Navigating Your Quality of Earnings Report

A quality of earnings report is one of the most crucial documents in the middle market M&A process. But understanding a quality of earnings report is significantly different than reading the audited financial statements most business owners are accustomed to seeing.

Here, we’ve outlined the basics of how to read, use and interpret your company’s quality of earnings report.

What is a Quality of Earnings Report?

The quality of earnings report is one of the key documents used in the due diligence process, but it can also help business owners prepare for an acquisition ahead of time. The quality of earnings report draws out the financial insights at the core of the value of the business and can help develop a roadmap to optimize value of the acquisition.

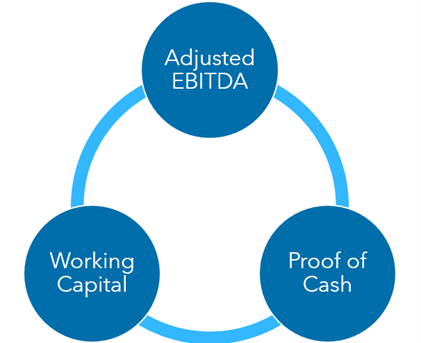

The following outputs of the quality of earnings analysis are the core to the quality of earnings report:

Proof of Cash

Proof of cash validates and reconciles cash basis revenue and expenses to the company’s bank account. This gives the reader confidence that the financial statements are anchored to the bank statements—reflecting the actual cash collected or disbursed by the company.

Working Capital Analysis

The working capital analysis supports both the buy side and sell side in setting a level of “adequate working capital” to operate the business, as defined by the signed letter of intent and represented as an average or percentage of revenue looked at in three, six or twelve-month periods, which is expected to be left in the business at close.

Adjusted EBITDA

Adjusted EBITDA shows what the earnings of the business are, after adjusting for non-operational and non-recurring, accounting principle-based adjustments and normalizations. Adjusted EBITDA should not be used as an exact proxy for cash flow as it excludes key-cash-flow-related needs, including taxes, interest and capital expenses, which all have cash outflow implications.

Additionally, it’s important to balance the core outputs from the quality of earnings report with additional analysis focused on cash flows to accompany the working capital analysis. Most quality of earnings reports will also cover analysis focused on the company’s capital expense needs and a cash conversion cycle in order to give the reader of the report a fuller understanding of the cash needed to operate the business.

How Is a Quality of Earnings Report Used?

These three outputs of a quality of earnings report are used:

- By business owners to help optimize the value of the business and prepare for the acquisition process by focusing on key areas of analysis, transparency and performance

- By potential buyers to examine the target company’s financials, operations and other aspects before finalizing the deal, and to assess the risks, opportunities and overall value of the target company

- By buyers and sellers to negotiate and validate the final deal terms and in closing the deal—especially during the process of setting adequate working capital or re-trading on the agreed upon valuation based on the work done to better understand the business’s earnings.

How Should a Business Owner Prepare To Review Their Business’s Quality of Earnings Report?

To fully understand what’s being communicated in the quality of earnings report, you’ll need to have a thorough grasp of operations and accounting in order to interpret the findings that were identified in your quality of earnings analysis.

It’s also important to note here that due diligence (and specifically reviewing the quality of earnings report) can be an emotional process. Without setting the right mindset before you review your report, it’s easy to become defensive. Remember to read your quality of earnings report with an open mind to avoid clouding your logic—which could ultimately damage your deal.

How Is a Quality of Earnings Report Different Than Audited Financial Statements?

A quality of earnings analysis is not an audit. So, a quality of earnings report is very different than an auditor’s opinion on financial statements.

An audit examines a company’s financial statements and evaluates them for accuracy and adherence to accounting standards. A quality of earnings analysis examines the sustainability and accuracy of a company’s earnings and working capital.

A formal opinion is not issued as part of a quality of earnings report.

What Is the Format of a Quality of Earnings Report?

A quality of earnings report is usually presented as an Excel data pack, sometimes including a PDF report.

Typically, the Excel portion of a quality of earnings report will be organized by tabs within the document, distinguishing the executive report, entity-level financial statements, and specific analysis of areas like sales and vendor concentrations, inventory, prepaid and accrued expenses, accounts receivable, and accounts payable agings.

Most reports will also have a summary of procedures tab, which acts as a table of contents for the document.

What Does It Mean if a Report Note Says That It’s “Not Quantified?”

When a provider is unable to quantify their findings in a quality of earnings report, they will note this in the report as “not quantified.” This is most often due to a lack of data or evidence available to the provider to support a calculation.

However, it also means the adjustment or consideration was important enough to mention regardless of having no way to calculate it. These items are important for a business owner to consider, despite a lack of supporting data.

It’s best to help your provider quantify as much information in your quality of earnings report as possible. Having more quantifiable information can help facilitate negotiations based on facts and avoid having difficult negotiations based on theory.

If your quality of earnings report includes “not quantified” notes, begin capturing the data that will help quantify the notes over time.

Learn More About How To Interpret and Use Your Company’s Quality of Earnings Report

Understanding the role of your quality of earnings report in middle market M&A is crucial for business owners looking to maximize the value of their companies.

By simplifying complex accounting concepts, focusing on key areas of analysis, and taking actionable steps to improve financial transparency and performance, business owners can set themselves up for success in M&A transactions and attract potential buyers who recognize the quality of their earnings.

To learn more about how to position your business for a successful transaction, connect with your Warren Averett advisor directly, or ask a member of our team to reach out to you.