FAQs About 1031 (Like-Kind) Exchanges by Real Estate Investors

If you’re planning a real estate re-investment, exploring 1031 exchanges may help you maximize your investment potential. Here’s what you need to know.

What is a 1031 Exchange?

1031 exchanges, often referred to as “like-kind” exchanges, are a powerful and widely used tax strategy for real estate investors. Named after Section 1031 of the United States Internal Revenue Code, these exchanges enable property owners to defer capital gains taxes when selling one property and acquiring another “like-kind” property of equal or greater value.

What is a “like-kind” property?

While the term “like-kind” may seem limiting, it encompasses a wide range of real estate assets.

For example, you can exchange a residential property for a commercial property or a vacant land for a rental property. This flexibility provides significant opportunities for investors to diversify their portfolios without incurring immediate tax obligations.

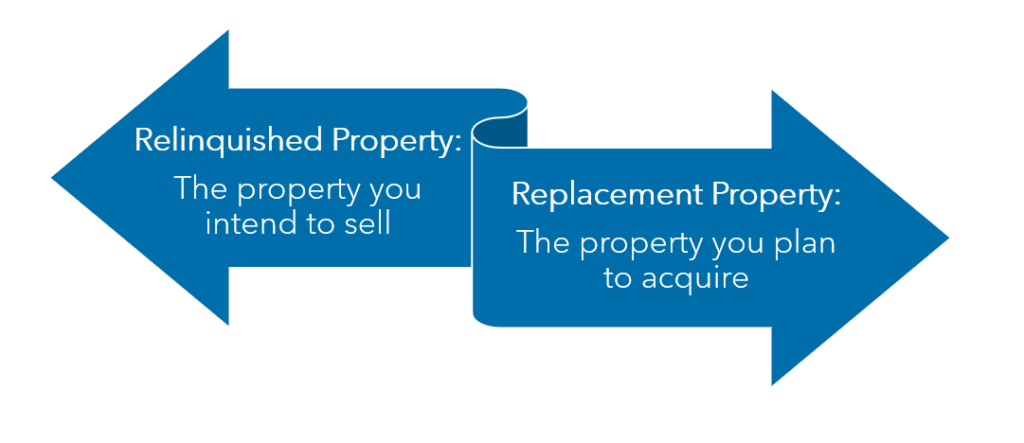

Ultimately, the replacement property (the property you plan to acquire as part of the exchange) must be of equal or greater value and similar in nature or character to the relinquished property (the property you intend to sell in the exchange).

What are the tax benefits of a 1031 exchange?

The primary benefit of a 1031 exchange is the deferral of capital gains taxes. This means that you can sell a property, reinvest the proceeds, and defer the capital gains tax until a later date. This can be particularly advantageous for long-term investors looking to compound their wealth over time.

In some cases, 1031 exchanges can be used as part of an estate planning strategy to pass down properties to heirs with a stepped-up basis.

What are the Rules and Requirements for 1031 exchanges?

To successfully execute a 1031 exchange, investors must adhere to several key rules and requirements to completely defer their gain.

These include:

- Meeting property eligibility requirements

- Identifying like-kind properties

- Meeting the identification period and acquisition period requirements

- Using a qualified intermediary

- Receiving no boot

What are the eligibility requirements for properties used in a 1031 exchange?

To be eligible for a 1031 exchange, you must be exchanging real property that is held for use as a business asset or an investment property. Personal residences, personal property, vacation homes and equipment are not eligible for a 1031 exchange.

What is a qualified intermediary?

In a 1031 exchange, an investor is prohibited from taking direct possession of the proceeds from the sale of the relinquished property. Instead, the qualified intermediary will take possession of the funds gained from the sale and will maintain control of those funds for the duration of the exchange process.

A qualified intermediary facilitates the transaction, assists in identifying potential replacement properties, facilitates closings, ensures compliance with IRS regulations and safeguards the funds.

All 1031 exchanges are required to have a qualified intermediary in order to protect the tax-deferred status.

What is the typical 1031 exchange timeline?

Within 45 days of selling the relinquished property (the identification period), the investor must identify potential replacement properties. The investor has 180 days from the sale of the relinquished property (the acquisition period) to complete the acquisition of the replacement property.

Adhering to this timeline is critical, and extensions are seldom granted.

What is the process for identifying properties?

During the 45-day period, you’ll notify your qualified intermediary of the specific properties you might want to acquire.

You can identify three properties without any maximum value, or you can identify an unlimited number of properties as long as the acquisition cost of all properties identified is less than 200% of the gross proceeds of your sale.

What is “boot”?

The term “boot” refers to any cash or property of lesser value received during the exchange that is not like-kind. While boot may not always invalidate a 1031 exchange, real estate investors should avoid receiving boot in an exchange because it may trigger capital gains tax liability.

Examples of boot could include:

- Personal property (like furniture or equipment)

- Variances between the mortgage of the replacement property and the relinquished property

- Stock

- Cash

Specific implications of boot depend highly on what is received, how much is received and what your unique circumstances are. Planning an exchange well ahead of time can go a long way in avoiding surprises in this area.

Learn More about 1031 Exchanges

If you’re re-investing in real estate, it’s a good idea to explore whether a 1031 exchange is right for you. And while it’s a great benefit, it’s important to not allow the tax deferral to rule your decision making.

Each scenario is different, so it’s important to work closely with your qualified intermediary and with your tax advisor to execute a successful exchange.

If you have any questions about how a 1031 exchange may work for you, contact your Warren Averett advisor directly, or ask a member of our team to reach out to you.