Significant Changes to How Your Company Accounts for R&D Costs

If your company has been expensing costs related to research and development activities in the past, the Tax Cuts and Jobs Act of 2017 (TCJA) made crucial changes to Section 174, which will require you to capitalize these costs instead.

While 2017 might seem like ancient history, those changes went into effect for tax years beginning after December 31, 2021.

In short, the law takes away an organization’s ability to immediately deduct research and experimental (R&E) expenses in the year incurred, requiring those expenses to be capitalized and amortized over five or 15 years.

That’s a significant change for companies that incur costs for software development and other research and experimentation designed to redevelop or improve a product or discover information that would eliminate uncertainty.

While there has been some discussion around repealing or extending the applicable provision of the TCJA, the rules remain in effect for now, so it’s crucial for companies with these types of expenditures to start tracking and analyzing their costs.

What are Section 174 Costs?

Section 174 costs are all costs incidental to the redevelopment or improvement of a product or stemming from activities intended to discover information that would eliminate uncertainty.

Examples of Section 174 costs include:

- Salaries of research staff

- Supplies consumed during research activities

- Contract research expenses

- Rent and utilities for facilities used for research

- Depreciation

- Attorneys’ fees related to applying for patents

Overview of Section 174 Changes

Historically, Section 174 allowed taxpayers to immediately deduct research and experimental (R&E) expenditures under Section 174(a). Alternatively, taxpayers could elect to capitalize and amortize R&E expenditures over at least 60 months under Section 174(b).

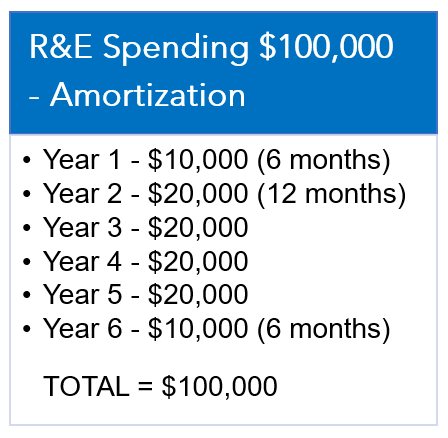

Under TCJA rules, R&E expenditures can no longer be deducted. Instead, they must be capitalized and amortized over five years (15 years for foreign expenditures).

The amortization period begins with the midpoint of any tax year in which the company incurs Section 174 costs, regardless of whether the expenditures were made before or after July 1. The amortization period runs until the midpoint of year six (or year 16 for development conducted on foreign soil).

This change is expected to make it more difficult for companies to invest in research and development in the U.S. It could also significantly impact a firm’s financial statements and cash flows.

Companies that might have in the past realized a tax loss due to the ability to write off R&E expenditures may instead have a taxable profit when costs they’ve been deducting for decades are no longer 100% deductible.

How Section 174 Impacts the Research & Development (R&D) Credit

There is quite a bit of overlap between Section 174 expenditures and the expenses eligible for the R&D tax credit.

R&D credit-eligible expenses include direct wages of research staff, supplies consumed in research activities and contract research expenses—all of which qualify as R&E expenditures.

Now that those R&E expenses must be capitalized and amortized over five or 15 years, there is some worry among taxpayers that only the amortized portion of their R&D expenditures will be eligible for the R&D credit in the future, resulting in a significant reduction in the available credit.

Fortunately, the changes to Section 174 do not impact the R&D credit directly. The deductibility of Section 174 expenditures and the R&D tax credit are separate and distinct sections of the Internal Revenue Code.

What Does the Future Hold?

In late 2021, it looked like implementation of Section 174’s mandatory amortization rules might be delayed. The House version of the Build Back Better Act proposed a delay to the effective date until taxable years beginning after December 31, 2025. However, the Senate could not get the votes needed to pass the legislation.

While mandatory R&E amortization is currently in effect, there are efforts underway in Congress to repeal it or defer implementation to a future year.

To date, efforts to repeal or delay it have been unsuccessful. Still, we might see negotiations to address Section 174 included in a year-end tax extenders package or as part of a budget reconciliation bill.

Learn More About Section 174

The new Section 174 requirements reach far beyond companies that have historically claimed the R&D credit.

Many entities that previously did not have enough R&D expenses to warrant a tax credit study, have only offshore R&D expenses or have net operating losses may need to start tracking, analyzing and amortizing their research and experimental expenditures for the first time.

If you have any questions about how the new Section 174 amortization rules apply to you or how they might impact your R&D tax credit, please contact your Warren Averett advisor or ask a member of our team to reach out to you.