What Happens in a Quality of Earnings Analysis?

The sale of your business represents new opportunities and growth, but it also comes with a highly technical M&A process. It’s a complicated and emotional process for all parties involved, and there’s a reason why more transactions fall through than cross the finish line.

The more prepared you are, the more likely you’ll be to succeed, and a quality of earnings analysis is an essential factor in that preparation that can make or break a transaction for a buyer.

Knowing what to expect from the process is the first step in navigating negotiations well and setting your business up for a successful sale. Here’s what you need to know about what actually happens during a quality of earnings analysis.

What is a Quality of Earnings Analysis?

A quality of earnings analysis is a comprehensive evaluation of a company’s financial statements and tax returns, typically prepared by an accounting or advisory firm. A quality of earnings analysis is not an audit and, therefore, no opinion is given.

The primary objective of a quality of earnings analysis is to assess the sustainability and accuracy of historical earnings and the achievability of future earnings.

Why Do I Need a Quality of Earnings Analysis?

In today’s environment, the majority of transactions that occur in the middle market require some form of quality of earnings analysis to transact.

It’s required by most buyers either for their own analysis or as required by their investors and finance partners.

How Long Does a Quality of Earnings Analysis Take?

The timeframe of a quality of earnings analysis can vary depending on the complexity and availability of data. The majority of middle market analyses typically take three to four weeks. The analysis culminates in the delivery of your quality of earnings report.

What Happens in the Process of a Quality of Earnings Analysis?

During a quality of earnings analysis, the advisory team gathers and analyzes account-level data on a company’s Profit and Loss Statement (P&L) and Balance Sheet to examine the underlying components of a company’s earnings and identify potential issues and areas of concern.

This includes:

- Evaluating the quality, sustainability and accuracy of the company’s financial performance, shedding light on its historical financial trends and the strength of its earnings, and

- Normalizing earnings, considering how this company would have been run under “normal” or “new” circumstances. Ultimately, the goal is to exclude the impact of extraordinary and non-operational events.

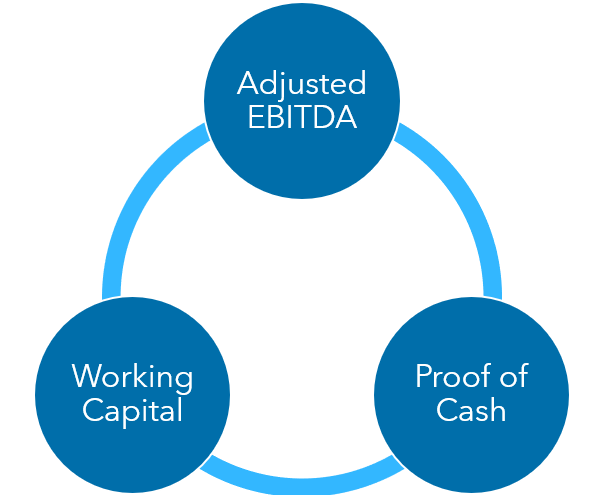

What Areas are Analyzed in a Quality of Earnings Analysis?

Three key areas are analyzed in a quality of earnings analysis and are essential components of the resulting quality of earnings report: adjusted EBITDA, proof of cash and working capital.

Adjusted EBITDA

Focusing on the core operational and accounting-standard-compliant earnings of the business, EBITDA (earnings before interest, tax, depreciation, and amortization) is often used as a proxy for “operating” cash flow in middle-market M&A.

EBITDA is commonly used to set enterprise value for middle market transactions because it provides a clearer picture of a company’s operating performance and profitability.

EBITDA focuses solely on a company’s operating performance by excluding non-operating items, providing a more accurate reflection of the company’s core earnings potential and ability to generate cash from operating activities.

Adjusted EBITDA is a critical metric during due diligence, and the quality of earnings analysis involves validating EBITDA through a deep dive into the P&L and Balance Sheet accounts.

To ensure accounting compliance, a quality of earnings analysis adjusts EBITDA for the accounting compliance stated in the Letter of Intent (LOI), although it shouldn’t be solely relied upon for complete accounting compliance.

The quality of earnings analysis also evaluates revenue recognition practices to minimize discrepancies in reporting revenue, and expense analysis helps identify non-recurring items, inefficiencies and cost-saving opportunities.

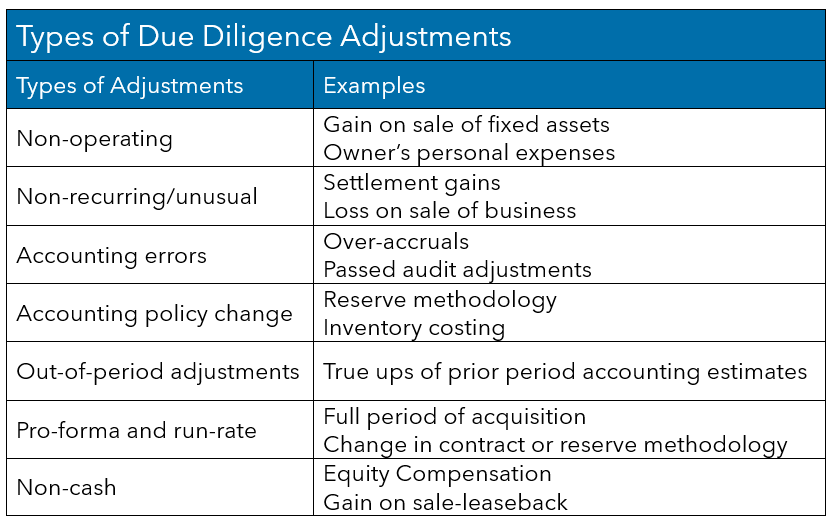

It includes adjustments to the financial statements, providing potential buyers with a more accurate picture of the company’s earnings. These adjustments fall into three categories: due diligence adjustments, management-proposed adjustments and proforma adjustments.

Due Diligence Adjustments

Diligence adjustments are identified by the advisory team during the due diligence procedures and vary significantly in nature (e.g., normalizing expenses, cash to accrual adjustments, revenue recognition adjustments, etc).

Management-Proposed Adjustments

Management-proposed adjustments are typically identified by management as extraordinary items such as non-recurring or non-operational items incurred by the business (e.g., non-recurring legal or consulting fees, owner expenses, etc).

Proforma Adjustments

Proforma adjustments are adjustments to past operating results, as if events that have occurred or are expected to occur took place at the beginning of the analyzed periods. They are expected to affect EBITDA on a go-forward basis (e.g., new processes affecting profitability, hiring additional employees, etc).

Comparability of periods is instrumental when trying to predict future cash flows based on past business operations. In order to present all periods on a comparable basis and to reflect recurring operations, it’s necessary to push adjustments into the appropriate periods.

Common examples of proforma adjustments include management’s go-forward compensation, loss of significant customers, significant changes in the cost of key raw materials, foreign exchange adjustments to present historical financials on consistent foreign exchange rates, purchase accounting items, acquisitions completed in the current year, stand-alone audit fees, etc.

Other Considerations

Other items may be identified during diligence but are not included in adjusted EBITDA. Additional adjustments could be found in many places, including:

- Audited financial statements

- Memorandums, management reports and board minutes

- Various source documents

- Audit working papers

- Key areas where controls/accounting are weak

- Comprehensive data room financial documents

Overall, the focus of a quality of earnings analysis is on validating EBITDA, identifying adjustments and providing potential buyers with a clear understanding of the company’s true earning potential.

Proof of Cash

The proof of cash is an important piece of a quality of earnings analysis because it checks the accuracy of a company’s cash performance, cash flow trends and cash balance.

It involves comparing the cash inflows and outflows recorded in the bank statements to the revenue and expenses reported in the company’s financial statements, considering adjustments for accrual accounting.

This verification gives potential buyers confidence that the reported earnings are supported by actual cash transactions. The proof of cash also provides buyers with valuable insights into the company’s cash cycles and overall financial position.

Working Capital

A quality of earnings analysis will assess a company’s quality of working capital to bring clarity to the organization’s cash cycles and cash demand required to operate. The analysis will examine the management of current assets, liabilities, the company’s ability to efficiently manage cash flow and any areas of concern.

Negative net working capital can raise liquidity and financial management concerns for a company in a transaction. In middle-market deals, buyers often structure transactions to be “cash-free and debt-free,” meaning they take on the responsibility of providing additional working capital beyond the closing date to address any negative net working capital situation.

As a result, potential buyers may carefully assess the company’s working capital position and its implications during the due diligence process to understand the financial implications of the transaction.

Each industry and business type have different working capital realities, and a quality of earnings analysis is tailored to the requirements driven by an organization’s industry and type.

Your advisory team will help define the adequate level of working capital, as defined by the deal’s LOI, to be left in the business, by providing the information necessary based on due diligence findings.

As with EBITDA adjustments, net working capital can be adjusted to provide a more accurate representation of a company’s cash needs. Adjusting net working capital helps potential buyers understand the true working capital requirements of the business, its assess and its operational efficiency.

Seasonal variations, misstated receivables, obsolete inventory, changes in deferred revenue and adjustments to accrued liabilities are some ways net working capital can be adjusted during a quality of earnings analysis.

How involved will I be as a business owner in the quality of earnings analysis? What’s expected of me?

Your advisory team will typically send you a detailed list of the data you’ll need to provide for them to be able to complete the quality of earnings analysis. If you provide them with access to the business’s accounting system, the team may be able to fulfill many of the requests for information on their own.

Usually, after all of the initial requests for information are met, your advisory team will request management meetings to ask questions and dig into the financials. These meetings could be anywhere from two hours to two days long, depending on the complexity of the business.

After the management meeting, there are usually follow-up requests driven by findings within the analysis.

How will a quality of earnings analysis affect a company’s purchase price?

A company’s enterprise value can be set in many ways. Most often in the middle market, it’s set using a multiple of EBITDA.

Because a quality of earnings analysis is primarily focused on EBITDA, every adjustment can have a potential impact on purchase price.

Your advisory team’s balance sheet analysis helps determine:

- The working capital PEG that, at close, will be used to determine the working capital adjustment

- The amount of debt and debt-like items

- Nuances that may impact how much cash the seller will keep

Learn More about Your Business’s Quality of Earnings Analysis

It’s critical for sellers to have a good understanding of what a quality of earnings analysis is and how it can impact your transaction.

If you have more questions about your company’s quality of earnings analysis ahead of a transaction, connect with your Warren Averett advisor, or ask a member of our team to reach out to you.