How Much Working Capital Do I Need? (Plus Five Ways to Get It)

Sometimes, businesses need additional working capital to plan for future growth, to expand a project or (in more serious scenarios) to keep their doors open.

Businesses can find themselves in these types of situations for many different reasons. It could be that capital wasn’t as readily available as planned, because of a series of missteps in decision making or due to an unforeseen event.

Regardless of the scenario, it’s always good to know how much working capital you need and what options are available to find some additional cash that can be used for the business.

How Much Working Capital Do I Need?

The question many businesses face is: “How much working capital do I need?”

The answer will vary based on which option the business pursues (see more on this below), a business’s current financial condition and what the capital is being used for (e.g., for growth or to stay in operation).

Lenders will consider the business’s condition (whether it’s losing revenue or growing steadily) when making these decisions. Some lenders will let businesses have access to a larger facility than what is needed, while others will limit the amount requested based on a business’s collateral, revenue or both.

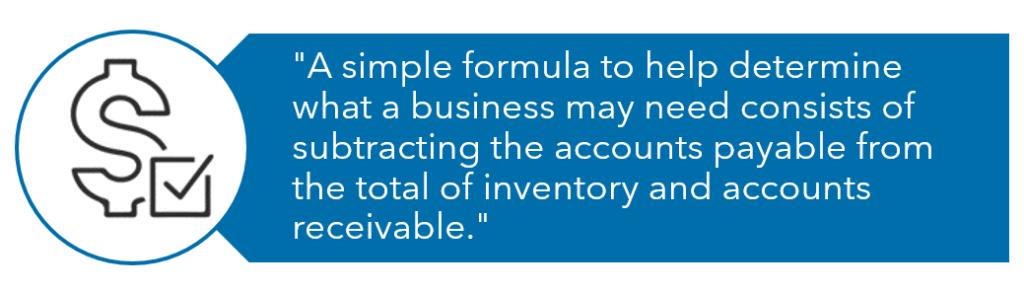

A simple formula to help determine what a business may need consists of subtracting the accounts payable from the total of inventory and accounts receivable.

How Can I Obtain Additional Working Capital?

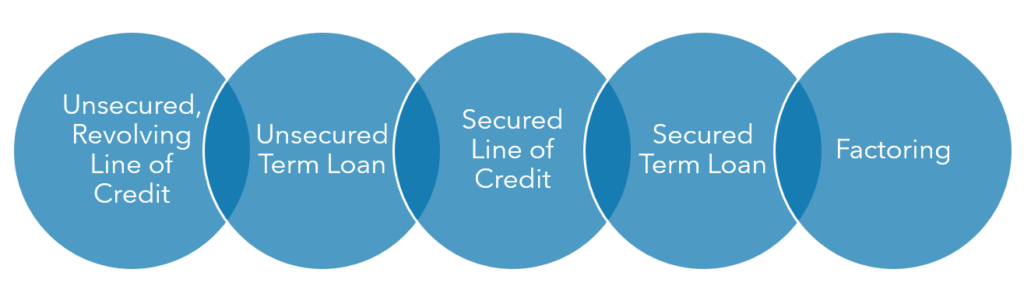

Below, we explore five options provided by bank and non-bank lenders that can help businesses obtain additional working capital.

Unsecured, Revolving Line of Credit

This option provides businesses the flexibility to draw on a set amount of credit that has been pre-approved by the borrower’s bank or other financial institution.

It is not secured by any collateral, but, rather, it is determined by the borrower’s finances, including but not limited to the financial statements, annual revenue and other metrics. The borrower can draw up to a set amount that is needed to cover expenses.

Unsecured Term Loan

This option provides a set amount of capital in a lump sum that is due on a date set by the lender. The capital amount and due date are set by the lender based on similar requirements to the unsecured, revolving line of credit.

Secured Line of Credit

This option differs from the unsecured line of credit in that some type of collateral is provided to secure a line of credit.

Some lenders will not lend to companies that have experienced any kind of loss in the past few quarters, while other lenders are willing to overlook losses due to various circumstances.

Regardless, the lenders typically seek collateral consisting of, but not limited to real estate, accounts receivable, inventory and machinery and equipment. Some lenders may also seek a personal guarantee, in which case the business owner puts up personal collateral to secure the line of credit.

Secured Term Loan

This option provides a set amount of capital in a lump sum that is due on a date set by the lender. The capital amount and due date are set by the lender based on similar requirements to the secured line of credit. It is very common to see real estate, inventory and machinery and equipment being the basis for a term loan.

Factoring

This option is tied to a business’s accounts receivable. Both banks and non-banks offer factoring solutions in which they will purchase a business’s receivables and will typically handle collections as well.

Do note that factoring may have limitations based on a business’s cyclicality, and most factors will not consider receivables past 75 days outstanding.

What Else Should I Know About Pursuing a Working Capital Solution for My Business?

Many of these options are readily available to businesses via their banks or other financial institutions. It is not uncommon, however, that a business max out or be denied additional funds by its current bank due to tightening lending parameters.

That said, there are many lenders out there that will lend where banks won’t, including in industries that aren’t typically favored, such as construction companies and companies that have medical receivables.

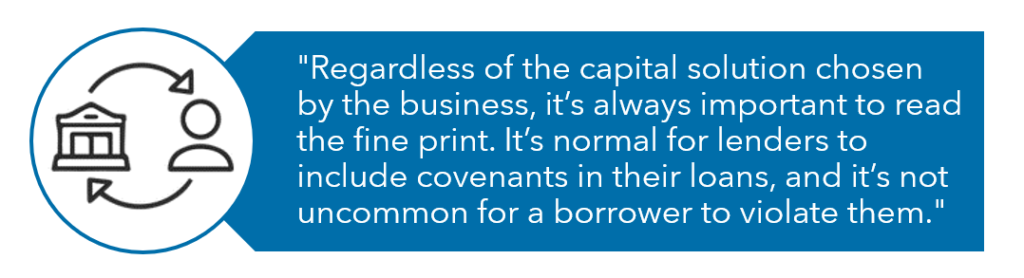

Regardless of the capital solution chosen by the business, it’s always important to read the fine print. It’s normal for lenders to include covenants in their loans, and it’s not uncommon for a borrower to violate them.

A business may already have a line of credit with its current bank, but it may also want to secure a term loan with a separate party. By securing a loan with another party, the business may have violated a covenant that would lead to dire consequences, such as seizing any assets posted as collateral with the bank. It’s important to review the covenants for any outstanding loan and any new loan to avoid conflict.

Learn More about Obtaining Additional Working Capital for Your Business

To learn more about what options are out there or how you may be able to tap into some of these products, have a member of our team reach out to start the conversation.

This article was originally published on March 31, 2020 and most recently updated on October 26, 2022.

This article reflects our views at the time this article was written and should be used as reference only. We recommend that you talk to your Warren Averett advisor, or another business advisor, for the most current information or for guidance specific to your organization.