The IC-DISC Tax Incentive: What It Is and How It Works

The globalization of the marketplace has ushered in many changes for businesses and has guided U.S. tax policy to incentivize exportation of goods and services by U.S. companies.

The Interest Charge Domestic International Sales Corporation (IC-DISC) was originally created by Congress to facilitate export sales by providing a tax deferral mechanism. The IC-DISC can now provide permanent tax savings for pass-through entities because of the 23.8% qualified dividend rate.

While individuals, S Corporations, partnerships, LLCs or C Corporations can all utilize an IC-DISC if they have export sales, this article will focus on the potential tax savings available to pass-through entities.

What is an IC-DISC, and how does it work?

An IC-DISC is a tax incentive for U.S. manufacturers that export goods. The savings afforded by the IC-DISC are meant to increase the competitiveness of a U.S.-based company with export sales and to help it compete in the global market.

To take advantage of the IC-DISC tax incentive, a U.S. exporter must create a separate entity, an IC-DISC, which acts as a commission agent on the exporter’s export sales.

The U.S. exporter pays a tax-deductible commission to the IC-DISC, which doesn’t pay income tax on the commission income. The IC-DISC then pays a dividend to its shareholders who are taxed at the current preferred qualified dividend tax rate of 23.8%, as opposed to the ordinary income tax rate on pass-through income.

With the 20% Qualified Business Income (QBI) deduction introduced by the Tax Cuts and Jobs Act, the effective marginal rate on pass-through entity income can be as low as 29.6%. The tax rate difference between the tax-deductible commission (paid by the exporter to the IC-DISC) and the dividends (paid by the IC-DISC to its shareholders) creates permanent tax savings.

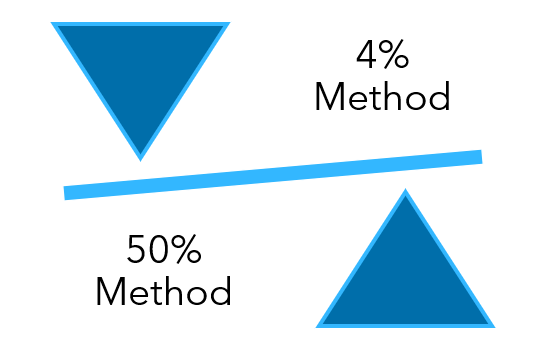

The U.S. exporter calculates the commission using one of the following methods:

- 4% Method – The IC-DISC earns a commission of 4% of qualified export receipts

- 50% Method – The IC-DISC earns a commission based on 50% of the combined taxable income from qualified export sales

Whichever method the exporter uses, the goal is to maximize tax benefits for U.S. exporters by reducing taxable income through commissions paid to the IC-DISC. One way to maximize the commissions is to use a “transaction by transaction” approach, where the commissions are calculated separately for each transaction (i.e., export sale).

Example of the IC-DISC Tax Incentive

To illustrate, say a U.S. manufacturer, taxed as an S corporation, exports $5 million worth of goods in a given year, with $1 million in export-related net income. The manufacturer establishes an IC-DISC to take advantage of the tax incentive. Here’s a step-by-step breakdown of how the tax incentive works and the potential tax savings.

Step 1: Choose a Commission Calculation Method

- 4% Method – The IC-DISC earns a commission of 4% of qualified export receipts ($5,000,000 x 4%), or $200,000.

- 50% Method – The IC-DISC earns a commission of 50% of the combined taxable income from export sales ($1,000,000 x 50%), or $500,000.

The company selects the 50% method to maximize tax savings.

Step 2: Reduce the Exporter’s Taxable Income

The $500,000 commission is deductible for the manufacturer, reducing its taxable income by this amount.

Tax savings (assuming an effective marginal rate on pass-through income of 29.6%) = $500,000 x 29.6% = $148,000

Step 3: Taxation of the IC-DISC Dividend

The IC-DISC pays no federal income tax on its commission income. Instead, the $500,000 is distributed as a dividend to the manufacturer, whose shareholders are then taxed at the qualified dividend tax rate of 23.8% on the dividend income.

Note that if the IC-DISC did not pay the $500,000 in a dividend to the manufacturer, an interest charge would apply to the deferred tax.

Tax on IC-DISC Dividends = $500,000 x 23.8% = $119,000

Step 4: Net Tax Savings

The total tax savings provided through the IC-DISC tax incentive are calculated by netting the exporter’s tax savings from Step 2 and the taxes that shareholders pay on the dividends from Step 3.

Net tax savings = $148,000 – $119,000 = $29,000

What if the IC-DISC is owned by foreign owners in a treaty country?

If the IC-DISC is owned by foreign owners in a treaty country, the tax rate on the dividends paid out by the IC-DISC could be as low as zero.

Which companies qualify to set up an IC-DISC?

To qualify for tax advantages associated with an IC-DISC, a company must be a privately held U.S. taxpayer with export sales of products primarily produced in the United States.

What is the process for initially establishing an IC-DISC?

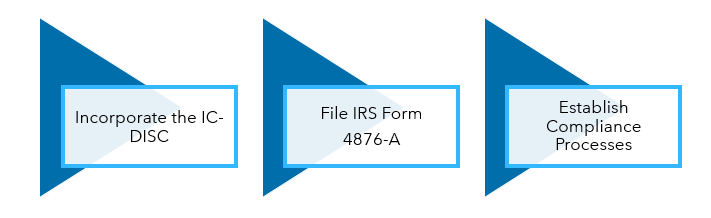

Establishing an IC-DISC involves a few steps to comply with IRS requirements and qualify for tax benefits.

- Incorporate the IC-DISC – The IC-DISC must be a separate legal entity incorporated under state law.

- File IRS Form 4876-A – Once the corporation is established, it must file IRS Form 4876-A, Election to Be Treated as an Interest Charge DISC, with the IRS within 90 days of the beginning of the tax year.

- Establish processes to ensure continued compliance – After creating the IC-DISC, the entity needs systems for tracking export receipts and calculating commissions accurately. These measures should include maintaining detailed records, monitoring export sales to ensure eligibility and preparing required annual tax filings. Additionally, the IC-DISC cannot engage in operating activities or hold excessive assets beyond those necessary to perform its functions.

What are the ongoing compliance requirements for maintaining an IC-DISC?

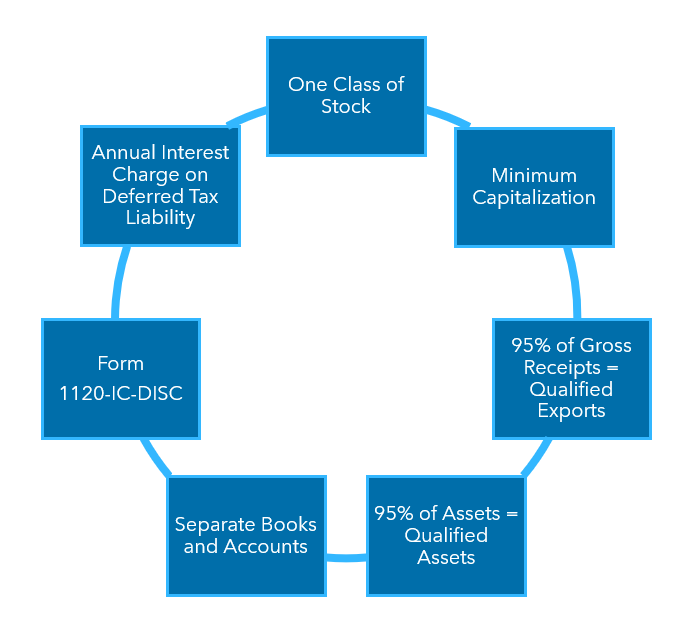

Maintaining IC-DISC status requires adherence to specific IRS guidelines to ensure the entity remains compliant and continues to qualify for the associated tax benefits. The requirements are as follows:

- Have one class of stock – The IC-DISC must maintain a single class of stock throughout its existence, with a minimum par value of $2,500, which must be fully paid and outstanding at all times.

- Maintain minimum capitalization – The corporation must retain at least $2,500 of capitalization to meet the IRS qualification threshold.

- At least 95% of gross receipts must be qualified exports – A minimum of 95% of the IC-DISC’s gross receipts must derive from qualified export sales. This includes income from exporting goods produced in the U.S. or related services.

- At least 95% of assets must be qualified assets – At least 95% of the IC-DISC’s assets must be directly related to its export activities, such as trade receivables from export sales or cash intended for qualified distributions.

- Maintain separate books and accounts – The IC-DISC must operate independently from its parent company, maintaining separate financial records and bank accounts to track export-related transactions.

- File Form 1120-IC-DISC annually – An entity must file Form 1120-IC-DISC annually with the IRS to report the corporation’s income and confirm compliance with IC-DISC regulations.

- Pay annual interest charge on deferred tax liability – Shareholders of the IC-DISC must pay an annual interest charge on the deferred tax liability arising from commissions earned but not yet distributed.

Learn More and Get Started with IC-DISC

Like many tax incentives, an IC-DISC can be complex, but it essentially does one thing—rewards innovation and sales of U.S. goods and services overseas. This opportunity should be examined for any closely held U.S. company, if even a portion of their products or services are suspected to be used outside of the U.S.

Connect with a Warren Averett advisor to learn if your manufacturing business qualifies or to determine what type of IC-DISC would best benefit your company.