What are Forms K-2 and K-3? (Plus, Why You May Need to File Them)

At the end of 2022, the IRS issued finalized instructions for partnership entities related to the filing of Forms K-2 and K-3 for years ending on or after December 31, 2022. As a result of these instructions, owners may see changes to the information provided them from their holdings in such entities with their annual K-1 packages.

What are Forms K-2 and K-3?

What is a Form K-2? Or a Form K-3 for that matter? In response to a growing and increasingly global economy, the IRS has created these forms to better capture and segment an entity’s foreign and domestic activity for the year.

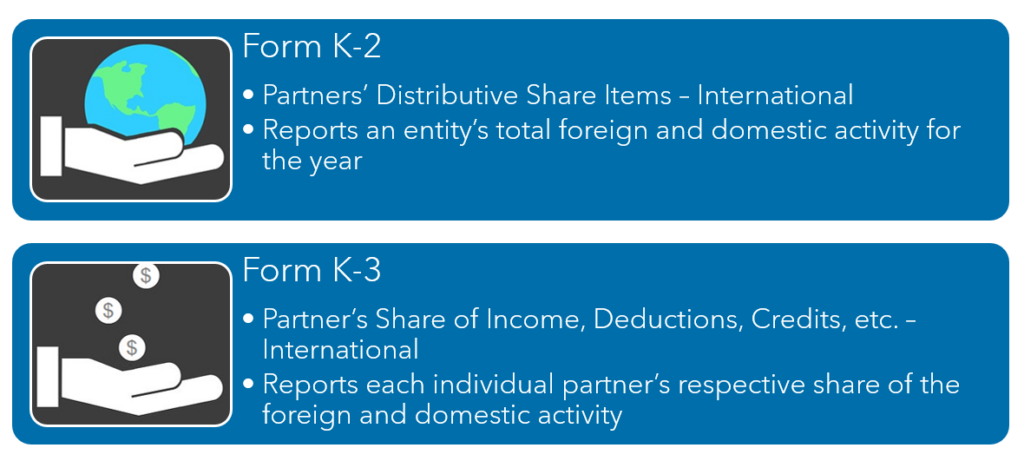

Form K-2 is titled “Partners’ Distributive Share Items – International” and reports an entity’s total activity with respect to these items.

Form K-3 is titled “Partner’s Share of Income, Deductions, Credits, etc. – International” and is filed to report each individual partner’s respective share of these items.

The forms and information contained therein will be used to help calculate your partners’ foreign tax credits and other international taxes such as GILTI and BEAT.

The goal of these forms is to provide consistent information to owners that enables them to have certainty around their required filings related to these items.

If My Company Doesn’t Conduct International Business, Do I Need Forms K-2 and K-3?

You may still have a need for Forms K-2 and K-3 even if you don’t do business internationally. Even if your business does not have any international activity, this information is needed by your partners for their tax returns.

Does My Partnership Really Have to File Forms K-2 and K-3?

The IRS currently has two exception paths that can be utilized to omit these forms from a 2022 filing. The first is the domestic exception, and the second is a Form 1116 exception.

Domestic Exception

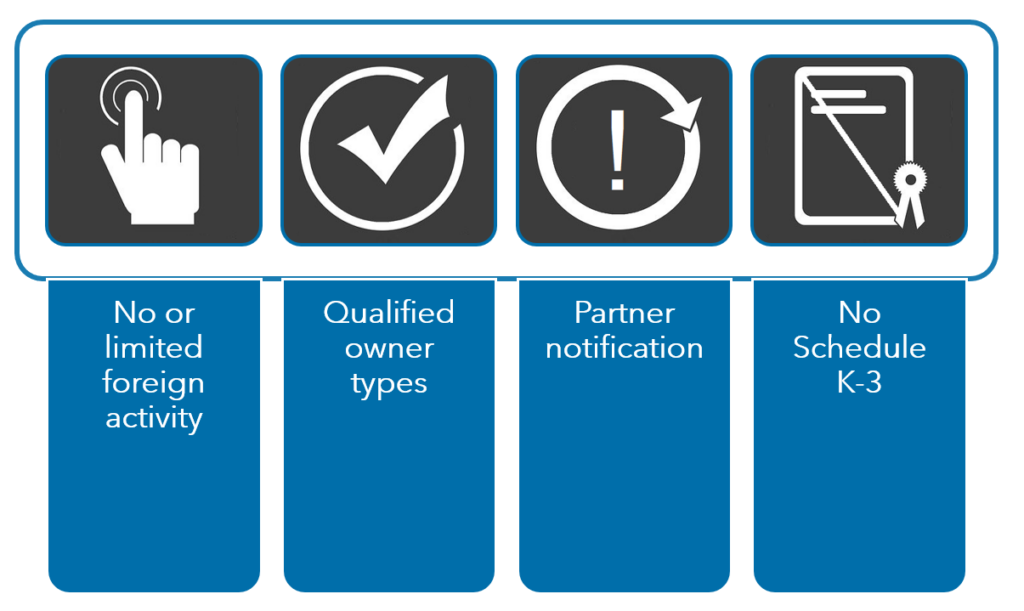

To utilize the domestic exception, all the below criteria must be met:

1. No or limited foreign activity

During a domestic partnership’s tax year 2022, the domestic partnership either has no foreign activity (as defined in the form instructions), or if it does have foreign activity, such foreign activity is limited to certain categories or amounts (again as defined in the form instructions).

2. Qualified owner types

During the tax year 2022, all the direct partners in the domestic partnership are qualified owner types:

- Individuals who are U.S. Citizens

- Individuals who are resident aliens

- Estates of domestic decedents

- Domestic non-grantor trusts with qualifying beneficiaries

- S Corporations with a sole shareholder

- Single-member LLCs with a qualifying single member

3. Partner notification

If you make it through the first two criteria, you must then furnish notification to each partner of the intent to omit the Form K-2 and K-3 from your 2022 filing. This notification can be attached to the partner’s K-1 for the year.

4. No Schedule K-3

No 2022 Schedule K-3 is requested by the one-month date, which is one month prior to the filing of the tax return

Note that if any partner in a partnership is also a partnership or multi-member LLC, then the partnership is not eligible for the domestic exception.

Form 1116 Exception

To utilize the Form 1116 exception, all the below criteria must be met:

- Every partner (both direct and indirect) does not have to file Form 1116 or 1118, and

- The partnership receives notification from each partner of their eligibility for the exception one-month or earlier from the filing date of the partnership.

If you meet either exception, you do not have to file Forms K-2 or K-3 with the IRS. However, if any partner requests a K-3, you must provide a completed form to the partner even if you are not required to submit it to the IRS.

What about S Corporations?

S Corporations are eligible to utilize both the exceptions listed above to omit the Form K-2 and K-3 filings from 2022 filings as outlined in the form instructions. As S Corporations are required to have only certain kinds of owners, which are all qualifying under #2 above, meeting the criteria for the domestic exception will be significantly easier for S Corporation filers.

Learn More about Filing Forms K-2 and K-3

As always, your Warren Averett Advisor is on top of these changes and is standing by to answer questions and lead you through your requirements for 2022.

Please contact your Warren Averett advisor directly or have a member of our team reach out to you.