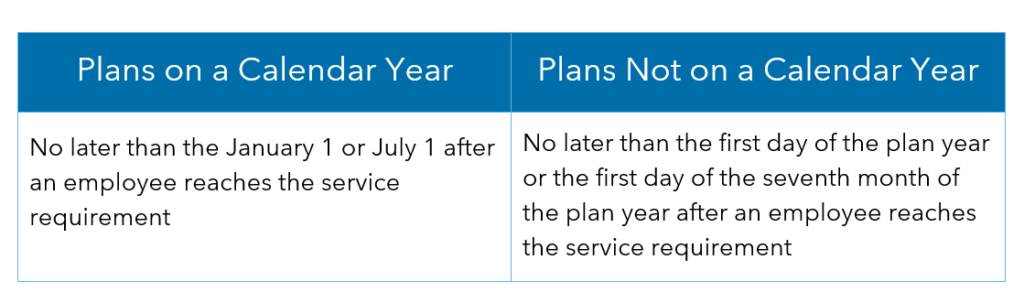

Once employees meet the service requirement, they must be permitted to participate in the plan no later than the following January 1 or July 1—or, for plans not on a calendar year, the first day of the plan year or the first day of the seventh month of the plan year.

Employer contributions aren’t required for these long-term part-time employees. However, if an employee ever becomes eligible for employer contributions, those long-term part-time employees will continue to vest at 500 hours.

Are minimum age requirements still allowed?

Yes, plans can still allow participants to meet minimum age requirements. For example, many programs require employees to be at least 21 to participate in a plan or to be at least 18 for vesting.

Are classes of employees still excludable?

Yes, so long as those classes are clearly defined and do not include a significant portion of part-time employees.

How do these changes affect retirement benefits?

These modifications could substantially change the landscape of retirement benefits.

Including long-term part-time employees in retirement plans means more employees might become eligible for company matches or profit-sharing contributions. Additionally, the earlier eligibility brought about by the SECURE 2.0 Act can lead to an uptick in participants and contributions.

How should plans be amended under the SECURE 2.0 Act?

A plan amendment signed in 2023 to be effective in 2024 is ideal. However, if employers haven’t formally amended their plans when the new rules go into effect in 2024, they will need to track how they apply these new rules in operation. An amendment will be required by 2026.

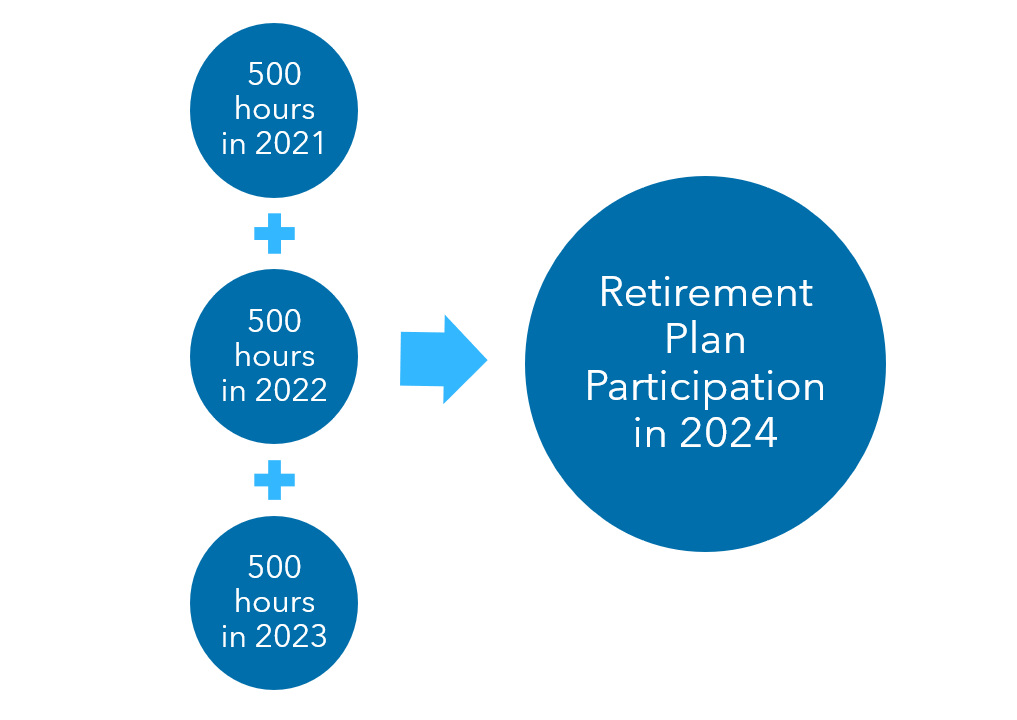

For example, employers must count hours for 2021, 2022 and 2023 to see if any part-time employees have worked at least 500 hours in each of those three years and must be offered retirement plan participation in 2024.

Companies that fail to comply may face substantial penalties, so it’s essential to have systems in place to avoid noncompliance and mitigate potential risks. Some companies might even contemplate a complete retirement plan redesign to ensure plan structures align with the new regulations.

What is the deadline for plan sponsors to amend their retirement plans?

Timeliness is of the essence. With many provisions going into effect for the 2024 plan year, employers should act promptly. Working with a trusted advisor to amend your retirement plan documents can prevent last-minute scrambles and potential oversights. Amendments aren’t required until 2026.

What are the potential impacts on retirement plan administration costs?

The modified criteria for long-term part-time employees can inevitably raise administrative costs because of the need for more rigorous hour tracking, meticulous record-keeping or adjustments to the benefit distribution structures.

Balancing retirement benefits with cost management will require strategic planning. Employers might consider leveraging technology or outsourcing specific tasks to ensure cost-effectiveness while retaining employee satisfaction.

Learn More About Amending Your Plan and Complying With the SECURE 2.0 Act

The SECURE 2.0 Act heralds a new chapter for long-term part-time employees and the companies that employ them. In this evolving landscape, being informed and proactive is key.

We are expecting additional guidance from the IRS soon. Please stay tuned.

Reach out to a Warren Averett advisor for assistance navigating the new rules and ensuring your company is better positioned for the future.

This article was originally published on October 26, 2023 and most recently updated on January 17, 2024.