Tax Treatment of ESOPs: The Business Leader’s Guide

Employee Stock Ownership Plans (ESOPs) offer benefits for both organizations and their employees. They can boost employee morale, enhance team retirement savings and offer potential tax advantages.

But, understanding the complex tax implications of ESOPs is crucial for maximizing these benefits and avoiding costly mistakes.

To help you make the most of your organization’s ESOP, we’ve highlighted the key aspects of ESOP tax treatment for businesses and the individuals they employ—along with common pitfalls to watch out for along the way.

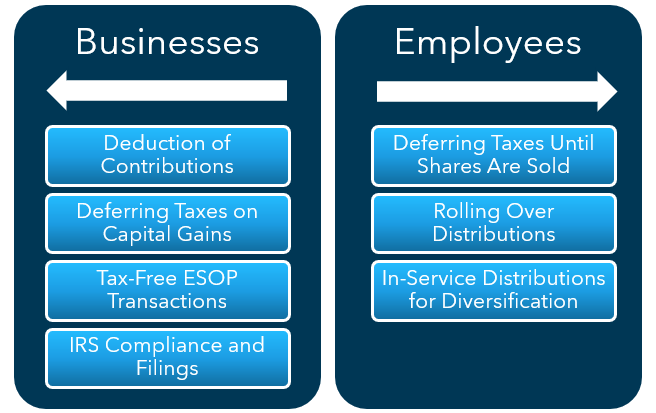

ESOP Tax Treatment Essentials for Businesses

There are many potential ESOP tax benefits for businesses, but maintaining these advantages requires careful IRS compliance from your organization.

Deduction of Contributions

One of the most attractive features of ESOPs for businesses is the tax deductibility of contributions for C corporations. C corporations owned by an ESOP can deduct contributions made to the ESOP trust—up to 25% of eligible payroll—whether in cash or stock. This can reduce the company’s tax liability while allowing the business to fund employee retirement benefits.

Contributions used to repay ESOP acquisition loans are also deductible, up to 25% of the covered payroll amount.

Deferring Taxes on Capital Gains

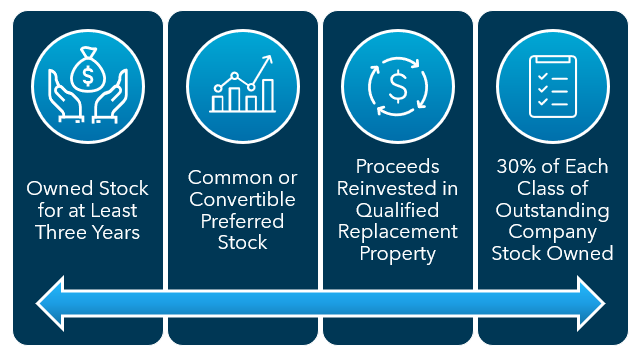

Shareholders selling shares of a C Corporation to an ESOP may defer capital gains tax under certain conditions.

To qualify:

- The shareholder must have owned the stock for at least three years.

- It must be either common or convertible preferred stock.

- The shareholder must reinvest the proceeds in qualified replacement property within a certain period.

- The ESOP must own at least 30% of each class of outstanding company stock after the sale.

Tax-Free ESOP Transactions

An ESOP is a tax-exempt entity, and one advantage of having an ESOP-owned S Corporation is that there is no federal income tax on the ESOP’s share of profits. In addition, most states follow the federal tax treatment.

Cash distributions to the ESOP aren’t taxable until the ESOP distributes to plan participants at retirement, termination of employment, death or disability.

IRS Compliance and Filings

Complying with IRS requirements is critical for maintaining ESOP tax benefits. Annual compliance involves:

- Filing Form 5500, including Schedule E, to report annual information about the ESOP to the IRS and the U.S. Department of Labor (DOL)

- Undergoing an annual audit if the plan has 100 or more eligible participants at the beginning of the plan year

- Preparing a Summary Annual Report (SAR) to provide employees with plan details

- Undergoing an ESOP valuation by a qualified independent appraiser at least once per year to determine the fair market value of contributions and distributions

ESOP Tax Treatment Essentials for Employees

Employees at ESOP-owned organizations can enjoy tax benefits of their own—such as deferring taxes on ESOP shares until they sell them or the company repurchases them, receiving favorable tax treatment for stock distributions and rolling over distributions into retirement accounts.

Deferring Taxes Until Shares Are Sold

One of the main ESOP tax benefits for employees is the ability to defer taxes until they sell their shares or the ESOP repurchases them.

While employees do not pay taxes on shares allocated to their accounts while employed, they will owe taxes (unless they roll over into a qualified retirement plan) upon distribution of the shares—typically when they retire, terminate employment or otherwise become eligible for a distribution.

ESOP distributions are generally done in installments and are taxed at ordinary income rates. However, if an employee receives a lump sum distribution in company stock, the tax treatment is more favorable.

The lump sum stock distribution is valued at the company’s cost to purchase the stocks and will be subject to ordinary income tax. When the shares are sold back at the fair market value (FMV), at the date of sale, the appreciation in value is taxed at the lower long-term capital gains rate.

For example, if an employee receives a lump sum stock distribution with a cost of $50,000 and sells them for FMV of $75,000, the employee will pay ordinary income tax on the $50,000 and capital gains tax on the $25,000 gain.

Rolling Over Distributions

Employees can roll over ESOP distributions into an Individual Retirement Account (IRA) or another qualified retirement plan to continue benefitting from tax-deferred growth. Employees must execute the roll-over within 60 days of receiving the distribution to avoid penalties or immediate taxation.

In-Service Distributions for Diversification

ESOPs must offer eligible participants the option of diversifying their accounts after they reach age 55 and have at least 10 years of participation in the plan.

These in-service distributions allow employees to transfer up to 50% of their ESOP account balance to other investment options under the ESOP or another plan, such as a 401(k) plan.

If the employee opts for a direct payment and does not roll it over to a qualified retirement account, the employee is then responsible for taxes and penalties when they file their tax return for the year they received the payment.

Potential ESOP Tax Pitfalls and How To Avoid Them

While employees and businesses stand to benefit from the tax treatment of an ESOP, certain ESOP transactions can trigger tax penalties and lead to negative consequences for your organization and your employees.

That’s why it’s critical to maintain careful compliance and to keep a thorough understanding of your ESOP’s requirements. Here are a few of the most common ESOP tax pitfalls that we see (and what you can do to avoid them).

Excess Contributions

The IRS limits ESOP contributions to prevent abuse. Cash and stock contributions are capped at 25% of eligible payroll. Exceeding these limits can result in penalties for the sponsoring company and jeopardize the ESOP’s qualified status, so it’s critical to carefully manage the contributions your company is making.

Mishandled Distributions

Lump-sum distributions can create large, immediate tax liabilities for employees. Opting to offer installment payments instead can spread the tax impact over time, but installment payments require careful administration to comply with IRS rules.

Economic Downturns and Employee Exits

Declines in business value during an economic downturn may affect the ESOP’s ability to fund distributions. The departure of a large, long-tenured employee can also strain the ESOP’s cash flow, particularly if the ESOP is required to repurchase shares at their current FMV. Companies can reduce this risk with proactive cash flow management and establishing a repurchase liability reserve.

Transaction Costs

Generally, the costs associated with establishing an ESOP are not tax-deductible. Companies can, however, structure contracts to include success-based fees contingent upon the ESOP transaction’s completion and receive a tax deduction of these costs.

Learn More About the Tax Treatment of ESOPs

Compliance is essential, but long-term success requires more than a basic understanding of the tax treatment of ESOPs. Companies must align ESOP strategy with their financial goals while navigating complex rules and regulations.

Working with advisors helps ensure compliance, optimize benefits and mitigate risks. Connect with a Warren Averett advisor for personalized advice on structuring and managing your ESOP for maximum benefits.