GILTI and BEAT: What They Are and What They Mean for U.S. Multinational Corporations

Two provisions of the Tax Cuts and Jobs Act of 2017 (TCJA) may have unforeseen consequences for U.S. multinational corporations.

Global Intangible Low-Taxed Income and Base Erosion and Anti-Abuse Tax – otherwise known as GILTI and BEAT – are complex tax provisions. Here, we’ll explore GILTI and BEAT at a high level to help business leaders understand how the rules work and when they might impact their tax situations.

What is GILTI?

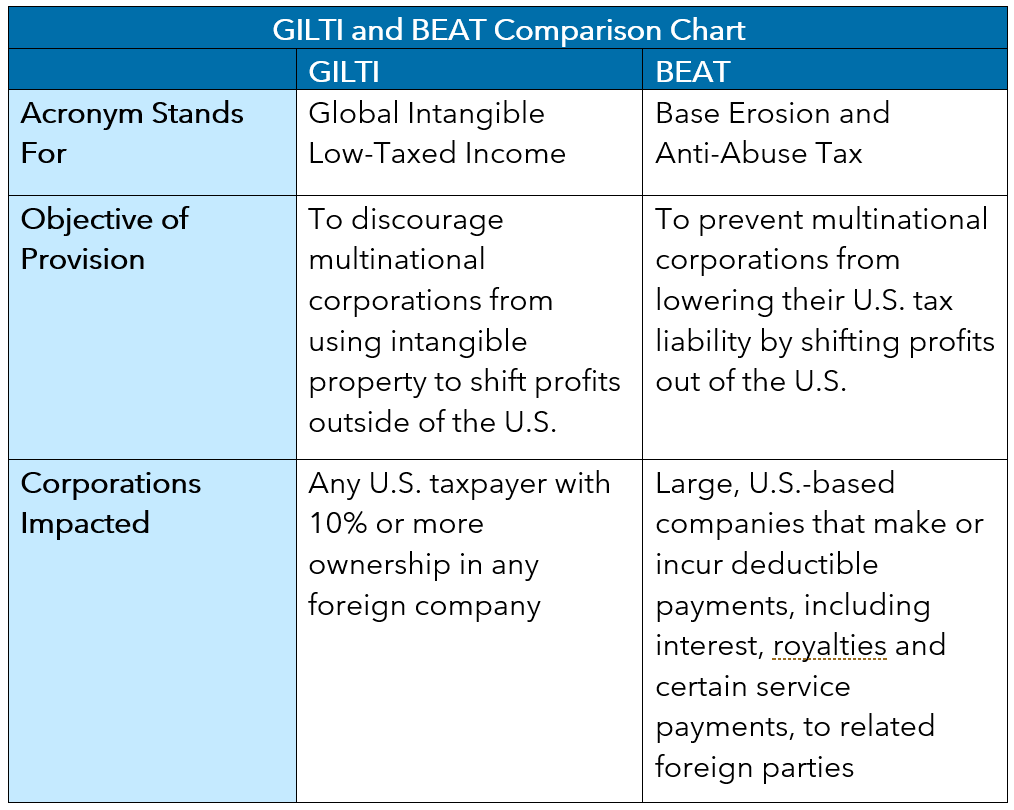

GILTI’s objective is to discourage multinational corporations from using intangible property (such as patents, software or goodwill) to shift profits outside of the U.S. by immediately taxing the net income of a controlled foreign corporation (CFC) that exceeds 10% of the net tax value of its depreciable assets.

Prior to the TCJA, those earnings may have been tax-deferred.

Essentially, each year, U.S. shareholders of CFCs must test if the CFC generated income exceeding its “routine income.” “Routine income” is set at 10% of the net tax value of its depreciable assets, such as equipment, buildings and machinery. The law presumes that any income exceeding this percentage must be derived from intangible assets.

This results in a yearly inclusion of foreign income and prevents U.S.-based multinational corporations, and any other U.S. taxpayer, from accumulating U.S. tax-deferred earnings offshore.

For some shareholders, routine income may be quite low, so shareholders are more likely to have their income taxed under GILTI. For example, this may be the case where:

- The CFC’s foreign profits are mainly from intellectual property;

- The CFC has limited tangible assets because it is a service business; or

- The CFC has tangible assets that are largely depreciated.

Any U.S. taxpayer with 10% or more (direct or indirect) ownership in any foreign company should assess the ratio of fixed assets to income for each CFC and evaluate how GILTI may affect their U.S. tax liabilities.

In computing taxable income, U.S. C corporation shareholders are allowed a deduction equal to 50% of GILTI for the 2018 through 2025 tax years and 37.5% of GILTI from taxable years after 2025.

The GILTI high tax exception can also be a useful planning option for shareholders with CFCs that earn income from foreign jurisdictions with high tax rates.

Pending Congressional proposals seek to reduce the net asset value from 10% to 5%, reduce the deduction even further to 25% or 28.5% and limit the benefit of the foreign tax credit under various proposed changes.

What is BEAT?

BEAT is a minimum tax targeting large U.S. multinational corporations that make (or incur) deductible payments, including interest, royalties and certain service payments, to related foreign parties. It is an additional minimum tax added to regular income tax.

BEAT is intended to deter foreign and domestic corporations doing business in the U.S. from avoiding their U.S. tax liability by shifting profits out of the country in the form of tax-deductible payments.

To be subject to BEAT, a U.S. corporate taxpayer must:

- Have average annual gross receipts of at least $500 million for the three preceding tax years;

- Have a base erosion percentage for the taxable year above the applicable threshold (3% or more of the total U.S. deductions and 2% for some specific industries); and

- Not be a regulated investment company (RIC), real estate investment trust (REIT) or S corporation.

In general, any outbound payments resulting in U.S. tax deductions, depreciation and amortization (except for purchases of inventory and service cost reimbursements) are considered base erosion payments and disregarded when computing alternative taxable income (referred to as “modified taxable income”).

U.S. companies are required to compute modified taxable income and compute alternative tax at 10% (increasing to 12.5% in 2026) each year. The tax liability for that tax year is the higher of the regular tax or the alternative tax computed without base erosion payments.

The Future of GILTI and BEAT

President Joe Biden has proposed several changes to corporate tax provisions, including replacing BEAT with the Stopping Harmful Inversions and Ending Low-Tax Developments (SHIELD) rule.

If enacted, SHIELD would ensure that income – regardless of where it’s earned – is subject to a minimum tax. Such legislation would have to be approved by Congress, so it could take a while for the Administration and Congress to agree on the details.

In the meantime, calculating the precise impact of GILTI and BEAT can be difficult because they can impact one another, be affected by other tax provisions and impact state income taxes.

Any U.S. multinational corporation with high income relative to its investment in tangible assets or considerable payments to foreign related parties should consult with a professional to assess the potential impact of GILTI and BEAT and model different tax structuring opportunities to develop an optimal tax strategy.

Additional congressional proposals seek to gradually increase the BEAT tax rate to 15% and 18% in 2024 and 2025 and add relief for such payments that are already subject to a sufficient rate of foreign taxes, generally expected to be the effective BEAT tax rate. Additionally, the application of BEAT to a U.S. taxpayer would remain for a 10-year period once the taxpayer becomes subject to BEAT.

Learn More about GILTI and BEAT

The descriptions we’ve included here are meant to provide a brief, high-level summary of two very complicated tax provisions.

As always, if you have any questions about GILTI, BEAT or any other international tax arrangements, contact your Warren Averett advisor or ask a member of our team to reach out to you.