A Business’s Guide to R&D Expense Capitalization and Amortization Changes

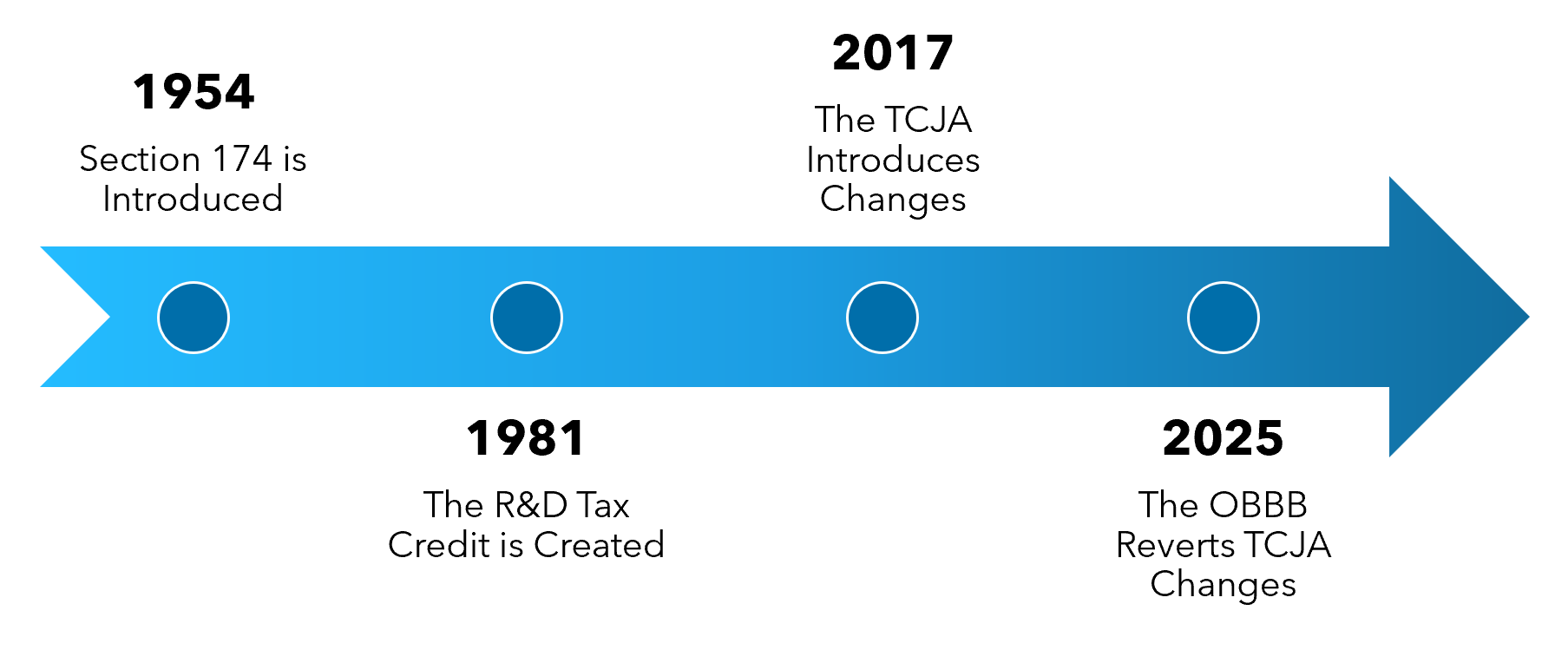

Since 1954, Section 174 of the federal tax code has allowed businesses to deduct qualified research expenses in the year they incurred those costs. Congress also created the R&D Tax Credit in 1981. Together, these elements of the tax code have been highly effective as an incentive for investing in innovation.

As part of the Tax Cuts and Jobs Act of 2017 (TCJA), Congress changed how businesses write off R&D expenses. Starting in 2022, companies were no longer able to write off 100% of costs in the year they were incurred. Instead, to comply with these new rules, companies had to amortize those costs over five years (15 years for R&D expenses attributed to foreign research).

However, in 2025, the One Big Beautiful Bill (OBBB) introduced a new section to the Internal Revenue Code (IRC Section 174A) which permanently reinstates the pre-TCJA rules for domestic research and development expenditures.

To learn more about research expense capitalization and amortization, connect with your Warren Averett advisor directly, or ask a member of our team to reach out to you.

This article was originally published on March 3, 2023, and most recently updated on September 3, 2024.